投資初心者の多くは、投資ポートフォリオを設計して実行しようとするときに、圧倒され、どこから始めればよいのかわかりません。彼らはこの仕事にとても無力感を感じており、振り返ってみるといつもとても簡単に思えるので、財務アドバイザーに助けを求めます。残念なことに、一部のライターは、ファイナンシャル アドバイザーの 93% は単なる営業マンであるため、これらの世間知らずの投資家の多くは正しいスタートを切れないと示唆しています。

DIY 投資は大変かもしれませんが、これを実現できます。 投資ポートフォリオを設計および実行するときに覚えておくべき重要な原則は、「近道をしない」です。これは非常に基本的なことのように思えるかもしれませんが、頻繁にスキップされるため、ポートフォリオ設計のプロセスで多くの問題が発生します。

プロセスは簡単ですが、順番に進めることが重要です。

<オル>一度に一歩ずつ進めていくと、シンプルでありながら洗練された投資ポートフォリオを自分で設計して実装できるようになります。あるいは少なくとも、アドバイザーが「川に売り込む」ときを知るために必要なスキルと知識を身につけることができます。

ステップ 1 — 目標を設定する

ステップ 2 — 資産配分を作成する

ステップ 3 — 資産配分を実装する

ステップ 4 — 計画を維持する

投資ポートフォリオを設計する最初のステップは、そのポートフォリオの目標を設定することです。それは、退職金を支払うため、子供の教育費を支払うため、最初の住宅を購入するため、死亡時に慈善寄付をするため、あるいは死亡時に一定の資産を相続人に残すためかもしれません。

目標は具体的であるほど良いです。必要な金額と必要な正確な日付を正確に指定する必要があります。良い目標の例としては、「2035 年 9 月 1 日にジュニアの 529 プランで 100,000 ドルを獲得したい」などがあります。目標が曖昧に定義されている例としては、「いつか引退できるようになりたい」、「投資でできるだけ多くのお金を稼ぎたい」、「億万長者になりたい」などがあります。

当然のことながら、人生の状況や目標は年とともに変化します。それで大丈夫です。目標、計画、ポートフォリオは決まったものではありません。計画は後で変更される可能性があるという考えに基づいて最初から計画を立てることを妨げると、実際に計画を立てるメリットは得られません。さらに、目標に向けてどれくらい貯蓄する必要があるかを実際に計算したことがなければ、ほぼ確実に貯蓄額が少なすぎるという間違いを犯し、目標を達成することができなくなります。

目標が 5 年以内であれば、インフレを無視してもおそらく問題ありません。それより長い場合は、「実際の」数値、またはインフレ後の数値を使用する必要があります。つまり、この目標を達成するには年間 20,000 ドルを節約する必要があると計算した場合、それは (明日のドルではなく) 今日のドルで 20,000 ドルに相当するため、おそらく毎年少しずつ寄付する必要があることになります。必要なリターンを計算するときは、より低いインフレ後のリターンも使用する必要があります。

何らかの目標に向けて貯蓄する場合、返済の順序が重要です。つまり、理想的には、貯蓄額が少ない初期には低い収益が得られ、巣の卵が大きくなった後はより高い収益が得られます。これから説明するような計算は本質的に単純化されているため、その限界を認識してください。また、金融市場は物理学とは異なることに留意してください。これらは複雑な社会制度であり、保証はほとんどありません。未来が過去と大きく異なる可能性は十分にあります。そのため、過去のデータは懐疑的な目で見てください。

節約する必要がある金額について、何らかの見積もりを作成する必要があります。 3年以内に購入したい住宅の場合、それは比較的簡単かもしれません。同様の住宅の価格を調べて、20% 値下げに必要な金額を計算し、価値が上がった場合や成約費用に備えてさらに数パーセント追加することもあります。

目標が複雑になるにつれて、見積もりも複雑になります。たとえば、3 歳児の母校の授業料を支払うことが目標の場合は、いくつかの仮定を立てる必要があります。現在の 4 年間の授業料が 40,000 ドルで、授業料は一般的なインフレ率より 2% 増加すると考えたとします。 Excel などのお気に入りのスプレッドシートを取り出し、これをセルに入力します。

=FV(2%,15,0,-40000)

=$53,834.73

最初の数字は年間収益率です。 2つ目は年数です。 3番目は各年に支払った金額、最後は現在持っている金額です。この計算により、40,000 ドルの授業料が 15 年後にいくらになるかがわかります。その目標を達成するには、今日のお金で 54,000 ドルが必要です。

退職後の巣の卵の金額を見積もるのはさらに複雑です。このテーマに関しては、多くの研究が書かれており、さらには本全体が書かれています。

基本的なプロセスは次のとおりです。

<オル>たとえば、現在のドルで年間 100,000 ドルが必要だと見積もっており、年金はなく、社会保障がインフレに応じて年間 30,000 ドルを拠出すると予想します。したがって、インフレに連動して年間 70,000 ドルをポートフォリオに拠出する必要があります。研究を検討した結果、3.5% の出金率 (70,000 ドル/0.035 =200 万ドル) に満足できると判断しました。したがって、あなたの目標は、「2040 年 7 月 1 日までに退職後の貯蓄として (現在のドルで) 200 万ドルが欲しい」ということになるかもしれません。

投資ポートフォリオの目標がわかったところで、必要な貯蓄額とポートフォリオの必要なリターン、つまり取る必要のあるリスクの関係を調べます。

資産配分の概念について説明し始め、将来価値関数と、貯蓄する必要がある金額、ポートフォリオの収益、時間の関係についてさらに詳しく説明します。

スプレッドシートを再度開き、この将来価値関数をセルに入力します。

=FV(5%,20,-60500,0)

=2,000,490.22

この関数は、何もない状態 (0) から始めて、年間 60,500 ドルを 20 年間貯蓄し、インフレ後に毎年 5% の利益を得た場合、20 年後には現在のドルで 200 万ドルを手に入れることができることを示しています。さて、毎年6万ドルを節約するには、非常に多額のお金のように思えます。つまり、あなたの収入は 20 万ドルしかなく、多額の住宅ローン、私立学校に通う 2 人の子供、高額な税金、そしてポルシェの支払いもあるのですよね? 200 万ドルという数字を達成するには、他にどのような選択肢がありますか?

4 つの用語はすべて相互に依存していますが、この概念は投資計画にとって非常に重要であるため、十分な時間を費やす必要があります。年間30,000ドルしか節約できないとしましょう。まだ始めるものが何もなく、それでも投資で実質 5% の利益を得たと仮定しましょう。 200 万ドルという数字に達するまでにどれくらい時間がかかりますか?

=FV(5%,30,-30000)

=$1,993,165.43

さらに10年。うーん。あなたは今、高額な住宅ローンを組んで大きな家を買うか、あと10年長く働くか、どちらかを決断しているところです。他にどのような選択肢がありますか?

そうですね、相続財産を得ることができるので、すでに退職金口座に 30 万ドルあるとします。年間 30,000 ドルを節約し、実質収入の 5% を得る場合、今どれくらい働かなければなりませんか?

=FV(5%,21.75,-30000,-300000)

わずか 21 年 9 か月で 200 万ドルに達します。

しかし、30 万ドルの学生ローンを抱えていて (話を簡単にするため、金利が 0% であると仮定しましょう)、本当にあと 25 年で退職したいと考えている場合はどうなるでしょうか?ローンを返済するために毎年いくら貯蓄/使用する必要がありますか?

=FV(5%,25,-63200,300000)

年間 63,200 ドルになります。

何が可能なのかを理解するために、この関数を自分で少し試してみることができます。

それはとてもクールだ、とあなたは言います。今、自分に力が与えられていると感じませんか?これで、あなたもファイナンシャル アドバイザーが驚かせるような派手なチャートやグラフをすべて作成できるようになります。

しかし、その機能には、あなたにとってコントロールするのがはるかに難しい要素が 1 つあります。それは、リターンです。リターンを 2 倍にできたら素晴らしいと思いませんか?

たとえば、年間 30,000 ドルしか貯めたくない、今は何も持っていない、それでも 20 年後には引退したいと考えているとします。どのような種類のリターンが必要ですか?

=FV(11.3%,20,-30000,0)

それは11.3%です。ポルシェを売ったり、小さな家に住んだりするよりも、11.3% のリターンを得るほうがはるかに簡単だと思いませんか?なぜそうしないのでしょうか?

収益の源は金融市場です。市場のリターンを予測することは不可能であり、ましてやコントロールすることは不可能です。これは、株式市場、債券市場、不動産市場、商品市場、その他の投資対象の市場にも当てはまります。リスクの量はコントロールできますが、実際のリターンとの相関関係は中程度にすぎません。期待収益の概念を理解することが重要です。

期待リターンは、一定レベルのリスクに対して、平均して長年にわたって得られると期待されるものです。特に、世界中や自分の都市や国で頻繁に起こる複雑な経済的および政治的変化を考慮すると、何年も経っても保証はありません。しかし、何が起こるか全く分からない場合、どれくらい節約する必要があるかを見積もることもできません。

リターンを見積もる際に参照できる情報源の 1 つは過去です。すべての投資目論見書に記載することが法律で義務付けられているように、過去の収益は将来の収益を示すものではありません。しかし、それらはさまざまな可能性を定義するのに役立ちます。

現実的な株式市場のリターン

たとえば米国の株式市場を見てみましょう。 1976 年の創設以来、低コストのバンガード 500 インデックス ファンドに投資していた場合、1976 年から 2020 年の平均名目 (インフレ前) リターンは年率 9.51% になります。 1976年10月から2020年までのインフレ率は平均約3.51%だった。したがって、米国株式市場の実質収益率 (配当を含み、非常に低い投資コストを差し引く) は 6.00% です。

未来が過去と同じで、100% 株式ポートフォリオに投資する場合、期待収益率 6.00% を計算に使用できます。この数字が上で説明した 11.3% とどれほど違うかに注目してください。これは、年間 30,000 ドルしか貯蓄せず、20 年後に 200 万ドルで退職するという計画がいかに非現実的であるかを示しています。たとえこの 6.00% を達成したとしても、目標には 896,000 ドル届かないことになります。

債券市場のリターン

債券についてはどうですか?バンガードは 1986 年にトータル ボンド マーケット ファンドを開始しました。それ以来の年平均リターンは 5.93% です。この期間のインフレ率は 2.58% で、実質リターンは 3.35% になります。これを期待リターンとして使用すると、株式 50%、債券 50% のポートフォリオでは、リバランス ボーナスを考慮せずに、4.68% のリターンが期待されることになります (詳細は後ほど)。

私たちは長期的な株式と債券のリターンに関するデータをさらに持っており、最良のデータセットは 1920 年代に遡り、中には数百年前に遡るものもあります。しかし、これらの数字は上で説明したものとそれほど変わりません。

収益を考えるもう 1 つの方法は、理論的な観点から見ることです。

理論上の債券リターン

もし債券投資家がこの時点から今後4%の実質リターンを本当に期待しているなら、ほとんどの当局は彼に「そんなのは狂っている」と言うだろう。過去数十年間、債券のリターンが比較的良好だった理由の一つは、金利が低下し、債券のリターンに良い追い風を与えたことだ。 1989年末時点で10年国債の利回りは約8%だった。今ではその半分以下の収量になっています。将来の債券リターンを予測する最良の材料は現在の利回りであり、これは名目 (インフレ前の) 数値です。かなり憂鬱ですね?

理論上の株価収益率

実際の株式リターンを理論的に見積もることもできます。最も一般的な方法は、割引配当モデルです。基本的には、期待される GDP 成長率に期待される配当利回りを加算します。投機的要因もありますが、長期にわたっては、通常は無視できます。この記事が最初に書かれた2020年時点のS&P 500の利回りはほぼ2%でした。エコノミストらは長期的なGDP成長率を約3%と予想していた。これらを合計すると、実質リターンは 5% になります。

これらの理論的リターンを使用すると、株式 50%、債券 50% のポートフォリオの長期期待実質リターンを 2.5% で計算できます。

より多くのリターンを期待して、より多くのリスクを取る方法があります。株式を中心としたポートフォリオに投資することもできます。また、マイクロキャップ、小型株、新興市場株など、理論的に期待収益が高いリスクの高い株式を含めることもできます。

不動産は、特に大きなレバレッジを利用した場合、ある程度の高い収益も約束します。

しかし、肝心なのは、ポートフォリオの収益計算で使用すべきインフレ後の予想収益率は 2% ~ 7% の間であるということです。あなた (またはあなたのアドバイザー) が 10% または 12% を使用して計算している場合、あなたの計画はおそらく失敗する運命にあります。

再び将来価値関数に戻りましょう。 25 年後に 200 万ドルが欲しいが、今何も持っていない場合、年間 65,500 ドル (リターン 2%) から 31,700 ドル (リターン 7%) の間のどこかに貯蓄する必要があります。ポートフォリオのリスクが高く、将来の経済について楽観的であればあるほど、貯蓄できる額は少なくなります。しかし、年間 20,000 ドルを積み立ててもそれは減りませんし、50,000 ドルでも十分ではないかもしれません。

ポートフォリオ設計のステップ 1 は、具体的な目標を設定することであることを忘れないでください。資産配分の実行を開始するときは、投資ポートフォリオで達成したい具体的な目標を思い出してください。これらの目標を達成するには、貯蓄する必要がある額と、ポートフォリオの複利収益によって負担となる重労働の量との関係を認識することが重要です。私が「どれくらい貯める必要があるのかが分からないと、十分な貯蓄ができないでしょう?」と私が言った理由を見てください。快適な老後を過ごすには、ほとんどの人が考えているよりもはるかに多くの貯蓄が必要です。

複数の資産クラスのポートフォリオを設計する場合、最も難しいステップの 1 つは、どの資産クラスを含めるべきかを決定する 2 番目のステップです。

理想的な資産クラスには 3 つの重要な特徴があります。

<オル>「資産クラス」に 10 株しか含まれていない場合、それはあまり良い資産クラスとは言えません。

私の意見では、ポートフォリオには少なくとも 3 つの資産クラスが必要です。 7 は、シンプルさの利点と、複雑なポートフォリオのパフォーマンス向上の可能性との間のかなり良い妥協点です。 10 を超えると、自分が何か良いことをしていると自分を騙しているだけで、実際にはいじくりのためのいじりをしているだけです。 3 ~ 7 の資産クラスを超えると、収益逓減の法則が実際に働き始めます。

比較的一般的な資産クラスは数十個思いつきます。真に分散されたポートフォリオの利点を得るために、それらすべてを含める必要がないことは簡単にわかります。また、一部の広範なファンドでは、一度に複数の資産クラスにアクセスできます。

実際、The Oblivious Investor でブログを書いている Mike Piper 氏は、ポートフォリオ全体を単一のマルチアセットクラスの投資信託に変更しました。シンプルでありながら洗練されています。

追加する資産クラスが増えるほど、ポートフォリオはより複雑になります。これにより、いくつかのことが行われます。

複雑さは気にしないかもしれませんが、配偶者や相続人のことも考慮する必要があります。相続人が、最近亡くなった最愛の人のポートフォリオに 200 の個別株とさらに 50 の投資信託が含まれていることを発見することは珍しいことではありません。あなたがそのようなポートフォリオを持って死んだら、彼らは何をするつもりだと思いますか?彼らは最寄りのエドワード ジョーンズ店に駆け込み、その人たちを雇って代わりにやってもらうつもりです。

また、ポートフォリオが 5 つ以上の異なる種類の口座に分割されている場合、15 の異なる資産クラスがあると、その追跡が非常に複雑になることにも留意する必要があります。しかし、すべての投資が 1 つの Roth IRA にある場合、おそらくそれはそれほど問題ではありません。

ウィリアム・バーンスタインが課税対象のテッドとシェルタード・サムに関する優れた議論で述べたように、投資が主に課税口座にある場合は、おそらくポートフォリオに多数の狭い資産クラスを含めるよりも、より少数のより広範な資産クラスを必要とするでしょう。これにより、個々の投資の節税効率が向上するだけでなく、将来のリバランスも簡素化されます。

他の人が使用していない資産クラスを含める機会もあるかもしれません。ポートフォリオを設計する際には、これらを考慮する必要があります。これは、401(k) の内容に応じて決まる場合もあれば、個人のビジネスに関連する場合もあります。

たとえば、私が軍隊にいたとき、政府の 401(k)、つまり TSP にアクセスできました。この非常に低コストのプランには、非常に低コストで提供される海外先進市場インデックス ファンド (I ファンド) と、バンガードを含む他のどこで購入するよりもはるかに安い拡張市場ファンド (S ファンド) が含まれています。機会がいかに魅力的だったかを考えると、ポートフォリオを設計する際にこれらの構成要素を使用することは理にかなっていました。さらに、TSP は他では提供されていない資産クラス、G ファンドを提供しています。これは強力なマネー マーケット ファンドであり、10 年物国債の利回りと 3 か月物国債のリスクを提供します。

他の人は、REIT ファンドとはまったく異なる機能を持つ TIAA-CREF 不動産ファンドにアクセスできる場合があります。手術センター、救急医療、さらには病院のシンジケート株式を購入する機会もあるかもしれません。この固有の資産クラスはあなただけが利用できる可能性があるため、複数の資産クラスのポートフォリオを構築する際にはそれを考慮する必要があります。

マットレスのお金: これは家や貸金庫に保管しているお金です。これは、自然災害の後に街を出る途中で受け取ることができる物理的なお金です。それは、20 ドル紙幣の束、4 枚ロール、あるいは金貨かもしれません。米ドル、ポンド、ユーロ、さらには円建ての場合もあります。おそらく緊急資金の一部としてこの一部を保有する価値はありますが、この資産から期待される実質収益はインフレ率の正反対です。

普通預金、当座預金、マネー マーケット口座: これは銀行にあるお金です。マットレスのお金ほど手が届きませんが、少なくとも少しの利益は得られます。そのリターンは一般にインフレ(特に税引き後)にすぎず、現在[2022年] です。 インフレよりもはるかに低いです。しかし、安全で流動性が高く、通常は FDIC の保険でカバーされています。マネー マーケット ファンドは、1 株あたり 1 ドルの価値を維持しようと努める投資信託です (通常は成功しています)。歴史的に、短期金融市場口座は銀行口座よりもわずかに高い利回りを提供してきました。お金は安全であり、資産クラスが変化しても非常に流動的です。

CD: 規則は銀行によって異なりますが、通常、この譲渡性預金 (CD) のお金は非常に簡単に入手できますが、早期に引き出した場合は通常、利息がいくらか失われます。このお金は FDIC によって保険されており、通常、特に長期の場合、通常の貯蓄金利よりも多くの収益が得られます。

確定利付国債: 非常に安全で、非常に現金に近い米国政府向けの短期 (1 年未満) 融資です。歴史的には、税引前インフレをほとんど上回っていません。

国債: 米国政府への最長 30 年間の長期融資。元本価値は金利の変化によって大きく変動する可能性がありますが、それでもかなり安全な投資であると考えられています。通常、彼らのリターンはインフレをわずかに上回ります。

外国国債: 国債と似ていますが、為替リスクも負うことが異なります(債券が建てられている通貨と比較してドルが上昇した場合、損失が発生します)。明らかに、一部の政府は他の政府よりもデフォルトする可能性が高くなります。

物価連動債券: 米国では、これには TIPS 債券と I 債券が含まれます。基本的に実質リターンが保証されており、予想外のインフレも債券でカバーされます。外国政府や一部の企業もこれらを発行しています。理論的にはリターンは同等の名目債券よりも低くなるはずですが、その理由は完全には明らかではありません。

社債: 企業への融資。金利リスクに加えて、デフォルトのリスクもあります。これらは国債よりもリスクが高いため、通常はリターンがわずかに高くなります。これらは、期間およびデフォルトのリスクごとにさまざまなサブクラスに分割できます。リスクの高い社債はジャンク債として知られています。

外国社債: 国内社債と似ていますが、為替リスクがあります。一部の投資信託では、そのリスクをヘッジして事実上排除していますが、その代償として期待収益は低くなります。

ピアツーピア融資: 個人向け消費者ローンへの投資。初期収益は期待できますが、デフォルトのリスクが途方もなく高くなる可能性があります。流動性と投資の管理に必要な時間も懸念事項です。

住宅ローン担保証券: これらの債券は住宅所有者への住宅ローンで構成されています。他の種類の資産担保証券もありますが、これらが最も一般的です。

スライス アンド ダイス アセット クラス: モーニングスターは、株式市場を表示するための 9 ボックスの方法を開発し、株式をサイズ (大型、中型、小型) および価値/成長の連続体 (価値、ブレンド、成長) ごとに分類しました。これにより、大型株から小型株までの 9 つの資産クラスが提供されます。これら 9 つの資産クラスにはすべてプラス面とマイナス面があり、ポートフォリオに合理的に組み込むことができます。ただし、一部の専門家は「宝くじ効果」のため、小さな成長は避けるべきだと主張しています。

セクター資産クラス: 米国経済 (したがって株式市場) は、金融、テクノロジー、エネルギー、ヘルスケアなどを含む多数のセクターに分割されることがよくあります。これらのセクターは少なくとも 11 あります。

REIT: 株式市場で取引されているにもかかわらず、多くの投資家はREITが他の株式とは根本的に異なるため、単なるセクターではなく別の資産クラスとみなすことができると感じています。多くの人気のある静的ポートフォリオ (エール大学やコーヒーハウスなど) には、REIT の別個のスライスが含まれています。

貴金属株: これらは、金、銀、プラチナなどを採掘する企業です。ウィリアム・バーンスタインなど一部の人は、これらを別の資産クラスとみなしています。貴金属は、金や銀の IRA アカウントにとって、この方法で退職後の生活を始めたいと考えている人にとって素晴らしい資産です。

マイクロキャップ: リック・フェリ氏など、多くの人はマイクロキャップを別の資産クラスと考えている。これらは株式市場で公開取引されている最小の株式です。理論上のリターンは有望です。これはうまく投資するのが難しいクラスであることが判明したため、実際の収益は期待外れになる可能性があります。

店頭在庫: これらは証券取引所に上場できるほど大きくない小規模企業の株式であり、「ピンクシート」で売買する必要があります。この資産クラスへの投資には重大な問題(特に透明性と詐欺の蔓延)があり、おそらくほとんどの医師投資家は避けるべきです。

これらの資産クラスのほとんどは、一般的にリターンがインフレを大幅に上回ると予想されますが、ボラティリティが大きく、一時的および恒久的な損失のリスクが伴います。

国際株式: 国内株式における上記の資産クラスはすべて、世界のどの国でも再現され、何百もの「資産クラス」が生み出される可能性があります。 (ブラジルのマイクロキャップのヘルスケア株を思い浮かべてください。)しかし、一般に、国際株式資産クラスについて話すとき、これらの資産クラスを指します。

国際バリュー株や国際小型株も一般的に保有される資産クラスです。

貴金属: これには、金、銀、銅、プラチナなどが含まれます。多くの投資家は、ポートフォリオにこれらの 1 つまたはすべてを保有しています。期待される長期リターンはインフレから経費を差し引いたものだが、他の資産クラスとの相関性が低い(そして終末論的な価値があるとも言われている)ため、多くの人が保有している。それは、自分が所有する金属として、他の人が所有する金属として、その他さまざまな方法で保持できます。すべてにプラスとマイナスがあります。特に金は、期待外れのリターンが長期間続く傾向と、短期間に顕著なリターンが現れる傾向があります。

エネルギー: 石油、ガス、天然ガス、ウラン、石炭、さらには代替エネルギーにも直接投資できます。それらの先物契約を購入できます。それらを生産、精製、輸送する企業の株を買う。井戸を買う。あるいはパートナーシップ(MLP)を組んで投資することもあります。 これらにはそれぞれプラス面とマイナス面があり、大きなリスクを負い、驚異的なボラティリティに耐えることにより、期待できるリターンが期待できます。この人たちは天候のためにノースダコタに住んでいるわけではありません。

農産物: トウモロコシから小麦、「豚バラ肉」、カカオに至るまで、あらゆるものに「投資」できます。商品先物担保ファンドがポートフォリオに組み込まれる余地があると示唆する人もいる。期待リターンはインフレに近いため、これらを長期ポートフォリオに追加するケースは主に、株式や債券などのより伝統的な資産クラスとの相関が低いことに基づいています。もちろん、コモディティには投機家がたくさんいます。

非貴金属: 鉄鋼、アルミニウム、銅など。これらには農産物と同様の問題があります。

通貨: さまざまな手段を使用して通貨の変動を推測できます。期待される実質収益はコストを差し引くとマイナスになります。

暗号通貨: ビットコインのような暗号通貨は、広く使用されている通貨ではなく(まして安定通貨でもない)、安定した価値の保存手段がないため、主に投機の手段です。ここ数年非常に人気がありましたが、私が大金を投じるようなものではありません。詳細については、こちらをご覧ください。

オルタナティブ投資: ラリー・スウェドローは、優れた著書『The Only Guide to Alternative Investments You'll Ever Need』の中で、20 の異なるオルタナティブ資産クラスをリストしています。これらのことを掘り下げる前に、この本を一読する価値は十分にあります。このリストではそこまで詳しくは説明しません。

金融商品: これには、生命保険、年金、オプション、先物、仕組み投資、優先株(社株と社債の組み合わせ)、カバードコール、転換社債、その他のデリバティブが含まれます。これらのオプションにはそれぞれ可能性がありますが、商品は複雑になる傾向があり、その複雑さはほとんどの場合、投資家よりも発行者に有利になります。

プライベート エクイティ: 多くの企業は株式公開されておらず、株式市場で取引されています。だからといって、彼らが良い会社ではないというわけではありません。これは投資するのが難しい資産クラスである可能性があり、多くの場合、高い最低投資額と「誰かを知る」ことが必要です。いくつかの記事は、リターンが過去に多くの人が考えていたほど良くないことを示唆しています。公開市場に比べて明らかに透明性が劣ります。

ヘッジファンド: ああ、お金持ちの投資ですね。世の中には十数種類のヘッジファンドがあります。彼らの最近の人気は、その才能を著しく希薄化させている。問題は、法外に高い報酬を補うのに十分な才能のある人材がかつて存在したのかということだ。シンプルなポートフォリオを設計する場合、おそらくほとんどの人が避けるべき領域です。

収集品: そう、もしあなたが数百年前にモナリザを買っていたら、かなりうまくやっていたでしょう。 Not exactly a mainstream investment product, this category includes everything from art to Beanie Babies to baseball cards. These are generally hobbies, not investments.

There are more asset classes than you can shake a stick at. You obviously don't need most of them. Let's discuss how to allocate between them to form an asset allocation.

The process of deciding your investment portfolio asset allocation is very personal, because there really is no single right answer. There probably isn't even a single right answer for you. There are literally hundreds of reasonable asset allocations that, combined with a reasonable savings rate, will allow you to reach your financial goals. Don't worry too much about getting this step perfectly right. Besides, portfolios that are only slightly different only perform slightly differently. Perfect can be the enemy of good here. Consider these five aspects as you build your portfolio.

A portfolio is traditionally composed of risky stocks and relatively riskless bonds. The ratio between these two is the most important factor for determining both the risk and the return of your portfolio and is the first thing to decide when putting your asset allocation together.

John Bogle's rule is that your stock allocation percentage should be approximately 100% minus your age. So if you're 25, you should have 75% stocks. If you're 75, you should have 25% stocks. No rule of thumb should ever be hard and fast, and there are plenty of good reasons to not follow this rule. But if you're not sure where to start, this is a great place.

Some have argued for as much as a “120 minus your age” rule, but I'll be honest:when I start seeing people advocating this, it usually is after a long run-up in stocks and shortly before the beginning of a bear market. That would put a 50-year-old at 70% stocks, which is probably a little on the aggressive side. I have two pieces of advice for you when deciding on your stock-to-bond ratio.

First, Benjamin Graham suggested you should never have more than 75% of your portfolio in stocks or less than 25% of the portfolio in stocks. Warren Buffett claims that everything he knows about investing, he learned from Benjamin Graham. I suggest you listen to those two. Your portfolio is not the place to be an extremist.

When you are first developing your portfolio, I suggest you be more conservative than you think you should until you pass through the fire of a bear market the first time to see how you react. The worst possible outcome for a portfolio is for you to sell low during a bear market just before your retirement. I have two colleagues who did just this.何だと思う? They're still working shifts.

The time to learn your true risk tolerance is not during the last bear market before your retirement. It's during the bear market you go through in your 20s or 30s. During the bear market of 2008-2009, the US stock market declined more than 56%. Other asset classes, such as emerging market stocks and REITs, lost even more. The US stock market declined approximately 90% during the Great Depression. You should expect to lose at least half of the money you have invested in stocks 2-3 times during your investing career.

That means at least a 25% loss on a 50/50 portfolio. If you've never watched several years' worth of savings evaporate before your eyes, you don't know what it feels like in your gut to go through that. DO NOT overestimate your risk tolerance. It is far better to underestimate it. You can always ramp up the risk after your first bear market managing your own portfolio if you find you can tolerate it. In my experience, it is far more common for people to take on more risk than they can handle, and most end up buying high and selling low.

Another difficult question for a portfolio manager (that's you, if you're managing your own) is how much of the portfolio you should expose to the unique risks faced by international stocks, including currency risk. There are lots of good reasons to invest internationally, including significant diversification benefits and the possibility of outstanding returns in many countries.

I personally recommend you invest at least 20% of the money designated for stocks in your portfolio in stocks of countries outside your home country. In my opinion, the maximum you should invest in international stocks is the market weight, which is currently about 55% of your stocks. Any number between those is reasonable.

One very reasonable way to invest is to just buy all the stocks and all the bonds. For example, you could design a portfolio that is 1/3 Total Stock Market Index (US Stocks), 1/3 Total Bond Market Index (US Bonds), and 1/3 Total International Stock Index (Non-US Stocks). This has many benefits, including ultimate diversification, very low costs, and simplicity.

However, there are also good arguments for “tilting” the stock portions of your portfolio to riskier assets. That means holding MORE than the market weights of riskier assets such as value stocks, small stocks, junk bonds, and emerging market stocks. The hope is that you'll have higher long-term returns to compensate you for taking the additional risk.

An example of a tilted portfolio would be 25% Total Stock Market, 10% Small Value, 25% Total International Stock, 10% Emerging Markets, 25% Total Bond Market, and 5% Junk Bonds.

How Much to Tilt Your Portfolio?

Once you've decided you WANT to tilt your portfolio to some riskier asset class, you're left with the decision of how much to tilt it. The more you tilt, the more theoretical return you will get, but you have to weigh that against the loss of diversification and the additional risk. The reason small stocks have a higher expected return is that the risk is higher that they may not get that expected return, even in the long run. It's a bit of a Catch-22.

I suggest moderation in all things. Although some authorities have advocated putting all of your stock allocation into risky asset classes, such as small value stocks, I recommend you keep your tilts small enough that you still have a significant chunk of your portfolio invested in all the stocks in the world and all the investment-grade bonds in your currency.

Some investors also like to “slice up” their fixed income allocation. The smaller your stock-to-bond ratio, the more important this issue becomes. I suggest you keep some portion of your fixed income in investment-grade nominal bonds or their equivalents (CDs or perhaps the TSP G Fund) and some portion in bonds indexed to inflation, such as TIPS. The percentages I leave up to you. If your bond allocation is relatively small and you want to keep it simple, there's nothing wrong with putting your entire fixed allocation into a total bond market fund.

As I mentioned above, there are dozens, perhaps hundreds, of reasonable asset allocations. I've outlined a number of popular ones here. The most important thing really isn't the specific portfolio you choose. The important thing (once you choose a reasonable portfolio) is that you stick with it through thick and thin, modifying it rarely, only for very good reasons, and after giving it great thought over a period of months. But for the novice asset allocator, I will provide three examples of portfolios I consider reasonable—and five portfolios I do not consider reasonable.

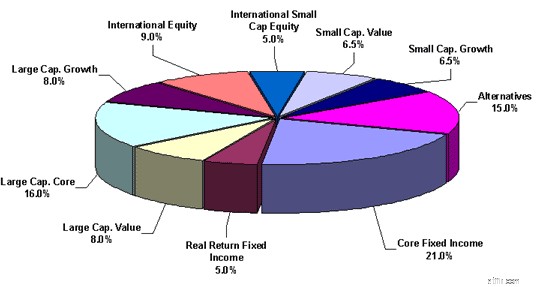

Reasonable Portfolio #1 — Relatively aggressive, with a tilt to small and some alternative asset classes

Reasonable Portfolio #2 — Conservative and Simple

Reasonable Portfolio #3 — The portfolio of an asset-class junkie

Unreasonable Portfolio #1 — Extreme, lacks diversification, and/or lacks growth potential

Unreasonable Portfolio #2 — Lacks diversification due to no low-risk asset classes

Unreasonable Portfolio #3 —Too much international tilt

Unreasonable Portfolio #4 — Bizarre, huge tracking error, lacks diversification

Unreasonable Portfolio #5 — Too complicated and slices are too small

It's now time to implement the asset allocation. This involves selecting the actual investments to fulfill the asset allocation, deciding what types of accounts to use, and determining where you should locate each investment within those accounts.

You've basically got three choices when you select investments:

<オル>I favor passively managed mutual funds for three main reasons:

#1 Active Management Is Really Hard

If this is news to you, I suggest a quick read of Rick Ferri's The Power of Passive Investing. He puts together academic studies done over decades that demonstrate that while beating the market is possible, it is highly unlikely and becomes more unlikely the longer the investing time period and the more investments that need to be selected.

#2 Active Management Is Really Expensive

In fact, that's a big part of the reason why passive funds outperform active funds. (The other big reason is primarily behavioral.) Years ago, the only funds available were actively managed. That provided a benefit to investors since they could get wide diversification at a much cheaper price than they could get themselves. There was little focus on “beating the market” since you couldn't buy the market.

When index funds showed up, other mutual funds had to focus on beating the market, and it turned out it was much harder to do than anyone imagined. The expense ratio on funds easily available to any investor is less than 0.1% per year or less than $1 per $1,000 invested.

#3 Passive Management Is Really Easy

You select a fund based on only three factors:

You don't have to learn all about the manager's background, evaluate their track record, and constantly monitor their activity so you can get out quickly if they ever “lose their touch.” You just buy it and forget it. Passive investors get mad when their fund doesn't have a return within a few basis points of the benchmark index, which is a pretty rare event for most popular index funds.

Some people spend a lot of time worrying whether to use traditional index mutual funds or ETFs. The truth of the matter is that it doesn't matter all that much. Expenses are similar, and true advantages of one over the other for most investors are minimal. Mutual funds are generally easier to use since you don't have to interact with the market, but in some of the more obscure asset classes, an ETF is markedly better than a fund.

The process for most of us goes like this:if I want, say, 5% of my portfolio in REITs, I look for a passively managed REIT fund and put 5% of my portfolio in it. I want 5% of my portfolio in emerging markets, so I look for the best passively managed emerging markets fund and put 5% of my money in it. It's pretty simple.

If you're not sure where to start looking for passively managed funds, go to Vanguard. You don't necessarily have to have all your investments at Vanguard, but you probably ought to have a pretty good reason to invest somewhere else.

The hard part is the asset allocation, not the selection of the investments. But too many people don't do these steps in order, and that's where things seem confusing and complicated.

This step can make a big difference. I'm often surprised to see people not using the appropriate type of accounts for their situation. For example, a resident who isn't investing for retirement in a Roth IRA. Or parents saving for their children's college in a taxable account instead of their state's 529 plan. Or a doctor at the peak of her earnings career choosing a Roth 401(k) or even a taxable account instead of maxing out his tax-deferred 401(k) contributions. Everyone's situation and outlook are a little different, but using the right accounts for the right reason can make a huge difference in your after-tax returns over the years.

If all of your investment accounts are tax-protected, this step doesn't matter so much. If you have a significant taxable investment account, however, you need to pay attention to this step. As a general rule, you should use tax-protected accounts as much as possible, and when you have to invest in a taxable account, you should place your tax-efficient assets there first. So if only 50% of your investments are within tax-protected accounts, and your desired asset allocation is:

Then you'd want to rank the assets in order of tax-efficiency. Here's that list in order from most efficient to least efficient:

You would then place your assets like this:

Tax-protected accounts 50%

Taxable account 50%

There are a few subtleties to this process, but in general, it's pretty straightforward. If you're not quite sure you're doing it right, consider posting your desired asset allocation and how you're planning on implementing it on the WCI forum or Facebook Group. You'll have valuable feedback within minutes and some reassurance that you're doing it right.

The final step in designing a solid, low-cost, do-it-yourself portfolio is managing your portfolio. As we've discussed, the easiest (and undoubtedly one of the smartest) portfolios you can have is a fixed-asset allocation of low-cost index funds. There are a few tasks that remain.

An important part of planning for the future and maintaining your asset allocation is to track your returns. This need not be done on a daily basis, but should at least be looked at once a year and tracked over the long term. I suggest you use the XIRR function to do so. As the years go by, this data becomes more and more valuable. If, for example, your plan for financial independence is to have $2 million in 25 years and you determined upfront that you need to save $42,000 a year and average 5% real returns (after taxes and expenses) to reach that goal, you ought to calculate your returns as you go along to see how you're doing. If after seven or eight years you see that you're actually only getting 4% real returns, then you can adjust by saving more money or perhaps even taking a little more risk than you thought you had to in the portfolio. Perhaps your plan was to get 10% real returns, and you realize how unlikely that seems to be after a few years of investing. You can now adjust the plan to spend less in retirement, work longer, or save more now. Investing without calculating your overall returns is like going on a road trip and never looking at a map, a GPS, or the road signs. You may run out of gas before you get there.

A static asset allocation is going to be knocked out of balance by varying market returns. If you want to maintain the same level of risk in your portfolio, you'll need to rebalance back to the original asset allocation from time to time. For the beginning investor, with a small portfolio compared to his annual contributions, this is easily done by directing the new contributions to the asset classes that haven't done particularly well recently. As the portfolio grows, it may occasionally become necessary to actually sell something that has done well to buy something that hasn't.

Studies show you shouldn't rebalance more often than every year or two, so some people just do it on their birthday every year. Others rebalance when the portfolio becomes out of whack by a certain amount, by using the 5/25 rule (or similar). You should try to avoid any tax consequences when rebalancing, as the benefit of rebalancing could easily be eliminated by the tax costs. This means doing your rebalancing predominantly within tax-protected accounts. You can also use distributions (dividends and capital gains) to new contributions to rebalance, further decreasing the need to sell appreciated securities within a taxable account.

You occasionally may come up with a good reason to change your asset allocation. This should occur rarely, and when I say that, I'm not talking every week or two. I'm talking once a decade or so. Remember, this is a strategic asset allocation we're talking about, not a tactical asset allocation. You don't change it in response to security valuations or recent market events. You need to be very careful about performance chasing, which is a very natural tendency that most investors fall into. I suggest you give yourself a waiting period, perhaps even 3-6 months after deciding to change the asset allocation before doing so. You may be surprised to see that after a three-month wait, you no longer think that change was such a good idea. Here are a few reasons why you might want to change your asset allocation:

Decrease in Risk – In general, as you get older, closer to retirement, and closer to your financial goals, you probably want to dial down the risk a bit, with safer assets like bonds and less risky assets like stocks. You may want to decide now how you plan to do this. Decreasing stocks by 1% a year or 10% a decade or whatever. You may also find you simply don't need to take as much risk after a raise, particularly strong market performance, or an inheritance.

Change in Life Circumstances – Perhaps you get married and your spouse doesn't like you investing in microcaps or you find you need a higher return than you originally anticipated. You may also gain access to different asset classes through a new 401(k).

Add an Asset Class – Every now and then, a new asset class comes along. If, after evaluating it, you find you want to add it to your portfolio, it's OK to do so. I do recommend you be very careful about performance chasing, however. It's easy to do, even for the “right reasons.”

Buy into a New Theory – You may come across some new investing research or theories that indicate a change in investing strategy. Examples from the past include the development of mutual funds, the development of index funds, the development of REITs, 3-Factor analysis into the benefits of small and value stock investing, or even momentum investing.

Last, and perhaps most importantly, once you develop your portfolio, you need to stay the course. This is much easier said than done.

Not only do you have to ward off the constant urge to tinker, but you need to avoid reacting to market ups and downs. It helps if you don't pay any attention to the financial news. Investment consistency is far more important than the particular asset allocation you choose (as long as it is something reasonable). Changing horses in mid-stream is a recipe for getting wet.

You can do this, and we can help. In fact, we're more than happy to help you. To explore thousands of more posts from WCI over the past decade, you can start here. WCI also has plenty of relationships with a number of high-quality, pre-vetted partners that can assist you with financial planning, retirement accounts, tax planning, and real estate investing.

Does this plan for building and managing a portfolio make sense to you? Or did you go about it a different way? Did you have success? Do you wish you could have taken this path instead?

[This updated post was originally published as a series in 2012.]