バックドア Roth IRA の設定は混乱する可能性があるため、このプロセスを実行するときに参照できる手順についてのチュートリアルをまとめてみようと思いました。始めましょう。

バックドア Roth IRA とは何ですか?

バックドア Roth IRA を行うべきなのは誰ですか?

バックドア Roth IRA をいつ行うべきですか?

バックドア Roth IRA の長所と短所

バックドア Roth IRA の税金への影響

バックドア Roth IRA ステップ

バックドア Roth IRA の間違いを修正および防止する方法

バックドア Roth IRA に関するよくある質問

その名前にもかかわらず、バックドア Roth IRA はアカウントではありません。これは 2 つのステップからなるプロセスです。

<オル>これら両方のステップのルールを理解していれば、それらを組み合わせるのは問題ありません。

低所得者の場合は、Roth IRA に直接寄付するだけで、このバックドア Roth IRA プロセスをスキップできることに注意してください。

低所得者は、2024年に14万6,000ドルから16万1,000ドル(夫婦共同申告の場合は23万ドルから24万ドル)の段階的廃止範囲に基づく修正調整総所得(MAGI)として定義されます。一部の医師(研修医、従業員歯科医、パートタイマー、さらには非収入の男性と結婚している低賃金専門の医師など)は、Roth IRA に直接寄付することができます。

少なくとも 7,000 ドル (50 歳以上の場合は 8,000 ドル) を稼ぐ人は誰でも、7,000 ドル (50 歳以上の場合は 8,000 ドル) を IRA [2024] に寄付できます。 。あなたの収入が146,000ドルから161,000ドル(夫婦共同申告で230,000ドルから240,000ドル)のMAGIを下回っている場合は、Roth IRAに直接寄付することができます。職場で退職金制度が提供されており、MAGI が 77,000 ~ 87,000 ドル (夫婦共同申告で 123,000 ~ 143,000 ドル) 未満の場合は、従来の IRA 拠出金を控除できます。このブログの読者のほとんどは仕事を通じて退職金制度を設けており、MAGI が 240,000 ドルを超えている (または間もなく持つ) ため、Roth IRA への直接拠出や従来の IRA 拠出金の控除ができないことがわかるでしょう。したがって、彼らの最良の IRA オプションはバックドア Roth IRA プロセス、つまり間接的な Roth IRA 貢献です。

既婚の医師は個人用と配偶者用の Roth IRA を使用する必要があり、通常は両方に間接的に (つまりバックドア経由で) 資金を提供する必要があります。これにより、課税年度ごとにそれぞれ 7,000 ドル (50 歳以上の配偶者には 8,000 ドル) の追加の税金保護および (ほとんどの州で) 資産保護のスペースが提供され、退職後の税金の多様化が可能になります。税金の多様化により、税金繰延 (従来型) 口座からいくら受け取るか、非課税 (Roth) 口座からいくら受け取るかを決定することで、退職者として独自の税率を決定することができます。 IRA は INDIVIDUAL Retirement Arrangement の略であるため、比例配分ルール (後述) によってあなたが Backdoor Roth IRA を行うことができなくなったとしても、必ずしも配偶者が行うことを妨げられるわけではないことに注意してください。各配偶者はバックドア ロス IRA をそれぞれ別の 8606 で報告するため、バックドア ロス IRA を行う夫婦の納税申告書には常に 2 つのフォーム 8606 を含める必要があります。

税金を夫婦別に申告する (MFS) 場合、拠出金と控除の所得制限は特に低くなります。 Roth IRA に直接拠出する機能と、あなた (またはあなたの配偶者) が 0 ドルから 10,000 ドルの間で段階的に廃止される退職金制度の資格がある場合に従来の IRA 拠出金を控除する機能の両方です。基本的に、MFS の納税者にとって最良の選択肢は、バックドア Roth IRA プロセス、つまり間接的な Roth IRA 寄付です。

実際に配偶者と同居していない場合には、これらの規則には例外があります。その場合、Roth IRAに直接拠出する能力は、2024年にMAGIが146,000ドルから161,000ドルの間で段階的に廃止されます。別居していて職場の退職金制度に加入していない場合は、収入に関係なく、従来のIRA拠出金を控除できます。 IRA 拠出金の一部または全部が控除対象となる場合でも、バックドア Roth IRA プロセスを実行できます。適切に行われた場合、税金請求額はまったく同じになり、0 ドルになります。ただし、寄付または変換のどちらにも税金がかからない代わりに、寄付に対する控除額は変換にかかる税金と正確に等しくなります。その結果、プロセス全体で同じ 0 ドルの税金請求が発生します。

Mega Backdoor Roth IRA は、通常の Backdoor Roth IRA とはまったく異なります。その名前にもかかわらず、実際には IRA ではなく 401(k) を使用して Mega Backdoor Roth IRA を実行します。これには、税引き後(Roth ではない)の従業員拠出の両方を受け入れ、サービス中の引き出し(したがって Roth IRA への変換)、またはより一般的には計画内変換のいずれかを許可する 401(k) が必要です。 Mega Backdoor Roth IRA プロセスを使用すると、最大 $69,000 (50 歳以上の場合は $76,500) を投入する可能性があります[2024] 年間で Roth 401(k) (または通常の 7,000 ドルから 8,000 ドルの寄付に加えて Roth IRA) に寄付されます。ただし、このプロセスは、この投稿で説明しているバックドア Roth IRA プロセスとは何の関係もありません。

多くの人がバックドア Roth IRA のタイミングについて疑問に思っています。

実際、Backdoor Roth IRA プロセスに従う期限は 1 つだけです。特定の課税年度の IRA 拠出は、その課税年度の 1 月 1 日から翌年の 4 月 15 日まで(延長を申請した場合でも)行わなければなりません。

変換ステップはいつでも実行できます。寄付の翌日または同日に行われる場合もあります。お勧めしませんが、投稿からコンバージョンまでに数か月、数年、場合によっては数十年待つこともできます。 Roth の変換に期限はありません。日割りルールを回避するために、ロールオーバー、またはトラディショナル、ロールオーバー、SEP、または SIMPLE IRA の変換を実行する必要がある場合は、その年の 12 月 31 日までに変換ステップを実行する必要があります。

両方の手順をできるだけ早く実行する必要があります。多くのホワイトコート投資家は、毎年 1 月の第 1 週に IRA 拠出ステップと Roth 転換ステップを実行します。これにより、それらのドルに対して発生する非課税複利の額が最大化されます。寄付からコンバージョンまでの時間を最小限に抑え、暦年内に両方のステップを実行することは必須ではありませんが、確実に事務手続きが簡素化されます。

本当に書類手続きを複雑にしたいですか?毎月 IRA に寄付し、毎月変換します。次に、12 件の寄付と 12 件のコンバージョンを毎年追跡する必要があります。しかし真面目な話、バックドア Roth IRA プロセスを通じて Roth IRA に寄付しなければならないほど十分なお金を稼いでいれば、毎年一度に寄付をするのに十分なお金を稼いでいるということになります。

はい。妻と私は 2010 年以来毎年この活動を行っており、収入がなくなるまでやめるつもりはありません。これは、私たちが年に 1 回行う投資業務の 1 つにすぎません。

バックドア Roth IRA を早期に実行するよう促す可能性がある要因の 1 つは、5 年ルールです。さて、IRA に関連する 5 年ルールは少なくとも 3 つありますが、ここで注目すべき主なルールは Roth 転換後の 5 年ルールです。この規則は、59 歳 1/2 歳未満の口座からの元本の引き出しがペナルティなしで行われるかどうかを決定します。 5 年間の期間は、変換を行う年の 1 月 1 日から始まるため、5 年より少し短くなる可能性があります。 Roth IRA の元本は通常、税金も罰金も免除されます (罰金の対象となる可能性があるのは収益のみです) が、これは 5 年間のルールが満たされた場合に限ります。

本質的に、51歳でRoth IRAの変換を行うと、59歳1/2ではなく56歳から元本を非課税かつ罰金なしで引き出すことができます。これにより、早期退職者に生活費の資金を提供することができます。 57 歳で Roth 転換を行った場合、59 歳 1/2 歳になってもその元金 (および収益) に税金と罰金なしでアクセスできます。つまり、5 歳または 59 歳 1/2 のどちらか早い方となります。

IRA 拠出金にはまったく別の 5 年間のルールもありますが、これはすべての拠出ではなく、最初の IRA 拠出を行った時点から開始されるため、ほとんどの早期退職者には適用されません。

Backdoor Roth IRA には優れた点がたくさんありますが、すべてが優れているわけではありません。

バックドア Roth IRA の主な利点は、別の退職口座が提供されることです。バックドア Roth IRA プロセスを利用すると、収益が Roth IRA への直接拠出の所得制限を超えた後でも、引き続き Roth IRA に拠出することができます。退職口座を使用すると、課税口座や非適格口座にかかる税金の抵抗がなくなり、税金が減り、投資がより高い割合で成長できるため、より早く目標を達成できます。

その税金保護は、課税口座と比較してどれくらいの価値があるのでしょうか?それは、基礎となる投資の収益、その税金効率、および口座に資金が残っている時間によって異なります。私の限界税率では、50年間で税金非効率な投資で8%を得る10,000ドルは、Roth IRAでは469,000ドルに増加しますが、課税口座では88,000ドルにすぎません。より現実的には、30 年間にわたって、節税効率の高い投資に課税口座ではなく Roth IRA を使用した場合でも、29% 多くの資金が得られることになります。

退職金口座により、シンプルな財産計画が保証されます。受益者を利用することで、そのお金は検認プロセスを経ずに済むため、相続人は手間が減り、よりプライバシーが守られ、費用をかけずにより早くお金を受け取ることができます。口座を引き継いだ後、税金で保護された成長メリットをさらに10年間延長することもできる。 Roth IRA のような退職金口座は、ほとんどの州で実質的な資産保護も提供しています。つまり、非常にまれであることは明らかですが、政策制限を大幅に超える判決が下され、上訴で減額されない場合には、破産を宣告しても退職金口座の資産を保持し続けることができます。 Roth マネーは永久に非課税であるため、毎年寄付を続けることで、退職後の税金の分散を高めることができます。

Roth IRA は、バックドア Roth IRA プロセスを介して寄付した場合でも、すべての欠点を備えた退職口座であることに変わりはありません。退職金口座では、預けられる投資が制限され、証拠金投資の使用が禁止されています。承認された例外なしに 59 歳 1/2 歳より前に Roth IRA の収益を引き出した場合、10% の違約金が発生します。

日割りルール (下記参照) のため、Backdoor Roth IRA プロセスでは、保有している従来の IRA、SEP-IRA、および SIMPLE IRA を 401(k) に変換またはロールオーバーする必要があります。自営業の収入がある場合は、その収入を税金から保護するために SEP-IRA の代わりに Solo 401(k) を使用する必要があります。バックドア Roth IRA を毎年行うと、配偶者ごとに 1 つのフォーム (IRS フォーム 8606) が納税申告書に追加されます。税務ソフトウェアを使用して独自の税金を準備する場合、ソフトウェアがプロセスを正しくレポートすることを確認するのは難しい場合があります。収入がピークの時期に、税金繰延口座を最大限に活用する代わりに(追加ではなく)バックドア Roth IRA を実行すると、蓄積される資金が少なくなる間違いとなる可能性があります。

おそらく最も重要なことは、毎年 Roth IRA に資金を入金するためのステップが 1 つではなく 2 つになったことです。このプロセスは非常に単純だと思いますが、医師たちがそれを台無しにするユニークな方法のすべてにいつも驚かされます。この記事の後半では、こうした失敗をすべて修正する方法を説明します。

はい!ほとんどの場合。毎年行うのは実際には少し面倒なだけですが、比例配分ルールを回避するために最初に別の IRA の処理を行う必要がある場合は、初年度にさらに面倒な作業が発生する可能性があります。誰かが大規模な従来の IRA を持っている場合、Roth IRA に変換する余裕がなく、401(k) をまったく持っていない、401(k) の手数料が高い、または IRA 資産が 401(k) 内では投資できないものに投資されているなどの理由で、401(k) にロールオーバーできない場合があります。雇用主が提供する退職金口座が SIMPLE IRA または SEP-IRA である場合、Backdoor Roth IRA プロセスもおそらく価値がありません。最後に、大富豪の中には、Roth 口座に年間 7,000 ドルから 16,000 ドルの余分なお金が入っても、彼らにとって大きな変化にはならないため、バックドア Roth IRA プロセスの小さな面倒さえ気にしたくない人もいます。

Roth IRA は収益に対する課税を回避することを目的としているため、当然のことながら、このプロセスには多くの税務上の影響があります。

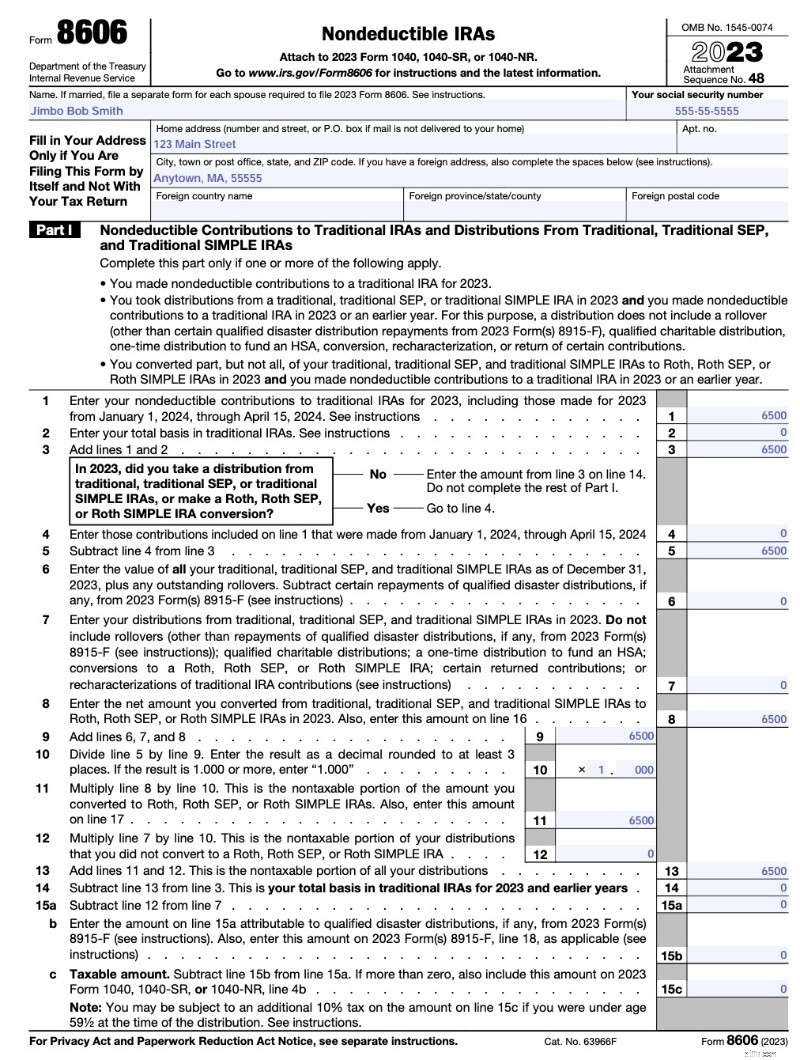

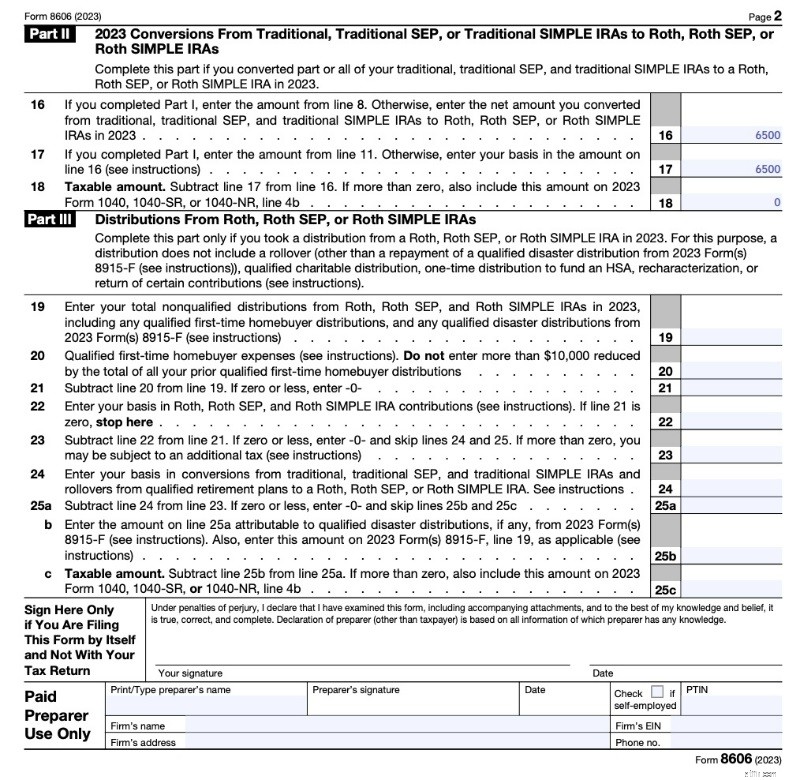

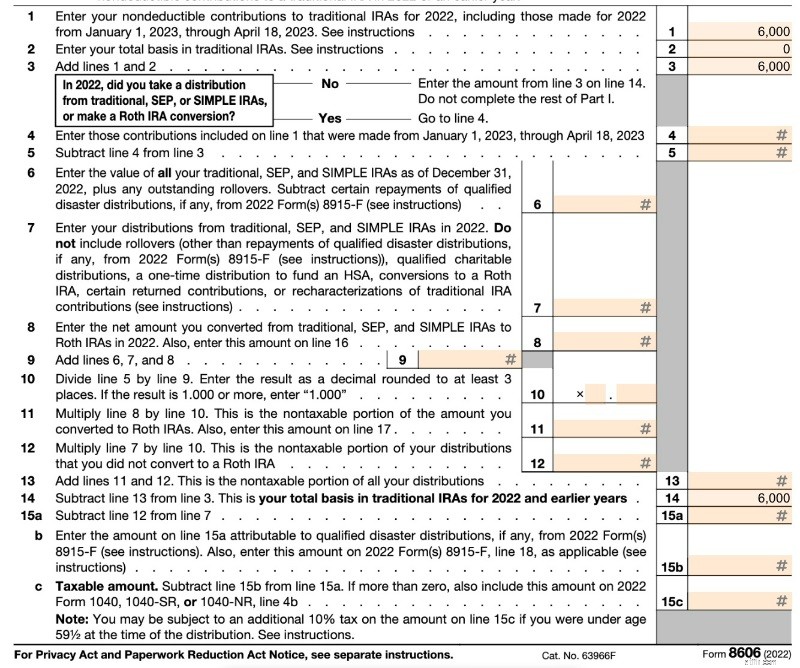

注意すべき最も重要な税金への影響は、比例配分ルールです。 Backdoor Roth IRA の失敗の 90% 以上には、投資家がコンバージョンを日割り計算されていることが関係していると私は推測します。 IRS Form 8606 (下記参照) で Roth IRA 変換を報告する場合、日割り計算が行われます。分子は換算された金額です。分母はすべての従来型、ロールオーバー、SEP、および SIMPLE IRA の合計ですが、401(k)、403(b)、457(b)、Roth IRA、または継承された IRA は含みません。したがって、税引き後の金額をRoth換算する年の12月31日までに、保有しているIRA残高で何らかの処理を行うことが重要です。この記事の後半では、このお金をどうするかについての正確な選択肢について説明します。

適切に行われた場合、バックドア Roth IRA 変換には税金はかかりません。ゼロ。灘。ジルチ。 Roth IRAに投入した資金(この場合はバックドアを介して間接的に)は、それを獲得したときに課税されますが、Roth IRAに直接寄付した場合、控除対象外のIRA変換として寄付した場合、またはその後そのお金をRoth IRAに変換した場合には課税されません。実際、再度課税されることはありません。

以前は、「ステップ トランザクション ドクトリン」と呼ばれる IRS ルールにより、IRS がバックドア ロスと問題を抱えているのではないかという懸念がありました。このルールは基本的に、一連の法的手続きの合計が違法である場合、それを行うことはできないというものです。この原則を考慮すると、この従来型 IRA から Roth へのバックドア変換が合法的な取引であるのではないかと疑問に思う人もいます。妥当かどうかにかかわらず、こうした懸念はもはや問題ではありません。 IRS は 2018 年初めに、Backdoor Roth IRA の拠出と変換ステップの間に待機期間は必要ないことを明確にしました。基本的にプロセス全体に祝福を与えています。 「ペニーとバックドア Roth IRA」で説明したように、待っていると 8606 では事態がさらに複雑になるだけです。

TurboTax でバックドア Roth IRA を適切に報告することは、残念ながらフォーム 8606 に手書きで記入するよりもさらに複雑です。これを正しく行うための鍵は、換算ステップは「収入」セクションで報告するが、拠出ステップは「控除とクレジット」セクションで報告することを認識することです。通常は最初に収入セクションを作成するため、実際には変換前に拠出を行ったとしても、拠出を報告する前に変換を報告することになります。最後に、会計士が記入したフォームを確認するのと同じように、TurboTax が生成するフォーム 8606 を確認します。

詳細についてはこちらをご覧ください:

TurboTax でバックドア Roth IRA を報告する方法

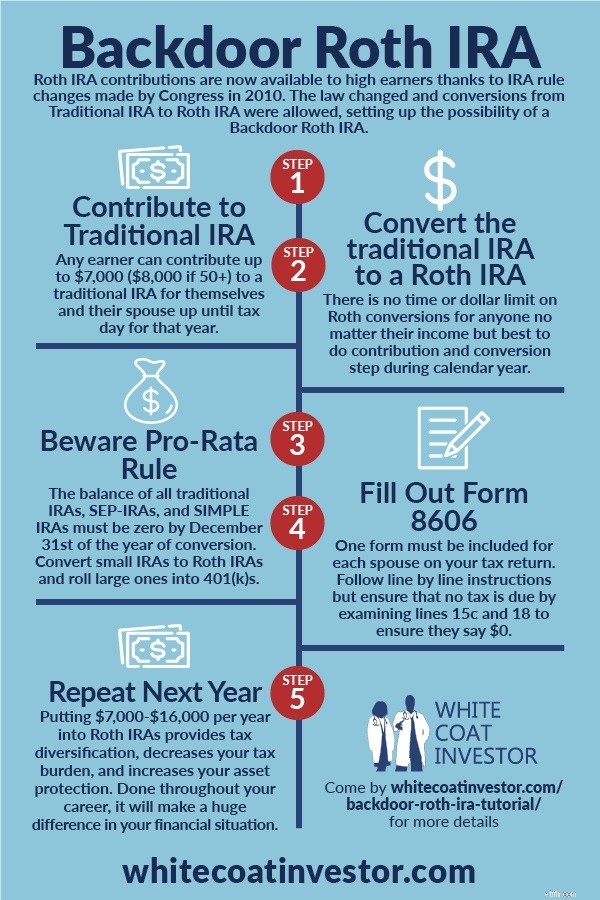

このセクションでは、Backdoor Roth IRA プロセスを実行する方法と、紙で提出するか税務ソフトウェアを使用するかにかかわらず、納税申告書でそれを報告する方法を正確に説明します。 Vanguard でバックドア Roth IRA の手順を簡単に実行することも、Fidelity でバックドア Roth IRA を完了することも、最も人気のある証券会社/投資信託会社 3 社である Schwab でバックドア Roth IRA をノックアウトすることもできます。

実際には 2 段階のプロセスですが、6 段階のプロセスと考えるのが最善です。これらのステップはすべて順番に実行する必要はありません (ステップ 1 の前にステップ 3 を実行する方が簡単かもしれません) が、すべて実行する必要があります。

自分自身と配偶者のために 7,000 ドル (50 歳以上の場合は 8,000 ドル) の控除対象外の従来型 IRA 拠出金を支払います。同じ従来の IRA アカウントを毎年使用できます。ほとんどの時間を 0 ドルで過ごすだけです。バンガードを含むほとんどのファンド会社は、口座に何も入っていないからといって口座を閉鎖することはありません。私は毎年 1 月 2 日にこれを行います。

もちろん、従来の IRA のようなアカウントは投資ではありません。スーツケースが衣類ではないのと同じです。従来の IRA に資金を投入する場合は、投資方法を IRA プロバイダーに伝える必要もあります。この場合、マネーマーケットファンドであれ決済ファンドであれ、お金は現金のままにしておきます。バンガードでは、決済基金は連邦マネーマーケットファンドです。事務手続きがより複雑になるため、寄付と変換のステップの間に利益(または特に損失)が生じることは絶対に避けたいです。利益を最小限に抑える最善の方法は、現金で残しておくことです(そしてもちろん、「ペニー」の問題を最小限に抑えるために、寄付後できるだけ早く両替を行います)。

次に、同じファンド会社で従来型 IRA から Roth IRA に資金を移管することで、控除対象外の従来型 IRA を Roth IRA に変換します。まだ Roth IRA を持っていない場合は、Roth IRA を開く必要があります。これは、Vanguard でオンラインで 1 ~ 2 分で行うことができ、従来の IRA を開くのと本質的に同じプロセスです。寄付をした翌日にこれを行います。とても簡単です。送金すると、Web サイトに「これは課税対象のイベントです」などと書かれた恐ろしいバナーが表示されます。それは本当だ。課税対象となります。しかし、すでに 7,000 ドルの税金を支払っており、稼ぎすぎているため寄付金を控除として請求できないため、税額はゼロになります。ステップ3は、基本的にはステップ1の直後に行うことができます。会社によっては即日実施してくれるところもあります。他の会社では翌日、場合によっては1週間程度まで待たされることもあります。しかし、それを実行するために何ヶ月も待つ理由はありません。

次に、Roth IRA で資金に対する投資を選択する必要があります。すでに投資を行っている場合は、それに 7,000 ドルを追加するだけです。それ以外の場合は、書面による投資計画に従って投資を選択する必要があります。書面による投資計画がまだない場合は、財務計画のその部分が完了するまで、資金を現金のままにしておくか、ターゲット 2050 退職基金または別のライフサイクル基金に積み立ててください。

SEP-IRA、SIMPLE IRA、従来型 IRA、またはロールオーバー IRA マネーを削除します。バックドア Roth IRA のメリットのほとんどが失われる可能性がある「日割り」計算 (フォーム 8606 の 6 行目を参照) を避けるために、変換ステップ (ステップ 2) を実行する年の 12 月 31 日におけるこれらのアカウントの合計はゼロでなければなりません。

これらの IRA アカウントは、次の 3 つの方法で削除できます。

<オル>バックドア Roth IRA の次の部分は、数か月後、あなた (またはあなたの会計士) が税金に関する IRS フォーム 8606 に記入するときに行われます。忘れずに実行してください。そうしないと、50 ドルの罰金が課せられます。配偶者ごとに 1 つのフォームが必要であることに注意してください:「個人退職手配」。この部分を台無しにしないようにプロに依頼したとしても、これが正しく行われていることを確認するために再確認する必要があります。顧問らは、税務担当者が不適切に行った問題の数十件を顧客が修正するのを手助けしなければならなかったと私に語った。正しく行わないと、Backdoor Roth IRA への寄付に対して 2 重に税金を支払うことになります。

ページ 1 (下) には、控除対象外の IRA からの「分配」が表示されます。お金にはすでに課税されているため、分配金の課税対象額はゼロです。行 1 は、控除対象外の寄付金です。行 2 では、昨年 12 月 31 日には従来の IRA にお金がなかったので、基礎はゼロになります (控除対象外の IRA を何年も持ち続けている場合、これはゼロではない可能性があります)。 6 行目は通常の年ではゼロです。 TurboTax ではこれを少し異なる方法で入力する場合がありますが (行 6 ~ 12 を空白のままにする場合があります)、結果は同じになることに注意してください。 13 行目は 3 行目と同じなので、納税額はゼロです。

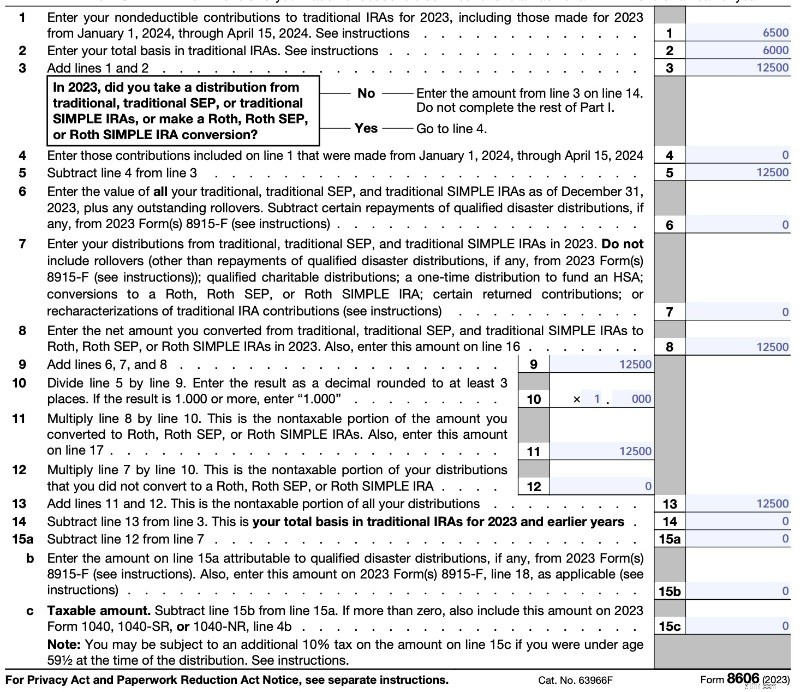

以下は、2023 バージョンの Form 8606 の例です。

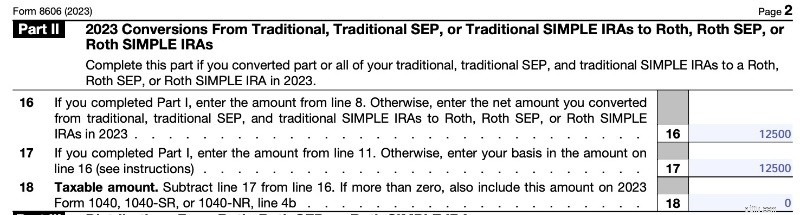

2 ページ (下記) では、Roth 変換を示しています。なぜこれを 2 回行う必要があるのかよくわかりません (8 行目と 11 行目から金額を転送してから差し引いているだけなので) が、フォームではそれが求められています。ご覧のとおり、控除対象外の従来の IRA 拠出金を利益なしで Roth に変換することは課税対象となります。ただ、税金がゼロになるだけです。

税務担当者の作業を再確認するときは、2 行目、14 行目、15c 行目、および 18 行目に注目し、それらがゼロなどの非常に少額であること、および 7,000 ドルなどの非常に大きな金額ではないことを確認する必要があります。他の Roth 変換を同時に行っている場合、または前年に寄付を行った場合 (つまり、2022 年の寄付を 2023 年に行った場合)、フォームはより複雑になる可能性があります。詳細については、以下を参照してください。

フォームには、寄付を行った日付や変換を行った日付を記入する場所がないことに注目してください。 IRA 管理者が IRS (1099-R) に送信するフォームにも記載されていません。

貢献からコンバージョンまでに一定の期間待つ必要はありません。毎年、私は1月2日にTraditional IRAで拠出を行い、翌日または数日以内にRoth IRAに変換します。そうすることで、投資資金をできるだけ早く活用できるようになり、記録の管理が簡素化されます。 Vanguard ではその日のうちに手続きを行うことができないため (他のプロバイダーでは許可してくれる場合もあります)、とにかく 1 日待たなければなりません。場合によっては1週間ほどお待たせすることもあります。アカウントに数ペニーが残っており、日割り計算されるのではないかと心配な場合は、この投稿をご覧ください:ペニーとバックドア Roth IRA。

詳細についてはこちらをご覧ください:

Vanguard でバックドア Roth IRA を実行する方法

Fidelity でバックドア Roth IRA を実行する方法

このセクションでは、バックドア Roth IRA プロセスでよくある間違いを修正および防止する方法について説明します。これらの間違いをより適切に整理するために、プロセスを上で使用した 6 つの非常に明確なステップに分割し、各ステップで考えられるエラーとその対処方法について説明します。

真剣に。それでおしまい。胆嚢摘出術ができる場合は、行うことができます。肺塞栓を適切に処理できる場合は、これを行うことができます。高血圧をうまく管理できれば、それが可能です。空洞を埋めることができれば、これを行うことができます。とても簡単です。

しかし、依然として、これら 6 つのステップのそれぞれを失敗してしまう人がいます。人々が犯す間違いを段階的に見ていきましょう。

最初のバックドア Roth IRA でよく発生するエラーは、人々が単に自分の収入が高すぎて Roth IRA に直接寄付できないことに気づいていないことです。たとえ制限を下回っていても大したことではないが、間接的に (つまりバックドアを通過するなど) 行う代わりに、Roth IRA に直接貢献します。その後、2024 年の修正調整総収入 (MAGI) が 146,000 ドルから 161,000 ドル (夫婦共同申告の場合は 230,000 ドルから 240,000 ドル) を超えていることに気付きました。次にどうするでしょうか?

この間違いを犯した場合は、Roth IRA 貢献を従来の IRA 貢献に再特徴付ける必要があります。これは基本的に、あたかも Roth IRA に貢献したことがなく、代わりに従来の IRA に貢献したかのようになります。通常、これを行うには IRA プロバイダーに電話する必要がありますが、それは大したことではありません。このセクションでは、その方法を詳しく説明します。

納税申告書の期限までにこれを行う必要があります(延長を含む)。したがって、2023 年 1 月に 2023 課税年度の IRA 拠出を行った場合、2024 年 10 月 15 日までに再特徴付けを行う必要があります。罰則も何もありません。従来の IRA に貢献したが、Roth IRA に直接貢献するつもりだった場合は、その逆も可能です。

2018 年以降、Roth CONVERSIONS の再特徴付け (コントリビューションではありません) ができなくなったことに注意してください。これにより、減税のための「Roth IRA Conversion Horserace」手法が廃止されました。

ほんの数年前まで、私は再特徴付け後にお金をRoth IRAに再変換するまでの待機期間があると考えていました。ただし、このルールはコンバージョンの再特徴付けのみを対象としたものであり、貢献ではありませんでした。再特徴付けのための待ち時間はこれまで一度もありませんでした。

もちろん、最終的な変換前に生じた利益は、最終的な変換の年の通常の所得税率で全額課税されます。

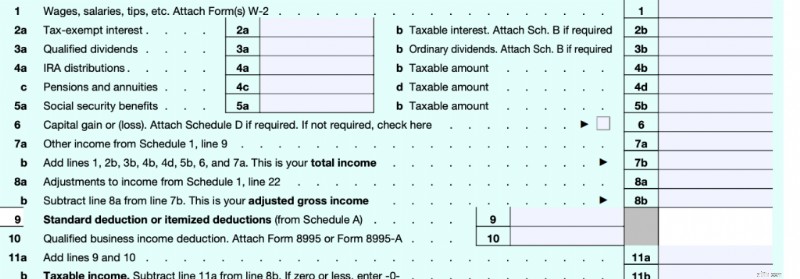

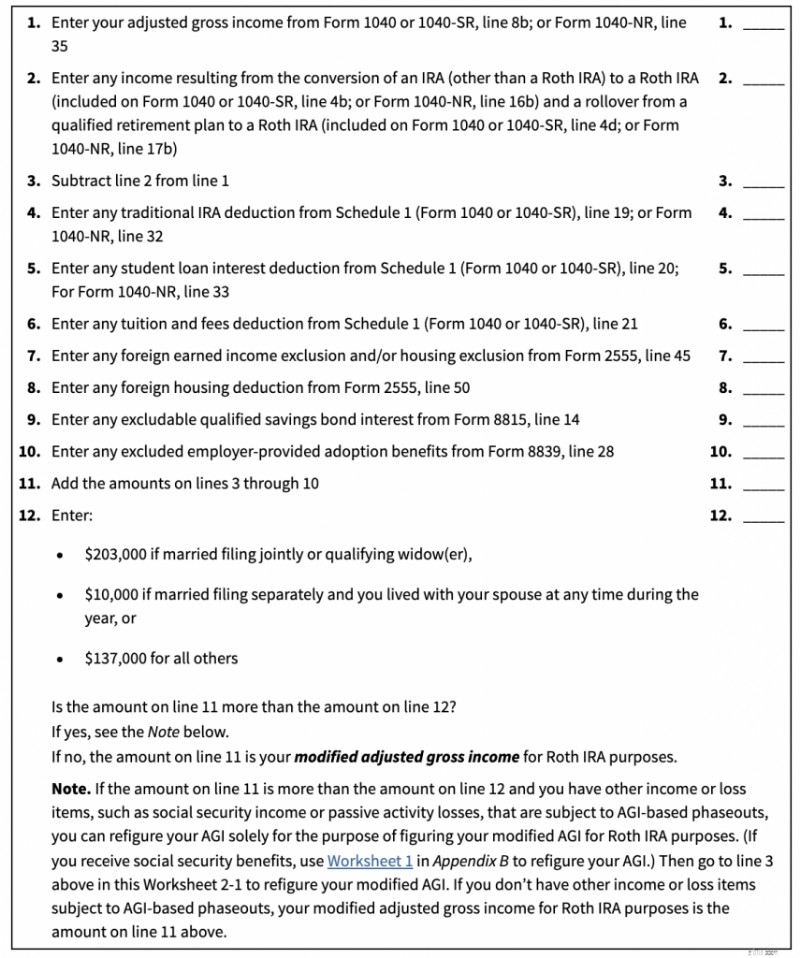

まず最初に判断すべきことは、この投稿があなたに当てはまるかどうかです。収入が一定額未満の場合は、Roth IRA に直接寄付することができます。その金額はいくつかの要因によって決まります。まず、MODIFIED Adjusted Gross Income (MAGI) です。この数字は調整後総収入 (AGI) に非常に似ています。 納税フォーム 1040 がどのように機能するかを思い出してください。

最初の収入行は 7b 行目の「総収入」です。収入について考えるとき、人々は一般的にこれを思い浮かべます。フォームの 3 番目の収入行は 11b 行目です。これがあなたの「課税所得」です。これが実際の税金の計算に基づいて計算されます。基本的には、総収入からすべての控除を差し引いた額になります。これら 2 つの間の 8b 行目は、別の収入、「調整済み総収入」です。これは、人々が「ライン以上の控除」と「ライン未満の控除」というフレーズを使用するときに話している「ライン」です。 AGI が計算される前にそれが判明した場合、それは限度を超えた減点となります。これらの控除には、自営業税、自営業の退職金制度、自営業の健康保険料、HSA 拠出金、学生ローンの利子、慰謝料、授業料、および IRA 控除などがあります。 AGI の計算後にそれが判明した場合、それは限界以下の控除となります。これらは、標準控除、または住宅ローン利息、州税、地方税、固定資産税、慈善寄付金などの項目別控除のいずれかです。 MAGI は、AGI を少し調整したものです。

以下は、Roth IRA による直接寄付に対する MAGI 制限[2024]です。 。あなたのMAGIが最初の数値を下回っている場合は、Roth IRAに直接寄付することができます。 MAGIが2番目の数値を超えている場合は、まったく貢献できません。あなたの MAGI が 2 つの数値の間にある場合は、部分的に直接貢献することができます (ほとんどの場合、これを気にする必要はありません。バックドアを通じてすべてを行うだけです)。

最初の数字に近いと思われる場合は、ご自身でRoth IRAへの寄付を間接的に、つまりバックドア経由で行ってください(従来のIRAに寄付し、その寄付をRoth IRAに変換します)。 2010 年以降、Roth のコンバージョンには所得制限がなく、従来の IRA 拠出にも所得制限はなく、控除できるだけです。

MAGI は AGI とどう違うのですか?それは非常にわずかな違いです。他にもMAGIがあることに注意してください。ここでは、Roth IRA の貢献に影響を与えるものについてのみ話します。ただし、MAGI を取得するには、AGI を取得し、そこから収入を差し引き、他の収入を加え直すだけです。これを行う方法を示すワークシートは、出版物 590 のワークシート 2-1 です。

基本的に、Roth 換算からの収入を差し引き、IRA 控除からの収入 (なぜこれがあるのかはわかりません)、学生ローンの利子 (このワークシートを使用している場合は、おそらくこれを持っていない)、授業料控除 (おそらくこれを持っていない)、いくつかのまれな海外所得/控除 (おそらくこれらを持っていない)、おそらくあまり持っていない貯蓄債券の利子、および雇用主が提供する養子縁組手当からの収入を追加します。 For most people, your MAGI =your AGI since all of these deductions are pretty rare for the folks worried about this limit for direct Roth IRA contributions. So, focus on your AGI. That means if you contributed directly to a Roth IRA but late in the year realized you probably should not have, one easy fix is to get your AGI below that limit by contributing to an HSA or a self-employed retirement plan like an individual 401(k) or SEP-IRA. Note that giving a bunch of money to charity is NOT a solution to this problem because that is a below-the-line deduction.

If you can't get your MAGI low enough, you will have to do an IRA recharacterization. As far as the IRS is concerned, a recharacterization is as though you never made the Roth IRA contribution at all but made a traditional IRA contribution instead. You don't report a recharacterization separately; you just report a traditional IRA contribution. Keep in mind as you read on the internet about recharacterizations that there used to be two types of them—a recharacterization of a Roth IRA CONTRIBUTION and a recharacterization of a Roth IRA CONVERSION. The second type was outlawed in 2018, but the first one, the one we're talking about today, is still perfectly legal. If you decide you want to undo a Roth conversion these days, you're simply out of luck. Here is how you do a recharacterization of a Roth IRA contribution:

Yup.それでおしまい。 The brokerage takes care of the rest. You can read all about all of the rules in Publication 590 Chapter 1 if you want, but that's basically what they say. Don't believe me?大丈夫。 Here are the IRS instructions:

How Do You Recharacterize a Contribution?

To recharacterize a contribution, you must notify both the trustee of the first IRA (the one to which the contribution was actually made) and the trustee of the second IRA (the one to which the contribution is being moved) that you have elected to treat the contribution as having been made to the second IRA rather than the first. You must make the notifications by the date of the transfer. Only one notification is required if both IRAs are maintained by the same trustee. The notification(s) must include all of the following information:

In most cases, the net income you must transfer is determined by your IRA trustee or custodian.

See what I mean? It's just a phone call. Any earnings that the account had in between the contribution and the recharacterization just go over with the contribution. No big deal.

You have until your tax filing date to do this. Most of the time, that's April 15 of the next year. However, the IRS is even more lenient than that. You actually can do this for an extra six months after your tax filing date, but you will have to refile your return.

If you hire somebody else to prepare your taxes, you can skip this section. If you do it yourself, you'll need to make sure you report this correctly. According to Pub 590, you report it on our old friend Form 8606.

Pub 590 says this:

Actually, that's really misleading. If you read Form 8606, you will see that the only time it ever mentions a recharacterization is to tell you NOT to put it on the form.

So, what is Pub 590 talking about? They're talking about this section in the 8606 instructions:

Reporting recharacterizations.

Treat any recharacterized IRA contribution as though the amount of the contribution was originally contributed to the second IRA, not the first IRA. For the recharacterization, you must transfer the amount of the original contribution plus any related earnings or less any related loss. In most cases, your IRA trustee or custodian figures the amount of the related earnings you must transfer. If you need to figure the related earnings, see How Do You Recharacterize a Contribution? in chapter 1 of Pub. 590-A. Treat any earnings or loss that occurred in the first IRA as having occurred in the second IRA. You can’t deduct any loss that occurred while the funds were in the first IRA . 。 。 Report the nondeductible traditional IRA portion of the recharacterized contribution, if any, on Form 8606, Part I. Don’t report the Roth IRA contribution (whether or not you recharacterized all or part of it) on Form 8606. Attach a statement to your return explaining the recharacterization. If the recharacterization occurred in 2023, include the amount transferred from the traditional IRA on 2023 Form 1040, 1040-SR, or 1040-NR, line 4a. If the recharacterization occurred in 2024, report the amount transferred only in the attached statement, and not on your 2023 or 2024 tax return.

The bottom line is that you just report this recharacterized contribution on Form 8606 as if it were the regular old non-deductible traditional IRA contribution that you should have made in the first place. You also need to include a statement. What should your statement look like? I would write something like this:

“To whom it may concern:

I made a 2024 Roth IRA contribution of $7,000 on March 13, 2024, because I didn't know about the whole MAGI limit thing when I made the contribution. After becoming smarter, I recharacterized $7,137.14 (original contribution plus earnings) to a traditional IRA on November 4, 2024. Thank you for helping our country fund its government. You're the best.

Hugs and kisses from your favorite taxpayer,

James Dahle”

Seriously, it doesn't say what has to be on the statement, just that there is one “explaining the recharacterization.” You don't even have to tell them why you did the recharacterization. If you had a loss in the account between contribution and recharacterization, no big deal. It's still as though you made a $7,000 contribution to a traditional IRA and THEN it lost money. If you were able to deduct the contribution (you probably can't) you would get a $7,000 deduction. The IRA provider may also send you a Form 5498 (which has the recharacterized amount on line 4), but you don't actually do anything with it when you file your taxes. It's just an informational return.

Here is where it gets interesting. You've now fixed your mistake in the eyes of the IRS, going from an illegal Roth IRA contribution to a legal traditional IRA contribution (that is probably not deductible for you). But you aren't done with what you meant to do, which is put money into a Roth IRA. You now need to do a Roth conversion. You do it just like you normally would as if you had contributed originally to the Traditional IRA. You can do it the very next day if you like. You can probably even do it the same day; just make sure there is a paper trail showing the money was actually in the traditional IRA at some point. There used to be a waiting period after a recharacterization before you could do a Roth conversion on that money. But that waiting period only ever applied to the recharacterization of a Roth CONVERSION (which was no longer allowed starting in 2018) and NOT the recharacterization of a Roth CONTRIBUTION. So, there is no waiting period. Just reconvert convert it and go on your merry way.

I hope this information helps you fix your mistake. Just do your Roth IRA contributions through the Backdoor going forward, and you won't have this problem again.

What happens if you LOSE money in between the contribution and conversion step? This problem is easily avoided by using an investment like a money market fund that does not go down in value for that time period. But some people fail to do so and end up losing money. When they work their way through their IRS Form 8606, they discover they have basis left over that they can then carry forward indefinitely for years! No big deal; it just makes your paperwork more complicated. Perhaps at some point in the future, you'll do a Roth conversion of tax-deferred money and this carry-forward basis will reduce the tax on that event.

What if you MADE money in the account between contribution and conversion? This actually happens most of the time, so I wrote an entire post on it called Pennies and the Backdoor Roth IRA. Technically, any money earned between the contribution and conversion step is fully taxable at ordinary income tax rates in the year of the conversion. If it is less than 50 cents, you just ignore it. If it's more, you report it on your 8606 and pay taxes on it.

If it is still in the traditional IRA, either do another tiny Roth conversion or leave it there until you do next year's Backdoor Roth IRA process. Either is fine. If you were smart and just used a money market fund and did the conversion as soon as your IRA provider allowed it (usually less than a week and sometimes as early as the next day), this won't be much money and there won't be much tax due.

If you forgot to do the conversion step for eight months afterward, it could be a huge gain on which you're unnecessarily paying taxes. No way to fix this one, just pay your “stupid tax” and move on.

Even worse than paying taxes on a huge gain is not getting the gain in the first place because you left the money sitting in cash for months. No way to fix this one either. Your “stupid tax” this time comes in the form of opportunity cost. Just get the money invested ASAP to stop the cash drag. Maybe you even got lucky and the market went down in between contribution and investment so now you get to buy low.

Some of the most common questions I get are from people who make a late contribution to a Backdoor Roth IRA. What do I mean by late? You are allowed to make an IRA contribution AFTER the calendar year ends. In fact, you have until Tax Day, usually April 15 unless you get an extension of up to six months. While it is to your advantage to contribute to retirement accounts as quickly as possible so that money can start compounding in a tax-protected way, I understand that we all have lots of good things to do with our money and sometimes this gets pushed back into the next calendar year. All it really does is complicate your paperwork a bit.

For example:if you made your 2023 IRA contribution in April 2024, instead of reporting both the contribution and the conversion on your 2023 taxes, you would report only the contribution there. The conversion would be reported on the taxes for the year you did the conversion, i.e., your 2024 tax return due in April 2025. Your 2023 IRS Form 8606 becomes a little simpler and your 2024 IRS Form 8606 becomes a little more complicated. Not a big deal if you can follow the simple instructions.

What confuses people, however, is the pro-rata rule. This is the rule that says you need to empty your traditional IRA by December 31 of the year you do the conversion. Since these folks have never filled out a Form 8606 (or apparently read the instructions), they assume that for a 2023 contribution they need to have a balance of $0 at the end of 2023, even if they didn't do the conversion step until 2024. That's simply not the case. The pro-rata rule isn't applied until the year of the conversion, i.e., December 31, 2024.

How do you empty those IRAs? You usually have two choices.

<オル>How large is large and how small is small? It's going to vary by the person and how much disposable cash they have. Most would consider an IRA under $10,000 to be small and an IRA over $100,000 to be large. In between, it's a personal decision as to which would be better for you.

What if you screwed this one up? Your Backdoor Roth IRA conversion step just got pro-rata'd. There is a tax bill associated with that because most of your conversion was of tax-deferred money rather than post-tax money like it was supposed to be.

The fix for this is going to vary by the individual, but the easiest fix is to simply convert the entire IRA to a Roth IRA now, so you end up getting all your post-tax money into that Roth IRA. Another possible fix is to figure out a way to separate your basis in that IRA, roll the tax-deferred money into a 401(k), and then convert the basis left behind in the IRA.

Do yourself a favor and just empty the darn IRA by December 31. Keep in mind that this is usually not an instantaneous process, so don't put it off until you're on holiday break at the end of the year.

Both individual taxpayers and professional tax preparers screw up IRS Form 8606 all the time. In fact, some of them haven't even heard of a Backdoor Roth IRA. (Incidentally, this is one of the best questions to ask while interviewing a potential tax professional—”How many Backdoor Roth IRAs did you help last year?”)

The usual fix to this error is to file a 1040X (Amended Tax Return) and a new Form 8606. You can do this for the last three years if necessary. If you didn't file Form 8606 at all, you'll definitely want to do this. The key is to check lines 15c and 18 on Form 8606. They should both be a number very close to zero if the form is being completed correctly.

The tax preparer should NOT be filing Form 5439. If you did Steps 1-5 right, this form probably doesn't belong in your tax return.

A lot of people wonder about the 1099-R sent to them by their IRA provider and worry that it was done wrong and that it will cause them to pay taxes they shouldn't have to pay. Sometimes the form was filled out wrong, but mostly this is just a lot of anxiety. What gets people anxious is finding something on Line 2a “Taxable amount.” As long as the box on Line 2b is also checked “Taxable amount not determined,” you're golden.ご心配なく。 If it is not, have the IRA provider send you a new, correct form—either with $0 in 2a or the box in 2b checked (usually the latter). Here's what mine from a few years back looked like from Vanguard:

Note that Box 2b is checked, even though a taxable amount of $5,500.07 is being reported to the IRS.

Again, if you're not sure how to enter this into TurboTax, check out my TurboTax tutorial.

Need more help with a Backdoor Roth IRA? I wish Congress would just lift the rule against direct Roth IRA contributions for high earners and save us all this hassle, but who knows if that will ever happen.

While it is “cleaner” to make your contribution and your conversion all in the same calendar tax year, you can make your contribution up until your tax filing date of the next year. The key to filling out the 8606 correctly when you make a contribution after the calendar year is to recognize that the contribution step is reported for the tax year and the conversion step is reported for the calendar year. So imagine you did the following during the calendar year 2023:

Your forms would look like this:

Note that all this serves to do is report basis for the next year. No tax is due. Since no conversion step was done during the calendar year 2022, you only have to fill out lines 1-3 and 14.

Note that you've got to do all of Part I plus Part II for this year because you did the conversion step, unlike last year (2022). Let's go through this line by line.

You have until tax day (generally April 15, but as late as October 15 if you file an extension) of the following year to make your traditional IRA contribution. There is no deadline for the Roth conversion step; it can be done at anytime. Make sure you fill out the paperwork properly according to the section above about late contributions.

はい。 Just remember to report last year's contribution on last year's Form 8606 and this year's contribution and the conversion on this year's Form 8606.

No. Only traditional IRAs, rollover IRAs, SEP-IRAs, and SIMPLE IRAs count. See line 6 of Form 8606 for details.

はい。 All IRAs count toward the pro-rata calculation.

If it is small, convert it to a Roth IRA along with this year's traditional IRA contribution and pay the tax due on it. If large, try to roll it into your employer's 401(k) or if you have self-employment income, into your individual 401(k).

The easiest solution is to convert the entire IRA, SEP-IRA, or SIMPLE IRA that caused the pro-ration and is now composed of both pre-tax and after-tax money. That is also the most expensive solution. A harder solution that may save you some taxes involves isolating the basis in that IRA by rolling the rest of the account into a 401(k) and then convert just the basis to a Roth IRA.

If you put it into a traditional IRA it is going to cause any future Backdoor Roths to be pro-rated. Better options include leaving it where it is; rolling it into your new employer's 401(k) or 403(b); rolling it into your individual 401(k); or, if it is small, just converting the whole thing to a Roth IRA.

In 2024, you are allowed to contribute $7,000 ($8,000 if 50+) per year for you and $7,000 ($8,000 if 50+) for your spouse. This includes all contributions to traditional and Roth IRAs. Rollovers/transfers do not count toward the annual contribution limit. [Visit our annual numbers page to get the most up-to-date figures.]

While in the traditional IRA for a day or two, leave it in cash. Once it is in the Roth IRA, invest it according to your written investing plan. If you don't have one, get one, but in the meantime it would be a good idea to put it into a lifecycle fund such as a Vanguard Target Retirement Fund.

You can use the same ones each year.

The Backdoor Roth IRA process leads to more tax-free retirement account money for doctors and other high-income professionals. If you follow the simple steps outlined above, you will pay less in taxes, boost your returns, facilitate your estate planning, and increase your asset protection. Most members of The White Coat Investor community do these every year, and you should too.

どう思いますか? Are you doing Backdoor Roth IRAs? Why or why not? Any questions about it?

[This updated post was originally published in 2014.]