不動産計画は、私たちのほとんどが可能な限り後回しにする雑務です。通常、私たちはそれが面白くなく、お金がかかると感じますが、さらに悪いことに、それは私たち自身の死と向き合わなければならない可能性があります。しかし、これは資金計画の重要な側面であり、下手に(またはまったく行わないで)行うと、相続人に大きな混乱を引き起こす可能性があります。

遺産とは、あなたが亡くなったときに残すものです。それにはあなたのお金と持ち物のすべてが含まれます。

プロベートとは、遺言の正式な証明を意味し、遺産(故人の財産)が債権者に返済し、有効な遺言書に指定されているとおりに遺産の資産を分配する法的手続きです。それは費用と時間がかかる可能性があり、多くの場合、訴訟費用や管理費として遺産のかなりの部分を消費し、数か月、場合によっては数年に及ぶこともあります。不動産計画の多くは、このプロセスを可能な限り回避することを目的としています。

不動産計画は、次のことを保証するプロセスです。

これは、単純で安価な作業である場合もあれば、適切に完了するために費用のかかる専門家の支援が必要な場合もあり、すべては個人の状況と希望に応じて異なります。

ほぼすべての人が、少なくとも少しの不動産計画を行う必要があります。確かに、多額の資産(20,000ドル以上)を取得し、自分が死んだときにその財産を誰に渡すかを気にしている場合は、相続計画が必要です。同様に、子供が 1 人でもいる場合は、少なくとも何らかの財産計画を行う必要があります。

遺産計画には多くの作業が必要ですが、主な作業は、死亡時または無能力状態になったときに関係するさまざまな法的文書の準備です。

正式には遺言書として知られる遺言書は、通常、ほとんどの人が最初に必要とする財産計画ツールです。人が「無遺言」(遺言書なし)で死亡した場合、その財産は州法に従って、通常は配偶者、または適用されない場合は子供に分配されます。近親者以外の方法で財産を分配したい場合は、遺言書が必要です。遺言書のもう 1 つの重要な役割は、自分が亡くなった場合に子供の世話をしてくれる人を指名することです。純資産が大幅にマイナスの医学生であっても、子供がいる場合は遺言書が必要です。

ほとんどの医師がよく知っている遺言書の種類の 1 つがリビングウイルです。これは通常、自分の医療について自分で決定できなくなった場合に備えて、あなたの希望を決定します。また、通常、あなたができないときに医療上の決定を下す医療代理人の名前も付けられます。 「蘇生禁止命令」もリビングウィルの 1 つの形式です。

私は日常的にリビングウイルを目にしますが、あまりにも曖昧なため、一般的には役に立たないと感じています。彼らは、私が下す必要がある実際の決定については決して言及していないようです:患者は抗生物質を望むでしょうか?点滴液?プレッサー?挿管/換気?心肺蘇生法?近親者に医療に関する決定をさせたくないのでなければ、リビングウィルの必要性はそれほど高くないと思います。おそらく、リビングウィルの最も重要な側面は、自分自身で医療に関する決定を下すことができなくなった場合に、どのようにしてもらいたいかについて、家族と簡単に話し合うことです。 「私を一週間以上人工呼吸器をつけたままで放置するのはどうかと思います」など。

それにもかかわらず、弁護士に相談したり、オンラインの遺産計画サービスを利用したりする場合でも、通常はこの文書が同封されます。比較的安価で簡単なのでやってみると良いでしょう。しかし、あなたの愛する人たちと必ずそれについて話し合ってください。そうしないと、いざ使用するときにその存在にさえ気づかない可能性があります。

たとえリビングウイルや医療委任状を省略したとしても、それができない場合には、信頼できる家族、友人、またはアドバイザーにお金の管理を任してもらう価値はあるでしょう。これは永続的な財務委任状と呼ばれます。研究によると、私たちの家計管理能力は50代でピークに達します。私たちは皆、10年、20年前には決してしなかったであろう、お金を使った愚かなことをした高齢者を知っています。委任状の文書は、一般的 (すべてを網羅) かつ生涯 (耐久性) のものにすることも、時間と範囲の両方を制限することもできます。たとえば、子供たちを祖父母に預けて旅行する場合、私たちは子供たちの世話をするために限定的な委任状を提供することがあります。経済的および医療上の委任状は同一人物である必要はないことに注意してください。

これはあなたの死の際に残しておける素晴らしいものですが、実際には法的文書ではありません。これは、故人から愛する人や遺言執行者に、知っておいてほしい情報を説明する単なる手紙です。個人的なメッセージを含めることも、簡単な指示だけを含めることもできます。多くの場合、次のような情報が含まれます。

このレターの最も重要な点は、常に最新の状態に保つことです。

これは、意向表明書の一部である場合もあれば、別の文書である場合もあります。次の文書をリストに含めることを検討し、その場所を必ず書き留めてください。

取消可能な生前信託は基本的に検認を回避することを目的としており、税金を回避したり債権者から資産を保護したりすることを目的としたものではありません。金銭と資産は信託に預けられ、あなたの死亡時に受託者が信託文書に従って相続人に資産を分配します。検認は必要ありません。もちろん、信託財産には相続税がかかります。取消不能な信託に対する取消可能の主な利点は、必要に応じて資産を管理および使用でき、いつでも「取り消す」ことができることです。資産は、信託の名前でタイトルを変更することによって信託に「入れられ」ます。取消可能な信託は、死亡時のプライバシーを提供し(検認は公的手続きであるため)、大規模な遺産に対して大幅な時間と費用を節約できます。ほとんどの医師は、受益者指定のない資産のほとんどを、死亡時までに取り消し可能な信託として受益者として記載する必要がある人もいるはずです。取消可能な信託の収入に課せられる税金は、通常、個人の申告書に送られます。

これらの信託には、検認を回避できるという点で、取消可能な生前信託の主な利点があります。また、相続税を回避できるという利点もあり、所得税も回避されることが多いです。これは、資産を取消不能な生前信託に預けるということは、本質的にそれらを譲渡することになるからです。資産やそれが生み出す収入を使用できなくなります。収入に対する税金は、信託または相続人が支払う必要があります(相続人がより低い税金階層にある場合、これが有利になる可能性があります)。

このような信託には、絶対に必要ないとわかっているお金だけを預けるべきです。取消不能とはまさにそのことを意味します。信託に預けた資金には贈与税法が適用されることに注意してください。贈与税や相続税を課さずに、毎年どれくらいの金額を信託に預けることができるかを判断するには、あなたの州の経験豊富な弁護士に相談してください。取消不能な信託は優れた資産保護ツールでもあることに留意してください。資産はもうあなたのものではないので、債権者がそれを差し押さえることはできません。取消可能な信頼にはこの利点がありません。

未成年の子供が成人したときに相続財産全体を権利として取得したくない場合、または障害のある成人の子供がいる場合は、資産が適切に使用されることを保証するために、ある種の浪費信託が必要になる場合があります。これらのドキュメントには非常に柔軟性があり、ここで必要なほぼすべてのことを行うことができます。墓場から彼らの人生を支配しようとすればするほど、より多くの複雑な問題が発生する可能性があることに注意してください。また、家族の小屋、墓地、または同様の多世代の財産を管理するために信託が必要になる場合もあります。子供の元配偶者から資産を保護したい場合もあります。婚前契約がなければ、信託が唯一の方法である可能性があります。

これは遺言書の重要な側面であり、別個の文書ではありません。これは、あなたの死後に未成年の子供を誰が世話するか(後見人)、また、子供が成人するまで誰が彼らに代わって残された財産を管理するか(後見人)を規定します。これらは同一人物ではありません (そしておそらく同一人物であるべきではありません)。難しい決断であることは承知していますが、最も重要なことは決断を下すことです。後でいつでも変更できます。潜在的な保護者が子供についてどう感じているか、そして子供が潜在的な保護者についてどう感じているか、両方を必ず考慮してください。理想的には、彼らはお互いを愛し、あなたとまったく同じように子供を育てるでしょう。経済状況、職業、身体的および精神的能力、宗教、およびお子様の将来の人生に影響を与える可能性のある生活のその他の側面を考慮してください。通常、カップルではなく、1 人だけをリストします。成人に達する前または後にお金の使い方に制限を設けたい場合は、後見人を指名する遺言書だけでなく、信託が必要になります。最後に、指定した人に必ず自分の決定を伝え、その決定に同意してもらうようにしてください。

書類の準備以外の財産計画のもう 1 つの重要な側面は、すべての退職金口座、年金、生命保険契約の受取人の指定が正しいことを確認することです。これらの資産はすべて、信託を使用しなくても検認の範囲外で譲渡されます。これらを定期的に確認し、出生、死亡、結婚、離婚などの主要なライフイベントに応じて更新してください。おそらく、生命保険や退職金口座が元配偶者に渡されることを望まないでしょう。

ほぼすべての種類の銀行口座を、誰にでも「死亡時に支払う」口座として指定できます。この方法では、あなたが亡くなったときに、あなたの指定された人があなたの死亡の証拠(通常は死亡証明書)を持って銀行に行き、検認を行わずにお金を回収するだけです。株式、債券、投資信託などの有価証券、さらには証券口座全体を「死亡時送金」として登録することもできます。その最も良い点は、これらの有価証券の基礎があなたの死亡日の時点で更新されるため、相続人がすぐにそれらを売却した場合、キャピタルゲイン税が課されないことです。カリフォルニアとミズーリの 2 つの州では、自動車でもこれを行うことができます。

遺産計画のポイントは、未成年の子供、お金、持ち物を、手間や出費、税金を最小限に抑え、最大限のスピードとプライバシーを保ちながら、希望する人や組織に確実に届けることです。上記で説明した文書を実装することで、通常、適切な後見と資産の適切な相続が保証されます。ただし、検認はできる限り避けて、納税額をできるだけ少なくしたいと考えています。次にこれら 2 つのトピックについて説明します。

検認は費用がかかり、公開され、時間がかかる場合があります。数万ドルの費用がかかる可能性があり、相続人は1年以上もたらされるものを受け取れない可能性があります。今少し計画を立てることで、後で多くの手間を省くことができます。検認は州法に準拠する州固有のプロセスであるため、州ごとに異なることが予想されます。しかし、一般に、検認を回避する方法はたくさんあり、そのうちのいくつかはすでに上で説明されています。これらには以下が含まれます:

退職金口座、年金、年金、生命保険契約に最適です。

場合によっては、検認を回避する手間と費用よりは検認を通過する方が良い場合もありますが、遺産計画の目標の 1 つは、原則として、検認を回避することです。これを行うには多くの方法があります。主なものの 1 つは、退職金口座の受取人を指定することです。たとえば、IRA の受益者があなたの息子である場合、あなたの死亡後、息子は検認を経ることなく収益を受け取ることができます (もちろん、相続税や相続税は引き続き課税され、従来の IRA の場合は最終的には所得税の対象となります)。

思い出してください。401(k) または IRA を開設するとき、受益者を尋ねられました。配偶者以外の人を選択する場合は、配偶者の書面による承認が必要になります。離婚したり、受取人と疎遠になったりした場合、または単に考えが変わった場合は、忘れずに戻って口座の受取人を変更してください。苦い離婚の後、元配偶者が、被相続人が故意に残したはずのない退職金口座を手元に残すことになることがよくあります。

共同財産州 (アリゾナ、カリフォルニア、アイダホ、ルイジアナ、ニューメキシコ、ネバダ、テキサス、ワシントン、ウィスコンシン、場合によってはアラスカ) にお住まいの場合は、退職金口座の半分以上を配偶者以外の人に譲渡することはできないことに注意してください。口座の半分は配偶者のものとみなされます。

生命保険金は検認を経ずに受取人に渡されます。一般に、あなたの死後、相続人がお金を得る最も簡単な方法の 1 つです。保険会社は死亡診断書を受け取ってから 1 週間以内に保険金を支払う場合がありますが、ほとんどの場合、死亡後 2 か月以内に支払われます。

銀行口座、投資口座、さらには州によっては自動車にも最適です。

信託に資産を所有させると、検認は行われなくなります。これは、家庭、自動車、ボート、飛行機、電動玩具、銀行口座、さらには投資口座にとっても優れたソリューションです。

死後は取消可能な信託と同じように機能しますが、死亡前には追加の制限と利点がいくつかあります。

共同テナントなど、共有所有権の一部の形態では検認も回避されます。たとえば、不動産の所有権が適切に設定されていれば、それを所有している人は、検認を経ることなく、不動産全体を自分の名前に簡単に譲渡することができます。

これを不動産計画ツールとして使用する場合は注意が必要です。たとえば、子供を共同所有者として銀行口座に追加するには、いくつかの問題が伴います。

資産の所有権を設定する方法によって違いが生じる可能性があるため、不動産や車などの資産の所有権を設定する場合は、そのプロセスに不動産計画の影響があることを認識してください。

共同体財産州では、共同体財産が検認される場合もあれば、されない場合もあります。これが行われている州 (アリゾナ、ネバダ、テキサス、ウィスコンシン) では、資産が検認を受けないようにするために、「生存権あり」という文言を追加できます。

投資や自宅などの不動産など、値上がりする資産を共同所有する場合には、追加の所得税の問題が発生します。あなたが死亡すると、相続人は通常、あなたの死亡日の資産価値に応じてステップアップの基礎を取得します。ただし、相続人が共有所有者の場合は、そのような根拠は得られません。そのため、最終的にその資産が売却された場合、非常に多額の、しかし完全に不必要な所得税の請求が発生する可能性があります。したがって、一般的なルールとして、銀行口座や車の相続人と共有所有権を持つことは問題ないかもしれませんが、投資や自宅の共有所有権を持つことはほとんど良い考えではありません。

場合によっては、遺産の価値が一定の金額を下回っている場合、相続人に相続財産が遺言書で指定されている旨の宣誓供述書に記入してもらうことで検認を回避できることがあります。ほとんどの医師の遺産は、死亡時にこれらの制限を超えています。

遺産計画は、検認を回避することに加えて、相続税、別名贈与税、相続税、そして「死亡税」を回避することに重点を置いています。故人、遺産、相続人が支払う所得税を最小限に抑えることも共通の目標です。

残念なことに、相続税法は変動の標的となる可能性があります。過去 10 年間に法律事務所が 6 回変更され、不動産計画弁護士には十分な収入が得られましたが、全員には大きな混乱が生じました。 2024 年の時点で、相続税が適用される前の連邦控除額は個人あたり 1,361 万ドルです[最新の数字を入手するには年間数値ページをご覧ください] 。あなたの死亡時の遺産総額がその額を下回っている限り、連邦相続税を支払う義務はありません。 [2024]結婚している場合、免除額は 2 倍の 2,722 万ドルになります。 , そしてこの金額は実際にはポータブルであり、死亡した最初の配偶者のすべての資産が税金を支払うことなく2番目の配偶者に渡され、2番目の配偶者は約2,800万ドルの連邦遺産を非課税で相続できることになります。現行法では免除額もインフレに連動しているため、約20年ごとに2倍になるはずだ。ただし、現在の法律では、議会が延長措置を講じない限り、免除は実際には 2026 年 1 月 1 日に半分になることに注意してください。

各州も相続税ゲームに参加することを好み、さらに悪いことに、一部の州は連邦控除額を使用しません。これらには、コロンビア特別区、ロードアイランド、コネチカット、イリノイ、ハワイ、バーモント、オレゴン、メイン、ワシントン、ミネソタ、ニューヨーク、メリーランド、マサチューセッツが含まれます。たとえば、ニューヨークに住んでいる場合、2022 年の州税免除額は 611 万ドルで、最高税率は 16% です。これらの各州の相続税の免除と税率は、ここで調べることができます。

アイオワ州、ケンタッキー州、メリーランド州、ネブラスカ州、ニュージャージー州、ペンシルベニア州は相続税よりも相続税の使用を好みます。これは、税金が遺産そのものではなく、相続を受け取る人に課されることを意味します。通常、配偶者はこれから免除されますが、州によっては直系卑属も免除されます。ここであなたの州に相続税があるかどうかを確認できます。

不動産計画を立てる際には、所得税も関係します。死亡前にあなたが支払ったのか、死亡の年に相続人が支払ったのか、あなたの死後に相続人が支払ったのかにかかわらず、すべての所得税を考慮する必要があります。また、所得税計画が相続税に与える影響、またはその逆も考慮する必要があります。

最も重要な所得税計画は、死亡時基礎額の引き上げを中心に展開されています。相続人はあなたの基礎(つまり、あなたが投資に支払った金額)を継承しません。あなたが亡くなった日の資産価値がステップアップされます。したがって、10万ドルで不動産を購入し、死亡時には100万ドルの価値があり、相続人がすぐにそれを売却した場合、所得税はかかりません。死亡時の基礎額が増額されなければ、彼らは90万ドルの税金を支払うことになるでしょう!原則として、高齢者、特に健康状態の悪い人が、低い基準で何かを販売し、それに所得税を支払うことは悪い考えです。たとえそれまで生活するためにお金を借りなければならなかったとしても、その資産を子供たちに残した方がはるかに良い場合が多いのです。死亡前に資産を売却する必要がある場合は、基準の高い資産を優先的に売却する必要があります。

所得税へのもう 1 つの重要な影響は、配偶者の一方が死亡した後、残りの配偶者が単身者として税金を申告することになり、通常はより高い税率で納税することになります。したがって、配偶者両方がまだ生きている間に所得税の一部を前払いすることが合理的です。

ほとんどの相続税計画は、連邦および州の相続税免除を最大限に活用することを中心に展開されます。理想的には、適切な計画により相続税が完全に免除されますが、非常に大きな財産を持っている場合でも、支払う金額を最小限に抑えることができます。

ほとんどの書類と同様に、あなたの遺産の価値が相続税免除額よりも低い場合、相続税はまったくかかりません。お金を使ったり、譲渡したりすることで、不動産の価値を下げることができます。いつでも慈善活動に任意の金額を寄付することができ、寄付により所得税の優遇措置が受けられる場合もあります。ただし、個人で寄付できるのは $18,000 [2024] のみです。 それ以上の金額を寄付することもできますが、年間 18,000 ドルを超える金額の場合は贈与税申告書を提出する必要があり、相続税控除が侵食され始めます。それがなくなると贈与税の支払いが始まりますが、これは相続税を前払いするのと本質的に同じです。あなたは子供に 18,000 ドル、子供の配偶者に 18,000 ドルを寄付することができ、あなたの配偶者も同様に寄付できることに留意してください。つまり、お二人は贈与税に悩まされることなく、結婚している子供たちに毎年 68,000 ドルを贈与することができます。

資産が値上がりする可能性がある場合は、その前に手放した方がよいでしょう。そうすれば、その感謝金はすべてあなたの財産に残り、相続税の対象となることはありません。これは、相続人に資産を譲渡するだけで直接行うことも、取消不能信託、家族有限責任組合 (FLP)、または家族有限責任会社 (FLLC) を使用して間接的に行うこともできます。

IRS は不動産の規模を評価する際に、税引き前のドルと税引き後のドルが同等であると見なすため、ロス換算により不動産の規模を減らすこともできます。

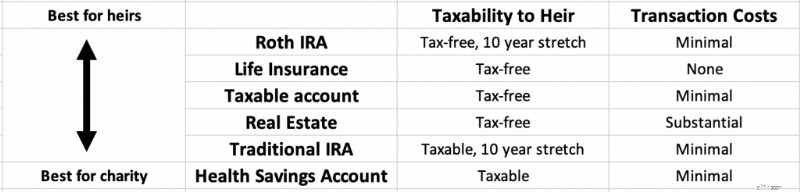

原則として、以下のリストの上部にある資産は相続人に残すのが最善であり、リストの下部にある資産は慈善団体に残すのが最適です。慈善活動に何も残すつもりがなく、相続人が受け取るものを最大限にしたいのであれば、ボトムアップで支出するのが最善です。

Roth 口座の税制上の優遇措置は、相続人によってあなたの死後さらに 10 年間延長されることがあり、通常、多額の資産保護も受けられます。

生命保険 あなたが亡くなってからわずか数週間以内に、非課税の現金として相続人に引き継がれます。

課税対象の投資 死亡時にベースアップの恩恵を受けるため、売却に多少の費用がかかる場合がありますが、あなたの死後、相続人が迅速に非課税の現金に変換することができます。

一方従来の IRA と 401(k) は 相続人は 10 年間延長でき、Roth IRA と同様に資産保護を受けることができます。これらは依然として税引き前のお金であり、引き出しはすべて相続人にとって全額課税所得となります。

税引前資産の場合 慈善団体に寄付されると、慈善団体が全額を受け取り、誰もそのお金に対して税金を支払いません。 Health Savings Account (HSA) も、相続人による増額ができないため、慈善団体に任せるのが最適な税引き前のお金です。

生命保険金には所得税がかかりません。あなたが死亡したときに、100万ドルの生命保険金を妻、子供、または愛犬に残したとしても、誰一人として所得税を1セントも支払うことはありません。したがって、生命保険は、終身保険などの終身保険であっても、資産計画に優れたツールとなる場合があります (ただし、適切な投資計画に役立つことはほとんどありません)。収益は相続税の支払いに使用したり、売却が難しい家族経営の事業や農場に流動性を提供したりすることができます。ただし、故人/遺産が保険契約の所有者である場合、その収益には引き続き相続税が課せられます。

これを回避する唯一の方法は、誰かまたは何か他のものにポリシーを所有させることです。子供に保険を所有させ、毎年保険料を贈与することもできますが、取消不能な信託によって所有される方がはるかに一般的です。本質的に、この戦略には、贈与税額 (2023 年には 1 人あたり年間 18,000 ドル) をわずかに下回る年間保険料で生命保険に加入することが含まれます。保険料は毎年取り消し不能の生前信託に積み立てられ、生命保険の購入に使用されます。死亡すると、その収益は所得税と遺産税の両方で相続人に相続されます。生命保険の現金価値や死亡保険金の増加に対して税金がかからないため、非常に節税効果の高い富の継承方法となります。

しかし、節税効果が追加コストや生命保険の「投資」の相対的に低い収益よりも大きいかどうかを判断するには、かなりの数値計算が必要になる場合があります。いずれにせよ、その不動産が相続税の対象にならないのであれば、それはおそらく良い考えではありません。保険の営業マンはあらゆる機会にこれらのメリットを強調することを忘れないでください。定期生命保険は、ほぼすべての人にとって今でも最高の保険です。相続税の問題が予想される場合は、考慮すべき点であることに注意してください。購入を待っていると、その年齢で保険に加入できないリスクが高まりますが、その時点で保険に加入できないことが判明した場合に使用できる他の不動産計画ツールがあります。

不動産計画を準備する際には、具体的な手順をいくつか行う必要があります。

<オル>財務計画と同様に、最初のステップは、自分が今どのような状況にいるのか、何が最も欲しいのかを把握することです。

あなたの純資産は、おそらく個人の財務において知っておくべき最も重要な数字ですが、相続計画に関しては、相続税の問題があるかどうかを決定するものです。あなたの純資産が連邦および該当する州の相続税免除額よりも少ない場合、相続税はかかりません。

あなたの純資産は、あなたが所有しているすべてから借りているすべてを差し引いたものです。銀行口座、自宅、退職金口座、証券口座、診療所やその他の事業の価値、賃貸物件などのすべての資産を合計します。ほとんどの目的には、妥当な見積もりで問題ありません。厳密に言うと、車、おもちゃ、家具、衣類、家庭用品なども合計する必要がありますが、実際的な観点から見ると、ほとんどの人は大きなものだけを含めています。次に、すべての負債を合計します。これらには、住宅ローン、学生ローン、クレジット カード、自動車ローン、その他の借金が含まれます。資産から負債を差し引くと、それが純資産となります。

純資産を計算するときは、すべての資産と負債のリストを作成します。この文書は、あなたとあなたの弁護士が適切な遺産計画を立てるのに役立ちます。含める:

人生では、特に未成年の子供がいる場合は、物やお金よりも人々が重要です。あなたが早すぎる死を迎えた場合の彼らへの計画をリストアップしてください。含める:

遺産法は州ごとに異なるため、州の弁護士が必要です。非常に基本的な不動産計画は、オンラインの弁護士/サービスを使用して自分で行うことができますが、このサイトを読んでいるほとんどの専門家は、最終的には本物の弁護士の向かいに座ってこれを完了したいと思うでしょう。この弁護士は、プロセスの理解を支援し、書類の草案を作成し、質問に答え、必要に応じて計画を定期的に更新します。また、あなたの死後、相続人のための管財人やリソースとしても機能します。

オンライン法律サービスは数十あります。最もよく知られているのは Legal Zoom ですが、他には Rocket Lawyer、LegalShield、Zen Business などがあります。 Some specialize in business formation such as LLCs and corporations, but most will at least do a basic will and perhaps even a trust. They can probably handle a basic “I love you” will that names a guardian and conservator for your children, but by the time you start thinking about trusts, it's probably time to find a local attorney.

Attorneys generally charge by the hour, perhaps $250-$350 per hour. So the cost of your estate planning depends on the complexity of your estate. If your situation is really complex, it will cost you thousands or even tens of thousands to form trusts, family-limited partnerships, and more. But a simple will or power of attorney may cost less than $200. The initial meeting is often free, so feel free to shop around a bit. It can help you keep costs down if you did your research, knew exactly what you want before you arrive, and collected all relevant information and documents. Plus, it'll help if you can make important decisions rapidly and are willing to participate fully in the process. No, the fees are not going to be tax-deductible, even if you own a business. They used to be deductible as an itemized deduction prior to the Tax Cuts and Jobs Act and may again be deductible when those provisions sunset after 2025.

Your goal is to find someone that is competent, experienced, and a good fit. You probably don't want your friend or cousin unless they specialize in estate planning. You can check to make sure they're in good standing with the bar and that estate planning is what they spend the majority of their time doing. Like with a financial advisor or a doctor, there is some value to a few gray hairs. Someone who has already done this hundreds of times is usually going to be more efficient and make fewer mistakes. You also want someone that you can relate to and enjoy working with. Ideally, they have worked with a lot of people in your particular situation. WCI keeps a shortlist of recommended attorneys for your estate planning and asset protection needs.

You have your documents and the ideas of what you want, and you have hired an attorney. Now, it is time to establish your directives and time to start producing documents.

The will lists a guardian and conservator for minor children. It may also list who is to receive various assets, including real property like your home that is not covered by beneficiary designations. These may be very simple “I love you” wills if you are recently married with young children to incredibly complex legal instruments when there are blended families with married adult children and minor children involved.

In some states, a “holographic will” is actually valid and requires very little formalities. However, to make sure the will is valid and not contested, it is best to sign it in a formal way, including each of these steps.

<オル>A will typically names the executor of the will. Sometimes it is simply a trusted family member, especially if there is an attorney in the family. It can also be your estate planning attorney if you prefer to minimize family drama. This person will be responsible for wrapping up your affairs, including selling property and filing tax returns, as well as carrying out the instructions in your will. Named executors are simply acting in your stead, of course, and have no responsibility for or ownership of your debts or assets.

An important part of estate planning is also to go over every account or policy that can name beneficiaries and make sure the appropriate people or entities are named. You may wish to name a trust as the beneficiary. You can also usually name contingent beneficiaries if the beneficiary dies before you or refuses the gift. Beneficiaries are easily and routinely named for retirement accounts, annuities, and life insurance policies. But you also need to think about Health Savings Accounts, 529s, and ABLE accounts. Taxable investing accounts and bank accounts can also be set up to go to a beneficiary at the time of your death with a “Payable on Death” or “Transfer on Death” designation. In some states, you can even do this with houses and cars. This is faster, cheaper, and more private than simply naming beneficiaries for each of these in your will and having the executor take it through probate.

If you want some control over your healthcare decisions after you get too sick to make your own decisions, you probably want to get a living will and name a healthcare proxy. This can even be a formal healthcare power of attorney. You may want to provide a specific HIPAA waiver for your proxy. Perhaps you want to fill out your state's formal Do Not Resuscitate (DNR) form. Whether it's in the will or not, provide as much direction as you wish to your proxy including what you would want in a given situation. I find that most people are fine with an attempted resuscitation or a short period of life support; they just don't want to “be a vegetable” who is “living on a machine the rest of their life.” Consider including specific instructions about CPR, dialysis, intubation/ventilation, pressors, nutrition support (tube feeds), ECMO, and surgery.

A revocable or living trust is very useful if you wish to pass on assets faster, with less expense, with more privacy, and with more control to your heirs. Most white coat investors will want to put one in place as part of their estate planning process and this is likely a large part of the work and cost of the attorney.

A trust is a separate legal entity—like an individual, a corporation, or a limited liability company—and lives on after your death according to its provisions. To pass an asset on to heirs through a trust, the asset must be titled in the name of the trust. With a revocable or “living” trust, you can simply remove the asset from the trust at any time while you're alive. Thus, it passes assets outside of probate but provides no asset protection. With an irrevocable trust, you are giving away the asset. You lose a lot of control that way, but you gain two things:

<オル>An irrevocable trust does have to file a tax return, however, and it is subject to a more aggressive set of tax brackets. This is why a lot of people put whole life insurance policies inside irrevocable trusts since they do not generate taxable income.

A testamentary trust is created at the time of your death. While this avoids the hassle and expense of maintaining a trust during your life, the assets must go through probate before going into the trust.

Charitable trusts can also be created at this point in the estate planning process. These can save a lot of taxes, but generally do require significant charitable intent to work out well.

Remember to actually retitle assets in the name of the trust, or you will spend all that money on a trust for nothing.

This discusses your funeral, burial, and other final wishes. You may also wish to include messages for family or friends. Obviously, you don't need an attorney to do this part, but be sure to include it with your other papers and tell people it exists, or they might not look at it until it is too late. This may be a good place to include the master password for your password manager and directions for what to do with social media accounts, email accounts, Google Drive, and other assets in the cloud.

This is also a good time to give some thought as to what you will do with your businesses. These might be a practice, side gig, or full-on free-standing business with multiple employees. Just like people need estate planning, so does your business. What will happen if you die? What do you want to happen? Make sure the business has a plan in place. Forming a business as a Family Limited Partnership (FLP) or Family Limited Liability Company (FLLC) can save a lot of taxes and provide asset protection, and it can facilitate a smooth, private transition at the time of your death.

As your trusts and other documents and plans are being created, this is a good time to consider the estate tax, income tax, and asset protection implications of your plans.

Estate tax is tax that is paid on any amount over the estate tax exemption. It is often called the “death tax.” The idea behind it is to try to prevent a class society from forming as rich people pass wealth to their kids' generation after generation. The federal estate tax brackets rapidly rise to 40%, meaning 40% of what you leave behind goes to the government and 60% to your heirs. Any money left to charity is not subject to that tax. However, the tax does not begin until your estate is larger than the estate tax exemption. On a federal tax level, that exemption is $13.61 million ($27.22 million married) in 2023, but some states have their own estate tax with a significantly lower exemption amount. Under current law, the married exemption is “portable,” meaning that just because you were married, you get the $27 million exemption at the time of your death. Essentially, if you die, your spouse can inherit everything from you without using up any exemption AND they get to use your exemption when they die.

Unlike the estate tax, which is paid by the estate (essentially the deceased), some states (Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania) have an inheritance tax instead of an estate tax or in addition to an estate tax. This tax is assessed to the person inheriting assets. It is entirely possible for an asset to be subject to an estate tax in one state where the person died AND be subject to an inheritance tax in another state where the inheritor lived!

The gift tax is rarely paid and is best thought of as part of the estate tax. Basically, if you give anyone more than $18,000 [2024] in a year, the amount above $18,000 is subtracted from the estate tax exemption amount. Once that exemption amount is completely gone, gift taxes must be paid. Until it is gone, you are merely required to file a gift tax return, not pay any actual tax. The gift tax prevents people from giving everything away on their death bed so that it isn't subject to estate taxes.

The main way to avoid estate taxes is to minimize the size of the taxable estate above the exemption amount. There are many ways to do this including:

The last two methods use up less of the estate tax exemption than you might think, because the value of the gift is reduced. That's due to the fact that the inheritor will not receive them for some time or because the asset is illiquid.

It is also a good idea to think about how you are going to reduce income taxes for yourself and your heirs. If you plan to split your estate between heirs and charity (or even just heirs in very different tax brackets), carefully decide which assets go where, as per the chart earlier in this post. You also want to take full advantage of the step-up in basis at death. It is often better to borrow against low basis assets rather than sell them and realize even long-term capital gains in the last years of life.

When forming businesses or doing estate planning, there are numerous asset protection implications. It can make sense to combine asset protection and estate planning into one process. Retirement accounts, whole life insurance, irrevocable trusts, family limited partnerships, and family limited liability companies can all have strong asset protection benefits. When forming trusts, be sure to consider the implications of the trust on your children and other heirs. Written properly, you can ensure the assets of the trust only benefit your heir and not their spouse or ex-spouse.

Now that your estate plan is in place, you need to do a few things to maintain it.

Estate plans should be reviewed for an update in three circumstances:

Sometimes, simple addendums can be added to documents or you may need to completely redraft the documents and entities you previously formed.

Beneficiaries may also need to be changed, and additional assets may need to be placed into the name of the trust.

You should have multiple copies of your estate planning documents. You should keep an easily accessible copy of everything at home in one place. Clearly label it so it can be found and tell those who need to know about it where it is. An electronic copy is also a good idea, and you may even want an additional physical copy elsewhere. Your attorney will also likely keep a copy of it. You may also want to provide a copy to the executor of the will, the conservator of your children, the trustee of your trusts, and even major heirs.

As a general rule, your estate planning documents are not a great place to keep secrets. It is far easier for your heirs to plan their own financial lives when they know what is coming. You may also wish to keep a file of your living will, healthcare proxy, and/or healthcare power of attorney at your local hospital and physician's office. Remember if no one can find your documents, it is as though they do not exist. What a shame to put all of that time, effort, and money into the process for nothing. Dying intestate (i.e. without a will) means you have chosen your state's designated estate plan instead of your own.

The first thing that may be needed after you die is that letter of intent that outlines your funeral wishes. The rest of the process probably won't even start until after that occurs. Once the dust settles from that, the executor of your will goes to work, and the probate process begins.

Probate law is state-specific, but you usually need an estate of a certain size before it must go through a full probate. Remember, your entire net worth does not contribute to the size of your estate for probate purposes, only the size of the estate that goes through probate. In my state of Utah, an estate must go through probate if:

So if you have your home, cars, boats, bank accounts, and taxable investing accounts owned by a revocable trust and have beneficiaries named for all retirement accounts and life insurance policies, you could potentially avoid this process altogether.

First, the last will and testament is authenticated and the executor/administrator/personal representative is appointed. Then this person must do the following tasks:

While state-specific, this bond is often required and is likely to cost at least a few hundred dollars and possibly thousands. If someone comes to the court and says the executor is not fulfilling their duties, the court can investigate and, if applicable, force them to do so because of this bond.

Hopefully, you've made this easy on your executor.

Appraisals may be required for some assets, but most of the time, this is just getting bank and brokerage statements. If you're still living at home at the time of your death, the executor may hire an estate sale company to determine a value for all the stuff left in your house.

A great benefit of living a debt-free life, at least by the end, is your executor has one less task to do. Remember your debts have to be paid off before anyone gets an inheritance, at least an inheritance of the assets that go through probate. Bypassing assets outside of probate, you can potentially stiff a creditor while still providing an inheritance.

An income tax return must still be filed in the year of your death (if you left a spouse, they can still file Married Filing Jointly one more time). The executor will also be responsible to make sure an income tax return for the estate is filed. An estate is technically a different entity than the person who died and needs its own tax number and its own special return (IRS Form 1041). It must file its own return if any beneficiary is a non-resident or if the estate made $600 or more. An estate tax return (IRS Form 706) must be filed if the estate is over the exemption amount OR if any of the exemption is being transferred to the spouse. The executor may also need to ensure state income and estate tax returns are filed.

Finally, the executor is responsible for actually distributing the estate. It would be a very bad idea to make any distributions before all creditors and taxes have been paid, and thus, you can see why it takes a long time for heirs to get their inheritance when it has to go through probate.

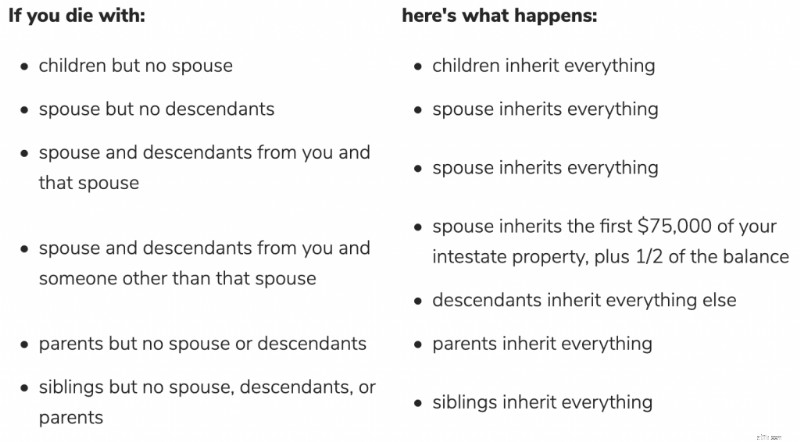

If you do not have a will appointing an executor, the state will appoint one. The usual first choice is your spouse or domestic partner, then your children, then any other available family. The executor must follow the state's intestate succession laws. These laws generally pass assets preferentially to a surviving spouse and children, not unmarried partners, friends, or charities. These laws can be complex if your family situation is complex, but it's very simple in a simple situation. For example, if you were only married once and only had children with that person, all of your assets go to your spouse if the spouse is alive and to the kids if the spouse is not alive. Otherwise, it gets very interesting. Per Nolo, this is what happens in my home state of Utah:

Intestate laws in other states are generally similar, but they all vary somewhat, especially as treating domestic partners. If you do not like your state laws, that is a very good reason to get a will in place ASAP.

The trustee of your trust(s) has a fiduciary responsibility to carry out the instructions in the trust, whatever they may be. There are almost limitless options for passing assets to your heirs via a trust. There can be restrictions based on age, knowledge, religion, marital situation, educational achievements, or almost anything else you can think of. Some trust fund kids have it easier than others!

I hope this is helpful in outlining the general strategies of estate planning. There are lots of other tricks and tips involving trusts that I'll discuss in future posts. Remember that having a will, naming beneficiaries properly, and titling assets properly is cheap and probably all that most of us will ever need. If you need more than that, a few thousand dollars spent on an estate planning attorney will be well worth your time and effort. Also remember that the laws governing this process are state-specific and frequently change, so personalized, up-to-date advice is warranted in this important area. Anytime you get wind that Congress or your state legislature has changed the laws regarding probate or regarding estate taxes, you ought to consider whether to visit with your estate planning attorney again.

Have more questions about estate planning or protecting your assets? Hire a WCI-vetted professional to help you sort it out.

What have you done as far as estate planning? Do you have a will? A trust? Have you at least checked to make sure your designated beneficiaries were right?

[This updated post was originally published in 2011.]