借金—個人のお金とそれに関する終わりのない議論において、これ以上に重みのある言葉はないかもしれません。それは時々(一般に不適切ですが)奴隷制と同一視されます。また、(これも不適切ですが)「経済的自由」や「他人のお金」と同一視されることもあります。借金は私たちの金融システムの重要な部分であり、便利なツールですが、財政を破滅させ、貧困を維持する可能性もあります。この記事では、借金に関するあらゆることについて説明します。皆さんが、新しく、よりオープンな考え方、いくつかの新しい戦略、善悪に対する借金の力に対する新たな敬意を持って立ち去ることを願っています。

借金の利点

借金の危険性

一般的な借金に関するガイドライン

良い借金と悪い借金

借金の代替可能性

学費の代替支払い方法

負の絆としての借金

証拠金投資

借金を返済するか投資する

借金のない生活の利点

借金の価値

道具または悪魔としての借金

借金は、世界の偉大な宗教書だけでなく、ほとんどの金融メディアやブログ界でも悪評が立つ可能性があります。真実は、あなたの周りの世界の驚異の主な原因は借金であるということです。私たちの経済とライフスタイルは、世界がこれまでに知った中で最高のものですが、その大部分は借金によって支えられています。 「消費文化」はさまざまな意味でアメリカの強みです。

ほとんどの場合、お金は借金です。政府が通貨を発行する場合、それは政府の課税能力に裏付けられた紙幣にすぎません。しかし、お金のほとんどは政府によって作られたものではありません。銀行によって作成されます。私たちはこれを「フラクショナル・リザーブ・バンキング」と呼んでいます。銀行にお金を預けると、そのお金の 0.6% が支払われる可能性があります。そしてそれを6%で他人に貸し出すのです。それは当然ですよね?その差額が銀行に収入をもたらし、銀行はすべての経費を支払い、利益を生み出すことができます。でも、お知らせがあります。単に6%でお金を貸し出すわけではありません。 6%で資金の10倍を貸し出します。本質的に、銀行はお金を生み出しました。しかし、ある人のお金は、他の人の借金にすぎません。そうであるに違いありません。それはどんな借金でも同じです。国債への投資は政府の借金です。 Amazon 債券は Amazon 株主の負債です。あなたの住宅ローンは他人の投資です。それは彼らのお金です。

西ヨーロッパとその子孫と呼ばれる歴史的僻地が過去 5 世紀以上にわたって世界を支配してきたのには多くの歴史的理由があります。ジャレド・ダイアモンド氏は、主な理由は銃、細菌、鉄鋼にあると主張する。ウィリアム・バーンスタインは、『プレンティの誕生』は財産権、科学的合理主義、資本市場、そして効果的な交通手段と通信手段によるものであると主張しています。どのような要因が最も重要であるかは誰にも分かりませんが、銀行 (借金) システムがイタリア北部で発展し、その後オランダ、そして最終的にはロンドンとニューヨークで改良されたことがそれに大きく関係していることは疑いの余地がありません。

債務と破産からの保護により、世界最大かつ最も収益性の高い企業の発展が可能になりました。彼らはしばしば「小さな男」を迫害していると嘲笑されますが、真実は、企業が私たち全員を劇的に裕福にし、私たちのライフスタイルを劇的に改善したということです。何だと思う?ほとんどの企業は、現在の規模に成長し、現在の事業運営を維持するために借金を利用しました。時間の経過とともに変化しますが、S&P 500 企業のうち無借金企業は 5% 未満です。

より個人的なレベルでは(地球上の何十億人もの人々を掛けると、かなりの額になります)、借金のおかげで私たちの多くは重要な面で生活を改善することができました。おそらく教育の甲斐あって、収入を劇的に増やすことができたのでしょう。もしかしたら、そのおかげで私たちは人生を生きるための素晴らしい場所を買うことができたのかもしれません。あるいは、そのおかげで私たち自身の小さなビジネスや事業を立ち上げることができたのかもしれません。

購入する前に家の費用を全額貯めなければならないことを想像してみてください。裕福な家庭の出身でない限り学校に通えないことを想像してみてください。自分の屋根板を干すのに必要な資金を得ることができないために、低賃金の従業員として立ち往生していることを想像してみてください。信頼できる中古車を買うために数千ドルを借りることができなかったために、素晴らしい仕事を断らなければならないことを想像してみてください。借金は、私たちが社会として、また個人として享受できる経済的成功の理由の 1 つです。

何世紀も前(驚くほど少数ですが)、債務不履行の結果は劇的に深刻でした。債務者刑務所は、1840 年代までは米国でも実際に存在しました。借金を支払わなかった場合、あなたまたはあなたの代わりの誰かが借金を支払うまで、文字通り刑務所に送られることになります。企業および個人の破産保護は、世界の歴史の中で比較的新しいものです。したがって、世界の偉大な宗教書が借金について深く警告しているのを見るのは驚くべきことではありません。

ユダヤ人もキリスト教徒もこの本から知恵を得ています。貸し借りについては何と書かれていますか?かなりの量です。

金持ちが貧乏人を支配し、借り手は貸し手の奴隷となる。 (箴言 22:7)

誓約をしたり、借金の担保を設定したりするような人になってはなりません。支払うものが何もないのに、なぜベッドを下から取り上げる必要があるのでしょうか。 (箴言 22:26-27)

悪人は借りても返さないが、義人は寛大に与えます。 (詩篇 37:21)

7 年ごとの終了時に、あなたは釈放を許可するものとします。そして、これが免除の方法です。すべての債権者は、隣人に貸したものを免除する必要があります。主の釈放が宣言されたのですから、彼は隣人、兄弟にそれを強要してはならない。 (申命記 15:1-2)

あなたは多くの国に貸してもよいが、借りてはならない。 (申命記 15:6、28:12)

もしあなたが貧しい私の同胞にお金を貸すなら、あなたはその人にとって金貸しのようなものであってはならず、彼から利息を徴収してはならない。もしあなたが隣人のマントを誓約に受け取ったなら、日が沈む前にそれを彼に返さなければなりません。 (出エジプト記 22:25-27)

見知らぬ人のために安全を築く者は必ず害を受けるが、誓約書で手を打つことを嫌う者は安全である。 (箴言 11:15)

分別のない人は、隣人の前で誓約をし、安全を確保します。 (箴言 17;18)

外国人に利息を請求することはできますが、兄弟に利息を請求することはできません。 (申命記 23:20)

キリスト教徒は、新約聖書が借金反対でもあることに気づきました。焦点は、融資よりも借入にありますが、融資から利益を得ることにも重点を置いています。

互いに愛し合うこと以外には、誰にも何の義務もありません。なぜなら、人を愛する者は律法を全うしているからです。 (ローマ人への手紙 13:8)

塔を建てたいと思って、まず座って、それを完成させるのに十分なお金があるかどうかを計算しない人がいるでしょうか? (ルカ 14:28)

あなたに物乞いをする人には与えなさい、あなたから借りる人には断ってはならない。 (マタイ 5:42)

そして、あなたが受け取ることを期待している人にお金を貸したら、それはあなたにとって何の功績になるでしょうか?罪人でも、同じ金額を返すために罪人に貸します。しかし、敵を愛し、善を行い、何の見返りも期待せずに貸しなさい。そうすれば、あなたの報酬は大きくなるでしょう。 (ルカ 6:34)

今日、私たちに日々の糧を与えてください、そして私たちが債務者を赦したように、私たちの負債も赦してください。 (マタイ 6:12)

聖典と末日聖徒イエス・キリスト教会の指導者たちは、借用に対して厳しく警告しています。

隣人から借りた者は、借りたものを返さなければなりません。 (モーサヤ 4:28)

借金を返済し、束縛から解放されましょう。 (教義と聖約 19:35)

あなたの敵に借金をすることは禁じられています。 (教義と聖約 64:27)

借金をすべて返済してください。 (教義と聖約 104:78)

主の家を建てるために借金をしてはいけません。 (教義と聖約 115:13)

現代の教会の指導者たちはそれほど極端ではありませんが、それでも間違いなく反債務者です。 J. ルーベン クラークは、大恐慌のはるか昔にこう言いました (少し言い換えました)。

「分割払いで買うということは、将来の収入を抵当に入れることを意味する」とJ・ルーベン・クラーク・ジュニア大統領は1938年に述べた。「病気や死亡、あるいは失業によって収入が途絶えれば、購入した不動産はそれまでにつぎ込んだものと一緒に失われる。私があえて一つ提案したいのは…普通の家庭は実際の生活必需品だけを分割払いで購入し、贅沢品は購入時に支払えるのでそのままにしておくのがよいだろう。私は必需品と必需品との間に線を引こうとは思わない」 [ホンダ シビックに] 乗って通勤できる [医師] が、その目的のために分割払いで [驚異的なスピードを誇るテスラ モデル S] を購入することは正当化されるとは言えません。」

そしてより有名なのは、私が以前に使用した引用です:

「利息は眠らず、病気にもならず、死ぬこともありません。病院に行くこともありません。日曜も休日も働きます。休暇を取ることもありません。訪問も旅行にも行きません。利息には愛も同情もありません。花崗岩の崖のように硬くて魂がありません。ひとたび借金をすると、利息は昼も夜も常にあなたの味方です。利息を避けたり、逃げたりすることはできません。利息を無視することはできません。懇願、要求、命令に屈することはありません。道を進むか、コースを横切るか、要求を満たさないと、それはあなたを押しつぶします。」

最近、ゴードン B. ヒンクレーは次のように述べています。

「私は、自国民を含む国民にかかる巨額の消費者分割払い債務に悩まされています…もちろん、家を買うために借金が必要かもしれないことは承知しています。しかし、余裕のある家を購入して、30年間も容赦なく猶予なく常に頭の上にのしかかる支払いを軽減しましょう。……自分の財政状態に注意してください。支出を控えめにすることをお勧めします。借金を避けるために購入時に自分を律してください。」できるだけ早く借金を返済し、束縛から解放されてください。

家計に深刻な借金がかかっていると、自立することはできません。他人に義務を負っているとき、人は独立も束縛からの自由もありません。

状況によっては借金も必要です。おそらく、教育を完了するために借金をする必要がある大学生もいるでしょう。もしそうなら、それを返済してください。そして、たとえそうでなければ享受できるかもしれないいくつかの快適さを犠牲にしても、すぐにそうしてください。ほとんどの人は住宅を確保するために借金をしなければなりません。もちろん、事業の経営においては、慎重な借入が必要かつ適切な場合もあります。ただし、賢明に行動し、支払い能力を超えないようにしてください。

手頃な価格の住宅の購入や、おそらくその他の必要なもののための合理的な借金は許容されます。しかし、私が座っている場所からは、本当に必要のないもののために愚かにも借金をした多くの人たちの恐ろしい悲劇が非常に鮮明に見えます。」

トーマス・S・モンソンはこう言いました。

「私たちはすべての末日聖徒に対し、慎重に計画を立て、保守的に生活し、過剰または不必要な借金を避けるよう強く勧めます。」

ジェームズ E. ファウスト:

「借金のない家を所有することは、賢明な生活の重要な目標です…抵当権や先取特権が免除されている家は差し押さえられません…独立とは…個人の借金や、世界中の借金に必要な利息や手数料から自由になることを意味します。」

率直な物言いで知られるスペンサー・W・キンボールは次のように述べています。

「借金から抜け出し、借金をしないようにしましょう。」

ヒーバー J. グラントは次のように説明しました。

「人間の心と家族に平和と満足をもたらすものがあるとすれば、それは収入の範囲内で生活することです。そして、つらく、落胆し、落胆させるものがあるとすれば、それは、果たせない借金や義務を負うことです。」

コーランの中で最も長い聖句は借金に関するもので、その一部は次のように書かれています。

定められた期間で借金を契約するときは、それを書面に書き留めてください…債務者の命令に従い、彼に主である神を畏れさせ、[借金を]まったく減らさないようにしてください。二人の男性を証人として呼んでください…借金の額が小さくても大きくても、返済期日とともに書き留めておくことを軽蔑しないでください。この方法は神の目から見てより公平であり、証言としてより信頼でき、あなたとの間に疑念が生じるのを防ぐ可能性が高くなります。 (2:282)

別の人はこう言います:

アッラーは高利貸しからすべての祝福を奪いますが、慈善行為に対しては増額を与えられます。 (2:276)

さらに重要なことは、預言者ムハンマドが次のように述べたことです。

「もし人がアッラーのために戦いで殺され、その後生き返り、借金を負った場合、その借金が返済されるまでは楽園に入ることはできません。」

「男が故意に受け取るリバ(利息)のディルハムは、ジーナ(淫行)を36回犯すよりも重い罪である。」

敬虔なイスラム教徒は、貸す側も借りる側もこのことを非常に真剣に受け止めています。私は毎月、イスラム教徒から、レバレッジを利かさない不動産投資や利息のない投資信託について問い合わせるメールを受け取ります。彼らは確かに債券やCDには興味がありません。 「イスラム法に準拠している」と考えられる投資信託がいくつかあり、私は通常、それらのファンドに誘導します。

おそらく、無宗教の人にとっては、私たちの社会における借金の影響が理解しやすいでしょう。次の 2021 年の統計を考慮してください。

私たちのほとんどは、経済的負債によって人生を台無しにされた人を知っています。借金がもたらした多くの良いことにもかかわらず、借金によって多くの破壊された生活が残されたことは確かです。そして、これは私たちの社会で現在利用できるすべての消費者保護と破産保護に当てはまります。

業界関係者に話を聞くと、驚くべき写真が現れる。銀行は文字通り、常に顧客に対して実験を行って、顧客に借金を返済させずにさらにお金を借りさせる方法を見つけ出します。金融業界には、あなたに借金をさせて富の構築を妨げることを仕事としている人々がいることを認識しなければなりません。

ベンジャミン フランクリンは次のように有名に言いました。

「借金が増えるよりは、夕食を食べずに寝るほうがいいです。」

したがって、借金を避けるために過度に宗教的になる必要はありません。

明らかに、あなたが経済生活を通じて借金を抱えながら何らかの穏健な道を描くつもりなら、上記の賢明な人々が数千年にわたって私たちに警告してきた問題を回避するために十分な注意を払わなければなりません。社会の大部分は、数学的にどのような可能性があるとしても、何のためにもお金を借りない方が良いでしょう。

さまざまな目的でいくら借りるのが妥当であるかについての実用的なガイドラインがあれば役立つと考える人もいるかもしれません。これが私の考えです。ただし、私に同意しない人もいることは承知しています。

クレジットカードは、名前とは裏腹に、信用を目的としたものではありません。彼らは恐ろしい信用源です。金利は高く(変動する場合もあります)、支払いを怠った場合の影響は深刻で、支払い計画は実際には借金を完済するように設計されていません。それらは「コンビニエンスカード」と呼ばれるべきです。その方がはるかに正確な名前です。銀行やATMに行って現金を受け取り、また店に戻るのは不便です。緑色の紙幣の束を持って歩き回るのは不便です。航空券を窓口で購入するのは不便です。

クレジット カードを入力します。さまざまな面で使いやすく、安全に使用できます。月末に支払いが行われる限り、この利便性を利用しても費用はかかりません。実際、一部のクレジット カードの特典プログラムにより、現金の代わりにカードの使用に対して報酬が得られる場合もあります。

しかし、冗談はやめましょう。銀行もバカじゃないよ。彼らは順調にやっています。アメリカ人の 45% は実際にカードに残高を入れています。さらに、クレジットカードを利用できる企業は手数料を支払っています。これらの手数料は通常、銀行が支払う報酬よりも高くなります。なぜ企業 (The White Coat Investor を含む) がクレジット カードを受け入れるのですか?それは、消費者であるあなたがカードを使用できるようにすると、さらに多くの商品を購入する可能性がはるかに高くなることがわかっているからです。しかし、クレジット カードの利用にかかるコストは誰が負担するのでしょうか?そう、消費者であるあなたです。通常クレジット カードで購入するため、何を買うにしても 2% ~ 3% 高くなります。

それは行動ファイナンスの側面さえ考慮していません。研究に次ぐ研究によれば、カードを使用するとより多くの支出が行われることがわかります。利便性と実際の信用に加えて、緑色のものの山を手放すよりも心理的苦痛が軽減されます。貯蓄率を 20% まで上げるのが難しい場合、問題を解決する最善の方法の 1 つは、クレジット カードを減らすことです。

いずれにせよ、買い物にカードを使用するかどうかにかかわらず、クレジットがクレジットのためではなく、単に利便性のためであることは間違いありません。したがって、クレジット カードのリボルビング債務の許容比率は 0. ゼロです。ジルチ。灘。クレジット カードに残高がある場合は、この金融ゲームで失敗していることになり、おそらくクレジット カードをまったく使用すべきではありません。ずっと。

車に対する私の態度や考えに対して、たくさんの反発を受けます。過去 6 か月間に売れなかった自動車の近くに行った私は頭がおかしいと思われています。私は家族や地球のことを気にしていないと言われました。しかし、車のローンの最高額についてアドバイスが欲しいのであれば、私の答えは 10,000 ドル未満であり、むしろ 5,000 ドルに近い金額を見たほうがよいでしょう。はい、たとえそれが2%のローンであってもです。はい、たとえ0%のローンであってもです。借金愛好家たちは、車のために借りることが経済的成功の秘訣であると私に説得しようとしましたが、うまくいきませんでした。これは私の最もお気に入りの 1 つです。ある医師は、クレジットで車を購入し、それを元に複数回借りることの賢明さを私に説得しようとしました。医師は私に「珍しい」車を買うよう説得しようとさえしました。

富を築いて慈善活動を支援する計画が珍しい車を購入することである場合、優先順位が少し混乱するかもしれません。不動産投資に 250,000 ドルが必要な場合は、まず車を購入してからそれを担保に借金をしないでください。それを不動産に投資するだけです。不動産への投資や慈善活動への寄付がもっとあることは保証しますが、トラック以外にネットワークを築く場所を見つける必要があります。

10,000 ドル以上の現金を持っていて車が必要な場合は、車の代金を現金で支払い、購入は手持ちの現金に限定してください。 10,000 ドルがなく、確実な移動手段が必要な場合は、それができるまで 10,000 ドル未満の車を運転してください。

多くの人が私の車に関するアドバイスを嫌い、それに従わなかったにもかかわらず成功していると指摘します。まあ、当然です。あなたは年間30万ドル稼いでいます。このような収入があれば、経済的な間違いはかなりカバーできます。それは間違いではありません。しかし、医師の収入ではカバーできない間違いの 1 つは、将来の収入に比べて巨額の学生ローンを組むことです。非常に高額な学校の教育費を全額借りて、給料の低い専門分野を選び、その専門分野内で薄給の民間の仕事に就き、それでもすべてうまくいくと信じている人が多すぎます。何だと思う?数学では合格できません。

あなたの心がどれだけ素晴らしいかは関係ありません。経済的/キャリア上の決定を誤ると、経済的に安全になることはなく、ましてや成功することはできません。家族に学費を支払わなければ、かかりつけ医や小児内分泌専門医になれないと言っているのではありません。それがあなたのキャリア目標であるなら、そのキャリア目標に沿った学生ローンプランが必要だと言っているのです。その計画とは、非常に倹約した生活を送り、生活費の安い地域で特に高収入の仕事に就くことと、訓練後の5年間は住民のように暮らすことを組み合わせて、ローンを返済できるようにすることかもしれない。その計画では、PSLF の資格を得るために、トレーニング後に学業に時間を費やすことになる可能性があります。その計画では、20年間のPAE支払いを行いながら、同時に税金爆弾資金を貯蓄することさえあるかもしれない。しかし、砂の中に頭を突っ込んで最善の結果を期待することはできません。

ここでは私が教育に関してよく挙げる比率をいくつか挙げます。比率の最初の部分は、トレーニング終了時の学生ローンの規模です。比率の 2 番目の部分は、トレーニングを終了してから数年以内の総収入です。

1:1 以下であれば、良い投資ができたことになります。私たちは 25 万ドルの学生ローンと、年収 25 万ドルの仕事について話しています。居住者のように生活することで、この借金をわずか 2 ~ 3 年以内に返済し、その後は残りの人生でその莫大な収入を楽しむことができます。

2:1 であれば、この取引はまだ許容可能ですが、実際には良い取引ではないと私は主張します。これが私が推奨する借金の最大レベルです。もしあなたが獣医師になりたいと思っていて、卒業したら75,000ドルの収入が見込めるのであれば、学校に通うために300,000ドルも借りない方が賢明です。比率を2に制限すれば、居住者と同じように生活していても借金を返済できます。もっと長くやればいいだけです。年収30万ドルの医師が60万ドルの借金を抱えていると考えてみましょう。税金(75,000ドル)と居住者より少し良い生活(75,000ドル)を差し引くと、年間150,000ドルが借金に充てられることになります。 5 年以内に処分する必要があります。

3-4+:1 では、もはや適切な投資はできません。 501(c)(3) に基づいて 10 年間フルタイムで働くことで PSLF を通じて非課税になるか、20 年間の PAYE 支払い (または 25 年間の返済) による IDR 免除によって課税対象 (税金爆弾に備えて貯蓄) によって借金が免除されることで、あなたは救われるかもしれません。しかし、法的なリスクがこれほど大きいキャリアパスを勧めるのは私にとって非常に難しいです。比率を修正する必要があります。あまり借りないようにするか、(おそらくその可能性が高いですが)単により良い仕事に就くかのどちらかです。このような比率を持つ医師のほとんどは、専門分野の四分位の収入が最も低いです。収入が高くなると、比率は 2:1、あるいはそれ以上になる可能性があります。彼らは通常、借金の問題よりも大きな収入の問題を抱えています。

ガイドラインが必要な方のために、住宅ローンに関する 2 つの一般的なルールをご紹介します。

<オル>とても簡単ですよね?そして、それは最大値であり、目標ではないことを忘れないでください。つまり、80万ドルの家が欲しいのに収入が30万ドルしかない場合、20万ドルを頭金として預ける必要があります。医師のローンを利用していて、頭金が 10,000 ドルしかない場合は、もっと安い家を探すべきです。

生活費が非常に高い地域に住んでいる人は、おそらくそのアドバイスを憂鬱に感じるでしょう。あなたがベイエリアで 18 万ドル稼いでいる医師なら、職場から車で 3 時間以内に家を買うことは絶対にない、と私は基本的に言いました。この種の分野では、その比率を 2 倍から 3 倍、4 倍まで拡張することは許容されると思いますが、10 倍まで拡張することは許容されません。たとえギャンブルが時々誰かにとってうまくいくとしても、家が貧乏になることは望ましくありません。そのストレッチをする場合は、富を築く能力に深刻な経済的影響を与えることを認識し、私立学校に行かない、休暇の頻度が減る、車の質が悪くなる、退職後の生活が遅くなる、またはあまり贅沢にならないなど、経済生活の別の場所で補う必要があることを認識してください。

湖畔の家やスキーコンドミニアムなどのセカンドハウスについては、現金で払ってほしいと思いますが、費用の一部を借りてもいいと思います。重要なことは、この家を母屋と同様に、投資ではなく消費アイテムとして見ることです。セカンドハウスの費用をすべて支払う余裕があり、目標を達成するために十分な貯蓄がまだできる場合は、購入しても問題ありません。ただし、最初に家を建てたときよりも多額の頭金が適切だと思われます。市場が好転した場合(休暇用不動産の経営が厳しくなる可能性もある)、水没したくないでしょう。あなたは、家を売って住宅ローンを返済して、家を出ることができるようにしたいと考えています。

改修には非常に費用がかかる場合もあり、通常は少なくとも一部は借金で賄われます。ここでの私のガイドラインは、リノベーションによって家の価値が上がった額以上は借りないことです。これはおそらく支出額の 50% 以下です。キッチンとバスはもう少し戻ります。造園、ガレージ、「ユニークな」改修工事の収益は大幅に減少します。一部の改修工事(プールなど)は、将来の購入者の観点からは負担となる場合もあります。

住宅はおそらく人生で最も高価な買い物です。特に借金を使ってやっている場合は、あまりお金をかけないでください。

ボート、スノーモービル、四輪車、家具、敷物、絵画、その他のものであっても、他のものを買うために借金をするべきではないと思います。それらの商品を購入するのは、一度だけ支払うことができ、元が取れたとわかるととても楽しくなります。これらの品物はおそらく価値が下がるでしょうが、もし私が問題に陥ったとしても、今ではそれらは呪い (キャッシュ フローからの継続的な支払いが必要なため) ではなく、私の人生にとって実際に祝福となっています (何かのお金で売れるため)。

個人金融では、良い借金と悪い借金があるという考えが一般的です。基本的な考え方は、収入を増やす借金(学生ローン、ビジネスローン、練習ローン)、または価値の高い資産(家、練習、珍しい車(?))を購入できる借金は何らかの形で良い借金であり、サービスや消耗品、または減価償却資産の購入に使用される借金(クレジットカード、自動車ローン、家具ローン)はすべて不良借金であるということです。これは借金についてのかなり表面的な理解です。たとえば、不良債権はどれですか:

どちらを借りたいかは言えますが、学生ローンはどういうわけか常に「良い借金」のカテゴリーに入れられます。一部の債務が他の債務よりも質が高いというわけではありませんが、これについては少し後ほど説明します。

真実は、借金もお金と同じように代替可能であるということです。借金がもともと車、学校、家、またはアイスクリームコーンの支払いのために行われたかどうかは、実際には重要ではありません。一度手に入れたらそれは借金です。そして、借金がある場合、その借金を返済する代わりに購入するあらゆるものは、すでに抱えている最高利息の借金と同じ条件でそのサービスや製品を購入するのとまったく同じことになります。

おっと!びっくりしました!

そうです。借金を抱えている場合、購入するものはすべてクレジットで購入されます。食料品、携帯電話の料金、休暇、車…すべて。この考え方を持てば、借金から少し早く抜け出すことができるかもしれません。

「これを買うために 3.5% で借りますか? おそらくそうではないので、買いません。」

私たちの社会のほとんどの人は借金を抱えているので、私たちの社会のほとんどはあらゆるものを借金しています。それは必ずしも悪いことではないと思いますが、世界を見るには興味深い方法です。

上で述べたように、基本的に借金は絶対にあってはならないと考えるほど借金嫌いの人もいます。しかし、実際に押してみると、 それらが存在していることがわかります。 借金を負うこと。彼らはそれを別の名前で呼んでいるだけです。私のお気に入りの回避策の 1 つは、イスラム住宅ローンの概念です。敬虔なイスラム教徒は、借りられなかったらどうやって家を買うのでしょうか?彼らは「イスラム住宅ローン」を得る。 3 つのタイプがあります:

イジャラ: 銀行が不動産を購入し、毎月の固定価格で一定期間リースします。その後、銀行はあなたに不動産を与え、あなたが貸し手に返済した後、その家をあなたの名義にします。

ムシャラカ: あなたと銀行はそれぞれ、不動産の別々の部分を所有しています。支払いを行うと、その一部は資本金、一部は家賃となり、銀行は不動産の取り分を少し多めに与えてくれます。家賃は、支払いの利息部分と同様に、期間が経過するにつれて徐々に下がっていきます。

ムラバハ: 銀行がその不動産を買い取ります。その後、それをより高い価格で販売し、一定期間の分割払いで支払うことになります。基本的には、利息/利益が購入価格に組み込まれるだけです。

敬虔なイスラム教徒と同じくらい借金に反対している人がいるとすれば、それはラジオのトーク番組の司会者であるデイブ・ラムジーだ。彼が大丈夫だと思う唯一の借金(推奨はされていませんが)は、頭金 20% の 15 年固定住宅ローンで、月々の支払額は手取り額の 25% 未満です。デイブは、教育費さえ借りるべきではないと考えています。実際、借金せずに学部教育を終えるのはかなり合理的だと思います。慎重に学校を選び、奨学金を申請し、在学中にアルバイトをして夏の間一生懸命働き、そしておそらく親の少しの援助さえあれば、学生ローンなしで学部教育を受けることは可能だと私は思います。

しかし、医学部や歯学部のような高額な専門学校となると、通常は年間5万ドルから10万ドルの学費がかかるため、状況は一変します。学生がアルバイトでそれを稼ぐことを期待することはできません。さらに、夏休みは(ほぼ)なく、奨学金もはるかに少なくなります。

医学部に行くために貯金するのはあまり賢明とは言えません。生活資金を貯めるために 15 年間働いて、その後 15 年間の医師の収入を逃す可能性があります。言うまでもなく、人生のかなりの部分がやりたいことをしていないことになります。お金を借りる方がはるかに賢明です。適切な金額のみを借りていることと、その後は適切な期間で返済する計画があることを確認する必要があります。確かに、何度も一致しないと本当にイライラする生徒も少数はいるでしょうが、ほとんどの場合、借りたお金を使ったとしても、これは非常に賢明な投資です。

Dave's proposed solution for paying for medical school is to do what I did—sign a contract instead of borrowing money. However, like an Islamic Mortgage, this is just debt by another name. The three main contracts that people sign are:

With each of these programs, your tuition, books, and fees are covered, and you are provided a living stipend.素晴らしい! A “scholarship” right?あまり。 All you have done is signed an indentured servitude agreement. Centuries ago, people came to America as indentured servants. Their employer paid the costs for them to emigrate, and then they were obligated to work for that employer—usually very hard and for not much money—for seven years. That sounds an awful lot like these programs.

With the HPSP program—in exchange for paying for you to get an MD, DO, DDS, or DMD—you have to go through the military match, live where they tell you to live, and be deployed wherever they tell you to go for four years. The pay is significantly less than the average for most specialties. In essence, they just gave you part of your salary upfront. Now the deal is better for some people than others (more expensive school, lower-paying specialty) but it's rare for someone to come out dramatically ahead financially for taking this deal. You certainly do not finish school “debt-free”, except by the narrowest definition of debt. Most doctors, if they live and work similarly to how they must live and work in the military, could retire substantial medical school loans in less time than it took to pay off their military commitment.

The deal with NHSC is similar. While there is no NHSC match or deployments, they certainly limit the specialties you can practice and the physical location and type of practice for four years afterward. The pay is also relatively poor (about $160,000 these days).

With an MD/Ph.D, you take the first two years of medical school, and then you hit pause to earn a Ph.D. That Ph.D may take anywhere from 3-7 years before you start your third year of medical school. Yes, school is paid for and you earn a stipend, but your opportunity cost is a half-decade of attending physician income. In essence, you're getting part of your pay upfront in the form of waived tuition.

The bottom line with each of these programs is that if you're going to do any of these things (military service, work in a rural or underserved community, or get a PhD) anyway, you should enroll in these contract programs. But you should not do any of them just to avoid medical school loans.

When building a portfolio, debt functions as a negative bond. Just like a bond provides a low-risk fixed return, so does paying off debt. While bonds do lower overall portfolio volatility and perhaps assist investors in staying the course in a market downturn, there is no mathematical reason to hold a bond paying 2% while you have a 4% mortgage or a 7% student loan you could pay off instead.

On a similar note, many people advocate for a 100% stock portfolio—no bonds. They argue that it provides the highest return. My question for them is, “Why stop at 100%? If 100% is good, why isn't 120% or even 150% better?” How do you get to stock percentages greater than 100%? Well, since debt is a negative bond, you get there by borrowing money and investing it. Many brokerages will let you borrow against your portfolio, sometimes at surprisingly low but typically variable rates. You can borrow up to 50% of the value of your portfolio. Most would recommend against a ratio that high, since when you are that highly leveraged, any drop in the value of the stocks will trigger a margin call. But if you borrowed 20% of the value of your portfolio, you could get to 120% stock portfolio pretty easily.

Frankly, since money is fungible, if you have any debt at all, it's like you're investing on margin already. While investing in stocks on a 2% margin might seem somewhat wise, investing at an 8% margin using some crummy student loan or a 15% margin using a credit card does not.

It's pretty easy to understand how borrowing at 2% and investing at 10% works out well in your favor. Imagine you borrow $10,000 at 2%. Each year you owe $200 (2%) in interest. But you may earn $1,000 in interest (10%). Before taxes, you've made $800. After taxes (let's assume a 35% marginal tax rate), you've made $520. It seems pretty good to get a “free” $520. However, remember that you don't get 10% from a risk-free investment. If that investment had lost 10% of its value instead of earning 10%, instead of gaining $520 after-tax, you would have lost $1,200 ($780 after-tax).

None of that really seems worth all the hassle of dealing with a loan, but what if we made the loan a lot bigger? What if we borrowed $1 million instead of just $10,000? Now we're looking at a possible $59,000 gain with a 10% gain and a $78,000 loss with a 10% loss on the investment. More money doesn't make someone a different person. It just makes them more of what they already are. In the same way, more leverage doesn't change an investment, it just makes it more of what it already is. If it was going to perform well before, it is now going to perform really well and vice versa. However, when you don't really know in advance how something will do—and with the added concern of margin calls—it seems an ounce of caution is in order.

While we're on the subject of investing on margin, it's worthwhile to point out that most real estate equity investments are purchased on margin. Leverage, i.e. the use of debt to buy the investment, is routinely used, primarily to facilitate the raising of capital but also to boost returns. In our example above, we just looked at $10,000 and $1 million in borrowed money. But with most real estate investments, the purchase is only partially completed with borrowed money. Many investors wonder how much they should borrow. They want to be protected and to get out of the investment without bringing money to the table if it all goes bad, but perhaps more importantly, they want the investment to be cash flow positive so they can hold on to it long-term even if its value drops temporarily.

No matter how much money you make at your day job, you can only carry so many negative cash flow properties for so long before you go bankrupt. But you can carry an infinite number of cash flow positive properties.

You can figure out your required “cash flow positive down payment” by running the numbers on your investment, but most of the time, you're going to come up with a number that suggests you put down 25-35% of the investment on any halfway decent deal. With that size of a down payment, a decent property should be cash flow positive. You will also notice that most private real estate syndications and funds use about the same amount of leverage.

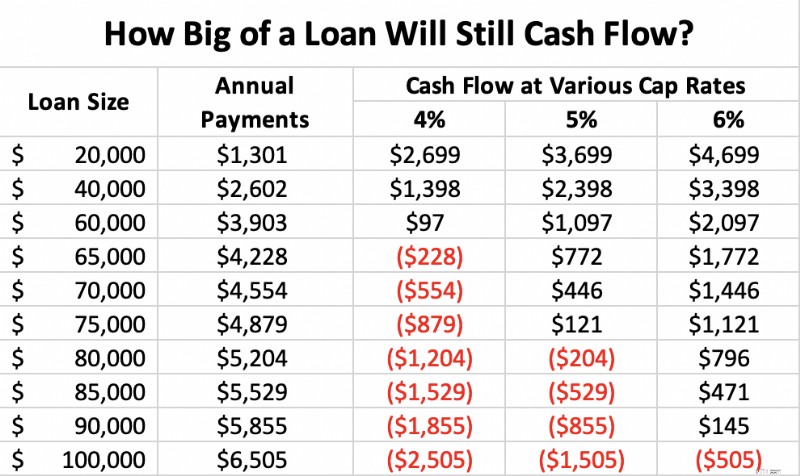

Consider a $100,000, cap rate 4-6 property (meaning if it were paid off, it would provide a $4,000-$6,000, 4%-6% cash-on-cash return to the investor). If, after all of its costs, it can generate $4,000-6,000 in cash, then it suggests you could pay up to $4,000-6,000 in mortgage costs and still avoid a negative cash flow situation. If you get a 30-year fixed mortgage at 5%, your annual payments would be as follows at the various cap rates:

As you can see, whether a property cash flows depends on three factors:interest rate, cap rate, and down payment. With a 5% interest rate and a 4% cap rate, you need to put down a lot of money, 40% in this case, to ensure positive cash flow. When the interest rate and cap rate are equal (5% in this case), the property cash flows with a 25% down payment. When the cap rate is higher than the interest rate, you can put down as little as 10% and still have positive cash flow. As I write this [2021] , cap rates in various cities across the country average at most 3%-4%, and investment property interest rates are in the 3.5%-4.5% range, suggesting you'd better plan to put down at least 25%-33% as a down payment to stay cash flow positive—and a whole lot more than that in Miami or Naples, Florida.

This is the most common question I get, particularly from new attendings who have more great uses for cash than they have cash. I have written about it many times, but this particular question does not lend itself to easy answers. It always depends, and there are a lot of variables:

Here is a priority list that may help guide you that no one will argue with too strenuously:

<オル>Honestly, the most important thing is not exactly what your money goes toward. Paying down debt is a good thing. Investing is a good thing. Both build your net worth. The most important thing is how much of your income goes toward building wealth either by paying down debt or investing. Concentrate on that.

I find it interesting to talk to wealthy people about how they did it. The same drive that leads the wealthy to save money in order to invest it also drives them to save money in order to pay down debt. In my experience, rich people do both, middle-class folks try to decide whether to pay down debt or invest, and the poor do neither. There's probably a mindset lesson there.

My family chose to be debt-free. We paid off our mortgage in 2017 and haven't looked back. In some ways, it's just a status symbol. By doing it, we get to make videos like this one:

There are some benefits of being debt-free besides just a status symbol. These include:

<オル>Some people consciously and deliberately choose not to seek the debt-free life for financial reasons that have nothing to do with overspending. They note that debt has a substantial number of financial benefits including increased investment returns, less overall risk, and lower taxes. In this section, I'll explain how that can be, as well as provide some guidelines as to how you can profitably incorporate debt into your financial plan without taking unsafe risks.

As we discuss debt and its uses, it is important to understand the characteristics of any given debt before you decide to incorporate it into your plan.

<オル>As you can see, the ideal loan to carry to invest is with a long-term, fixed-interest rate, unsecured, deductible, non-callable debt. Unfortunately, there is no debt that meets all of those characteristics. The usual choices are:

We've talked about how investing on leverage can raise returns, but investing is not just about returns. It is also about risk control. When you take on debt, you introduce leverage risk into your portfolio. Investing is a single-player game:you against your goals. You should ask yourself, “How much leverage risk do I need to take in order to reach my goals?” Many high-income professionals like doctors will appropriately conclude that they don't need to take any leverage risk at all, but some do because they had a late start, don't want to save much money, or simply have particularly aggressive goals.

However, what if you could take less overall risk by introducing leverage risk to the portfolio? There are other risks in investing, such as market risk, sequence of returns risk, liquidity risk, and inflation risk.

Thomas J. Anderson points out in his Value of Debt books that there are two ways to get to a 9% return. The first is to invest in assets that return 9%. The second is to invest in assets that return 6% but leverage them with debt. It is possible that you can have a lower volatility portfolio with debt than without. So while you have introduced leverage risk, you have reduced market risk.

One of the biggest risks in retirement is sequence of returns risk. This is the risk that despite having adequate average returns over the investment period, the retiree runs out of money because all of the crummy returns came first and decimated the portfolio while the retiree was withdrawing from it to live. This risk is highest right around the time of retirement, perhaps the last two or three years before you retire, and the first 5 years afterward, because that is when the portfolio is largest. By using debt earlier in the accumulation phase and perhaps later in the decumulation phase, you can spread out the amount of time that such a large part of the portfolio is exposed to market risk.

Rather than decreasing your asset allocation around the time of retirement, you simply reduce your leverage risk around that time. Alternatively, rather than selling low if stocks plummet shortly after you retire, you simply take out a margin loan against the remaining assets and spend that, so you do not sell your stocks low. Later, when the portfolio recovers, you can sell the stocks and pay off the loan.

Sometimes people run into liquidity risk. They simply need cash now and despite being wealthy, they have no cash. It might be tied up in long-term, illiquid investments or perhaps it is just in volatile investments, like stocks, they do not wish to sell while they are down in a bear market. Cash obtained from borrowing can provide cash and liquidity in these times.

Another big risk retirees face is inflation risk. This risk is much lower for accumulators, because they have jobs with wages that tend to rise with inflation and because they also have fixed debt that becomes easier to pay off in the event of high inflation. Retirees can also protect their nest egg with long-term, non-callable, fixed low-interest rate debt. It works exactly the same way. There is obviously a cost to this protection (the interest), but that can be offset or even superseded by additional investment earnings from the borrowed but invested money.

Most of us also face substantial liability risk. Debt can also improve our asset protection. For example, in some states very little home equity is protected. If you have another place to put that money that has better asset protection (retirement accounts or, in some states, a whole life policy), you could “equity-strip” that home equity out with a mortgage or HELOC and move it into the better-protected vehicle. Likewise, you could maintain loans against investment properties inside LLCs to limit the amount of money available to a creditor of the LLC. A margin loan against a taxable account could work similarly.

Thus, there are a number of strategies and circumstances where additional debt could actually lower your overall risk instead of increasing it.

A really cool aspect of debt is that it provides spendable cash without any tax consequences. You can borrow against your house, your car, your investment account, your rental properties, or your whole life insurance policy and get a lump sum of non-taxable cash. It isn't income. It's debt. So, you don't have to pay taxes on it. In fact, when combined with the step-up in basis at death on your house, investment account, or rental properties, or the tax-free death benefit of a whole life policy, there are no taxes due for you or your heirs for the use of that money.

Essentially, one can elect to pay interest instead of taxes. People accuse the wealthy of doing this to avoid paying “their share” of taxes, but in reality, it is a tax strategy available to all of us with anything to borrow against. It isn't always the right strategy—particularly if the interest rate on your debt is high, life expectancy is long, and the basis on your asset is also high. But it is silly for someone on hospice to sell low basis investments instead of just borrowing against them.

In retirement, you don't really need income. What you need is spendable money. The things you pay for do not care where the money to pay for them came from. It can be borrowed money, it can be tax-free Roth IRA money, it can be partially taxable withdrawals from your non-qualified account or Social Security, it can be tax-sheltered income from investment properties, or it can be fully taxable withdrawals from a tax-deferred account. The choice is yours, but there can certainly be times where the right option is borrowed money.

If you subscribe to this idea that borrowed money can boost your returns, lower your risk, and decrease your taxes, you will eventually come around to two questions. The first is what debt you should actually carry. There are lots of options here, including auto loans, RV loans, parental student loans, and more, but most people settle into some combination of

As I mentioned before, money and debt are fungible, so it doesn't really matter what secures the loan so much as the characteristics of the loan—term, interest rate, security, deductibility, and callability. You can even take out debt on stuff that your kids are using as a method of transferring money to them during your life.

The second question you will run into is how much debt you should take on. I briefly mentioned Thomas J. Anderson above, who has spent far more time thinking about this question than I have. He basically advocates that individuals act like corporations do and take on an optimal amount of debt. His conclusion? That your debt should get to within 15-35% of your total assets by the time you are within 20 years of retirement. Then you should maintain that “optimal ratio” throughout retirement as best you can through spending, taking out additional loans, and trying not to pay down the loans you have by using interest-only mortgages.

So if you have a $600,000 house, $1 million in retirement accounts, a $400,000 rental property, and a $1 million taxable account ($3 million total), he recommends you have somewhere between $450,000 and $1.05 million in attractive debt. Not too much, not too little. Adjust to your own taste, debt tolerance, and debt availability.

But Anderson is advocating for “enriching debt”—debt that helps you get richer. He's not talking about working debt (needed student loans, practice loan, needed mortgage, needed small car loan) or oppressive debt (that 29% credit card and fat 8% car loan keeping you poor). Plus, his books are so full of cautions about who should actually attempt this that it leaves you wondering whether you're even in that elusive group. Should you be like Katie and me, pay off your debts, and live the debt-free life? Or should you seek a moderate path and carry substantial debt to the grave in hopes of boosting returns, lowering risk, and decreasing your taxes? I cannot say, because the answer depends too much on you. Different strokes for different folks. Here are some considerations as you decide, however.

I will use some of Thomas's rules and some of my own.

Are you a devout Muslim, evangelical Christian, or a member of The Church of Jesus Christ of Latter-day Saints? Carrying debt into retirement probably isn't compatible with your religious beliefs, nor is it required for success for most high-income professionals. This approach probably isn't for you.

The vast majority of people clearly are not capable of handling debt well. I mean, 45% of Americans are carrying credit card debt month to month. This is not a good plan for them. If you're used to borrowing to buy cars, boats, and other consumer goods, this may not be a good idea for you, either.

In my experience, most doctors are way too comfortable with debt. Most young doctors have ratios that are way over what Thomas would recommend already. Consider a dentist with a $500,000 practice loan, a $500,000 student loan, a $500,000 mortgage, and a $500,000 house. What's that ratio? At least 150%, five times as much as that 15-35% ratio. Even if the dentist buys into the “keep an optimal amount of debt forever” philosophy, they need to really attack that debt and build assets to drop that ratio rapidly.

Maybe you're in a situation where debt is not going to be easy to get. Maybe you're 60, retired with inexpensive cars, a $2 million IRA, a $300,000 paid-for house, no kids, and no taxable account. Where are you going to get a $300,000-$600,000 debt with good terms?あなたではない。 This strategy really isn't an option for you.

Leverage risk is real and sends people to bankruptcy court all the time, even previously successful real estate investors. What happens if you lose your job and the stock market drops 75% and the value of your home drops 40%? Are you still OK? Can you still pay all of your living expenses? Can you still make your debt payments? If not, your debt ratio is too high, even if it is in the 15%-35% range.

We're all human. We get tempted to buy stuff we shouldn't buy with money we don't have. You might have an opportunity to take on a high-quality debt. But you might already be at your goal of a 20% debt ratio. Therefore, you should not take on this new debt. You don't want to just collect investments and you don't want to just collect debts. They all need to be part of the plan. You need to make sure the other side of the plan is smart, too. Are you borrowing all this money just to put it into Bitcoin, Tesla stock, and inverse leveraged ETFs, or are the investments you are purchasing sensible, long-term investments such as index funds and appropriately priced rental real estate?

The object is to get rid of low-quality (high-interest rate, short-term, non-deductible) debt while building an optimal debt ratio of high-quality debt. It can make sense to borrow against your portfolio or house to pay off credit card debt in order to save on interest rate, but you have to stay within your ratios or you could get in trouble. It would be terrible to lose the ability to service the debt right after converting an unsecured debt to a secured one!

The bottom line is:

<オル>If the answer to any of those is no, I would instead recommend the pathway I have taken—pay off your debts rapidly but in a methodical, rational way and live debt-free for the rest of your life.

What do you think about debt? How have you used debt in your investing life? How have you gotten in trouble with it? Do you plan to pay off your debts in a rapid fashion, in a moderate fashion, or continue to use debt strategically throughout your life?