この国には 400,000 を超える保険代理店があり、ほぼすべての保険代理店が終身保険を販売したいと考えています。年間保険料が 40,000 ドルの保険を購入した場合、その代理店の手数料は通常 20,000 ドルから 44,000 ドルの間になります。ご想像のとおり、特に保険代理店の収入の中央値が 49,840 ドルであることを考えると、この手数料は大きなモチベーションとなります。さらに悪いことに、最悪の保険の多くは最高の手数料を提供しています。残念ながら、販売されている保険契約の大部分は不適切に販売されており、販売者の大多数は金融アドバイザーを装ったセールスマンです。

この馬鹿げた利益相反の結果として、代理店は、あなたに自社の商品を購入するよう説得するために、いくつかの深刻な神話を投げかけることがあります。これは、この商品を購入した人の80%以上が死ぬ前にその商品を処分するという忌まわしい統計を説明するかもしれませんし、このサイトと私たちのFacebookグループの実際の医師への世論調査では、終身保険を購入した人の大多数が購入を後悔していることが示されています。これがすべてあなたにとってニュースである場合は、この投稿を続ける前に、終身保険について知っておくべきことをすべて読んでください。

WCI FB グループのメンバーのほとんどは終身保険に加入したことがありませんが、加入している人の 76% は加入したことを後悔しています。

読み込み中 ...

このサイトで実施中の世論調査では、数字は似ていますが、わずかに低くなります (FB グループとは異なり、これらの保険を販売する人による投票が許可されています)。

私が終身保険を嫌いだと思っている人はたくさんいます。実際にはそうではありません。私はその販売方法とそれを不適切に販売する人々が大嫌いです。それがどのように機能するかを本当に理解し、それでも必要な場合は、好きなだけ購入してください。それは本当に私にはどちらの影響もありません。しかし、購入時にその仕組みを理解していなかった読者やリスナーに遭遇するのはうんざりで、理解できてももう欲しくないのです。

終身保険はさまざまな方法で設定できますが、一般的には、定められた期間または死亡するまで、毎月または毎年の保険料を支払います。保険料の支払い期間が長ければ長いほど、保険料は安くなります。あなたが死亡すると、受取人は保険金を受け取ります。どの終身保険も死ぬまで持ち続ければ支払いが保証されているため、保険料は同等の定期保険よりもはるかに高くなります。

終身保険は、他の種類の終身保険と同様、実際には保険と投資のハイブリッドです。この保険は年が経つにつれて現金価値が蓄積されます。その現金価値は税金で保護された方法で増加し、そこにあるお金を非課税で(ただし無利子ではありません)借りることもできます。死亡すると、借りた金額(および利息)が死亡保険金から差し引かれ、残りが受取人に支払われます。 (現金価値または死亡保険金を受け取ることになります。両方を受け取ることはできません。)

この投資の側面により、終身保険を販売する人は、それを購入すべきあらゆる種類の創造的な理由と、それを構成するための創造的な方法を見つけることができます。最も極端な支持者は、住宅ローン、消費者ローン、保険、投資、大学の貯蓄、退職金など、あらゆるニーズに対応できるのは終身保険なので、一生他の金融商品は必要ないとさえ主張するかもしれません。

問題は、終身保険を利用するたびに、その経済的問題に対処するより良い方法があるのが通常であるということです。この記事は、終身保険の支持者によって宣伝されている、終身保険に関する 38 のよくある誤解です。

収入を守るのに最適な方法は終身保険ではなく、定期保険です。退職する前に、自分が早死にした場合に備えて、安価な定期生命保険に加入できます。健康な 30 歳が購入した額面 100 万ドルの 30 年水準プレミアム定期生命保険は、年間 680 ドルになります。同様の終身保険の場合、年間8,000ドルから10,000ドルと10倍以上の費用がかかります。これは、住宅ローンの支払いや休暇に費やすことも、退職後の資金に投資することもできないお金です。

永続的な死亡保険金を受け取るには、終身が最善の方法ではありません。無失効が保証される普遍的な生命保険が最適です。いつでも死亡時に支払われる保険を必要としている、または望んでいる少数の人々がいます。これは、不動産計画に関する特殊な問題に役立つ場合があります。ただし、これを提供し、終身保険よりもはるかに安価な優れた商品があります。これは無失効保証ユニバーサル生命保険と呼ばれます。 。現金価値を蓄積するものではなく、単に生涯にわたる死亡保障を提供するものです。費用は終身保険の半分だけなので、この販売における代理店の手数料がはるかに低くても驚くことはありません。

冷笑的だと言われても構いませんが、それが、無期限の宇宙生命の保証について聞いたことがない理由の1つではないかと思います。終身保険は、保証された死亡保険金を提供しますが、ゆっくりと増加すると予測されています (ただし、保証はありません)。そのため、平均余命かそれ以降に死亡した場合、元の保険契約の死亡保険金よりも少し多く残ることになります。

私が最近調べた終身保険では、30歳で購入した100万ドルの保険の死亡保険金は、83歳死亡時の死亡保険金が317万ドルになると予測されていました。これは素晴らしく聞こえますが、死亡保険金のインフレ保障とほぼ同じです。過去のインフレ率が 3.1% 程度であることを除けば。 3.1% であれば、現在の 100 万ドルは 53 年後には 504 万ドルに相当します。終身保険は予期せぬインフレによって壊滅的な打撃を受けるでしょう。配当は主に名目債券によって裏付けられており、高インフレ環境ではその価値が失われることになるからです。

したがって、終身保険は、生涯にわたって保証された名目死亡給付金や、生涯にわたって保証された実質死亡給付金を提供する最良の方法ではありません。それで、それは何に良いのでしょうか?保険会社が増額したいと思えば増額する可能性がある死亡保障保障についてはどうでしょうか。そのために2倍の保険料を払いますか?そうは思いませんでした。

生涯をかけて投資するのが最良の方法ではありません。従来の投資は最良の方法です。終身保険料を支払うと、お金の一部は保険の購入に使われ、一部は保険会社の諸経費と利益に、そして一部はセールスマンの手数料に使われます。残りは保険契約の現金価値部分に入ります。

保険会社は毎年配当を発表し、現金価値部分が 10,000 ドルで配当が 6% の場合、600 ドルが現金価値に加算されます。配当は支払われた保険料全体ではなく、現金価値にのみ適用されます。そのため、平均配当率は、投資としての保険契約の実際の収益とはまったく関係ありません。実際、少なくとも 10 年間は投資収益率がマイナスになるのが一般的です。私は最近、平均余命が53歳の健康な30歳の男性を対象とした政策を分析しました。 50 年後、現金価値に対する保証収益率は年間 2% 未満でした .

保険会社の楽観的な「予測」値を使用したとしても、利回りは 5% 未満です。実際には、おそらく 3% ~ 4% の利回りになるでしょう。この「投資」を 50 年間続けなければならないことを考えると、それはそれほど大きな代償とは思えません。投資に数十年かかる場合は、より多くのリスクをとって投資し、より高いリターンを得る方がはるかに賢明です。株式や不動産への投資では、数十年間で 7% ~ 12% の範囲の収益が得られる可能性があります。 100,000 ドルを年 3% で 50 年間投資すると、438,000 ドルに増加します。代わりに 9% で成長した場合、最終的には 740 万ドル、つまり 17 倍の金額になります。長期投資の複利率は、特に長期間にわたって重要です。

代理店の中には、保険会社があなたや私が他では見つけられない投資収益を何らかの方法で得て、その大きな収益を保険契約者に還元できると信じている人もいます。保険会社の内部を覗いて、実際に保険会社のポートフォリオに何が含まれているかを確認すると、啓発されることがあります。 2016年、保険会社の資産は67%が債券(ほぼすべてがありふれた社債と国債)、1%が優先株、12%が普通株、8%が住宅ローン、1%が不動産、4%が現金、2%が保険契約者へのローン、そして約5%が「その他」に投資されていた。インデックスファンド革命のおかげで、個人投資家は年間 10 ベーシスポイント未満の経費でほぼすべての商品を購入できるようになりました。アクティブ運用は、保険会社にとって投資信託ほどうまく機能しません。

ご想像のとおり、主に国債 (現在利回り 1% ~ 2%) と社債 (現在利回り 3% ~ 4%) で構成されるポートフォリオの収益はそれほど高くありません。では、配当金はどこから出てくるのでしょうか?一部は投資ポートフォリオの収益から、一部は保険を解約した人の手数料から、そして一部は「死亡クレジット」から来ています。これは基本的に、死亡者数が計画よりも少なかったため、受取人に支払う必要がなかったお金です(つまり、州の規制により、そもそも保険の保険部分に支払いすぎました)。保険会社が投資できる魔法のような投資で、保険会社なしでは投資できないものはありません。あなたと投資との間に層が追加されると、支出が増加し、収益が低下するだけです。

分散型ポートフォリオに含める価値のある資産クラスはたくさんありますが、生涯はその 1 つではありません。保険のセールスマンは、人生そのものが素晴らしい投資であるということをあなたに納得させることができないとわかると、たいていこのような議論に訴えます。株式、債券、不動産のポートフォリオに組み込むと全体のポートフォリオが改善されると言われています。ただし、任意のものをアセットクラスと呼ぶことができます。馬糞は資産クラスになる可能性がありますが、だからといって投資すべきというわけではありません。このように考えてください。次のような特徴を持つ資産クラスがあると言ったとしたら:

<オル>買いますか?もちろん違います。

投資税額を下げるには終身が最良の方法ではなく、退職金口座が最適です。多くの代理店は終身保険の税制上のメリットを宣伝することを好み、しばしば 401(k) や Roth IRA と比較します。現金価値は税金で保護された方法で増加し、現金価値は非課税で借りることができ、死亡時の保険金から得られる収入は(遺産ではありませんが)非課税となります。そのため、終身保険の支持者の中には、401(k) や Roth IRA のような退職金口座の代わりに終身保険を使用することを推奨する人もいます。ただし、401(k) または Roth IRA を利用すると、より多くの節税効果が得られ、より高い収益が得られる可能性が高いリスクの高い投資に投資できるだけでなく、その特権のために自分でお金を借りたり、利子を支払う必要もありません。

私は以前、401(k) が税金を節約する 3 つの方法と、終身保険がいかに Roth IRA と異なるかについて投稿しました。また、課税投資口座での節税効果の高い投資は、エージェントが言いたがるほどの税負担がかからないことについても投稿しました。生命保険に投資すると節税効果はあるのでしょうか?はい、しかし、劇的に売られすぎています。

保険代理店は、資産保護の問題について偏執的な医師に対してこの手法を好んで使用します。しかし、資産保護法が非常に州固有のものであることについては、あまり言及されていません(あるいはおそらく知らないこともあります)。例:[2022] , アラバマ州では、終身保険の現金価値のうち 500 ドルのみが債権者から保護されますが、401(k) または IRA のお金の 100% は保護されます。ウェストバージニア州は 8,000 ドルの保護のみを提供しています。サウスカロライナ州は4,000ドルを保護。ニューハンプシャー州は何の保護も提供していない。多くの州では、終身保険の現金価値に対して 100% の保護を提供していますが、この神話に陥る前に、おそらく州の特定の法律を調べる必要があります。

キャッシュバリュー型生命保険には、非常に役立つ優れた資産計画機能がいくつかあります。しかし、医師を含む大多数の人はこれらの機能を必要としません。生命保険の主なメリットは、死亡時に多額の所得税が免除されることです。これは、高価な不動産や個人事業の所有権など、多くの流動性問題の解決に役立ちます。あなたの不動産を平等に共有したい2人の子供がいて、あなたの不動産の大部分が家族の農場である場合、平等に共有するには、農場を売却するか、半分に減らすか、一方にもう一方を買い取ってもらう必要があります。しかし、農場と同じ価値の生命保険にも加入していれば、一人の子供が農場を手に入れ、もう一人の子供が保険金を受け取ることができます。同様に、幸運にも非常に大きな財産(連邦税法では独身者の場合500万ドルを超えるが、一部の州ではそれよりも低い場合もある)を持っている場合には、生命保険の収益を相続税の支払いに使用することができます。これは、相続人が 1 人であっても、相続人が税金を支払うために貴重な不動産や事業を投げ売り価格で売却するのを防ぐのに役立ちます。

また、財産の規模を減らして相続税を回避するために、取消不能な信託の中に生命保険を入れることを好む人もいます。代わりに、単純な課税対象の投資を信託に預けることもできますが(その方がより高い収益が得られる可能性が高いでしょう)、信託税率は非常に高くなる可能性があり、面倒な要素は言うまでもなく、税金効率の悪い投資の収益に重大な足かせとなります。生命保険によって相続税が節約されるのではなく、信託に預けることで死ぬ前に資産を手放すことができるという事実であることを指摘することが重要です。

しかし実際には、アメリカ人の大多数は、医師であっても、さらには「相続税問題」を抱えている医師も含めて、効果的な相続計画を立てるために終身保険を必要としていない。ほとんどの人は相続税を負担することなく死ぬでしょう。相続税の支払い義務がある人の大部分は、税金の支払いに使用できる流動資産を持っています。相続税を防ぐために遺産の規模を減らしたい場合でも、生命保険に加入しなくても簡単に減らすことができます。あなたとあなたの配偶者はそれぞれ 16,000 ドルを寄付できます[2022 — 最新の数字を入手するには年間数字のページをご覧ください] 相続税や贈与税の影響を受けることなく、任意の年の相続人に贈与されます。たとえば、4 人の子供がいて、それぞれに 4 人の子供がいて、20 人の相続人全員が結婚している場合、40 人になります。 40 x 16,000 ドル x 2 =年間 128 万ドルが、相続税や贈与税を支払うことなくあなたの財産から取り出されます。この税率であれば、相続税の上限を下回るのにそれほど時間はかかりません。保険は必要ありません。

エージェントの中には、子供の大学費用を支払うために終身保険を利用することを提案する人さえいます。これはできますか?もちろん。政策ローンを借りて、そのお金を大学に送金して授業料を支払うだけです。しかし、いくつかの理由から、良い 529 を使って大学に向けて貯金をしたほうが良いでしょう。まず、終身保険では利用できない 529 を使用することで州税の軽減が得られることがよくあります。次に、529 からお金を借りる必要はなく、引き出すだけです。利息の支払いは必要ありません。最後に、もちろん重要なことですが、大学の貯蓄の期間を考慮してください。親は通常、5~20年かけて大学進学のために貯蓄します。その資金を積極的に投資することで、7%~10%のリターンが期待できます。終身保険は、20 年未満の期間では収益率が非常に低くなります。実際、生涯を通じての「投資」に対する現金価値リターンは、少なくとも 10 年間はマイナスになることがよくあります。あなたのお金があなたと同じくらい一生懸命働き、終身保険の最初の10年間はお金が休暇であることを確認することが重要です。終身保険の支持者は、死亡した場合でも死亡保険金で短期大学の学費を支払うことができるが、そのリスクを定期保険でカバーする方がはるかに安いと指摘するでしょう。

保険代理店は、顧客が実際には永久死亡保障の必要性をまったく感じていないことが指摘されると、この議論に戻ることがあります。彼らは、顧客が実際には終身保険を必要としていないことを認めています。そして、それをステータスシンボルや贅沢品として持つことに基づいて販売しようとします。 「確かに、それは必要ありません、それは贅沢です。」贅沢とは定義上、必要のないものです。私は自分の贅沢が本当に楽しめるものであることを好みます。したがって、贅沢品として終身保険に加入する前に、「自分にとって本当に楽しいことは何だろう?」と自問してください。終身保険を所有している場合は、加入しても問題ありません。しかし、私たちのほとんどは、素敵な車、孫たちとのクルーズ、あるいはお気に入りの慈善団体への寄付などの贅沢を好むでしょう。

お金を使い果たさないようにするための最善の方法は、生涯を通じてではなく、資産の一部を年金化することです。 2番目に死ぬ問題に対処するには、終身が最善の方法ではなく、年金や年金を適切に構築することが最善です。終身保険代理店は、特に夫婦の場合、終身保険を所有しなければならない、または少なくとも所有したいと感じさせる退職後のシナリオを考え出すことを好みます。たとえば、働いている配偶者が死亡するまでしか支払われない年金について話します。あるいは、夫婦の片方だけの生涯に基づいて資産の一部を年金化することについて話し合うかもしれません。そして、終身保険の収益を2番目に亡くなった配偶者の生活費に充てるよう提案するでしょう。このように終身保険を利用する理由はありません。お互いが死ぬまで年金を継続したい場合は、そのオプションを選択してください。二人とも死ぬまで年金を継続したい場合は、そのオプションを選択してください。はい、支払われる率はわずかに低くなりますが、支払額の差は、年金の損失をカバーする終身保険契約の費用よりも小さいです。それは問題に対する正しい解決策ではありません。終身保険は退職後の柔軟な対応を可能にしますか?もちろんですが、その柔軟性の代償は高すぎます。

一生かけて高価なものを買うのが最善の方法ではなく、そのために貯金するのが一番です。世の中には、Bank on Yourself や Infinite Banking などのシステムを提唱する、非常にクリエイティブな保険セールスマンがいます。基本的なスキームは次のとおりです。払込済みの追加で保険契約を適切に構成することで、初期の数年間で多くの現金価値を保険契約に組み込むことができ、8 ~ 15 年ではなく 3 ~ 4 年で損益分岐点になります。 「非直接承認」の保険も購入します。これは、保険契約から借入すると、保険会社は借入前の金額に基づいて配当金を支払い続けるため、保険契約の配当金によって実質的にローンの利息支払いが相殺されることを意味します。車、冷蔵庫、投資用不動産が必要なときに、普通預金口座や銀行にお金を借りに行くのではなく、終身保険から実質的に無料で借りられるようになりました。さらに、借りない保険での現金の価値は、貯蓄銀行のお金よりも早く増加します。

それで、何が問題なのでしょうか?問題は、必要のない終身保険に加入しなければならないことです。従来の保険に比べてより早く損益を達成できる可能性もありますが、それでも数年間はマイナスのリターンが続き、長期的には同様に低いリターンが続きます。 5年後に年間4〜5%を稼ぐのと、1年目から年間1%を稼ぐのはどちらが良いでしょうか?まあ、最初の6、7年は年1%の普通預金口座を使ったほうが良いでしょう。また、金利が過去の最低水準から上昇した場合でも、残りの人生はこの制度に縛られることになります。マネーマーケットファンドから5%以上の利益を得られるようになったのは、それほど昔のことではありません。また、ディーラーで非常に低い金利で車を融資することも非常に簡単であるようです。 0% や 1% も珍しくありません。保険契約から 5% で借りるよりも、1% で借りたほうが賢明です。家電製品や住宅ローンについても同様の問題です。自分から借りるためにこれだけの努力をしたのに、他の人から借りたほうが安いことに気づくのです。最後に、5 年または 10 年間購入する必要がない場合は、終身保険よりもはるかに高い収益が期待できるものに投資する時間があります。自分自身に頼っている人は詐欺に遭っているのでしょうか?必ずしもそうとは限りませんが、彼らは一般的にその制度のメリットを過大評価されています。その支持者は主に、創造的なマーケティングを通じて売上の増加を目指す保険代理店です。大きな買い物をするには、終身保険に加入するよりも貯蓄する方が良い方法です。

終身保険の支持者、特に保険契約を銀行として利用することを主張する人は、多くの非常に裕福な人々や多くの企業(銀行を含む)が実際に終身保険を購入していると指摘するのが好きです。それは真実ですが、一般の人にとっては無関係です。大企業には、中産階級の個人が持つような節税のための退職金口座オプションを利用することができません。超富裕層はすでにこれらを最大限に活用しています。必要以上のお金を持っているときは、お金のリターンはそれほど重要ではありません。ビル・ゲイツは、一生懸命働くために自分のお金を必要としないため、2%〜5%の収益が得られるものに投資する余裕があります。それは、医師を含む中流階級から上流階級の人々の大多数にとってはまったく当てはまりません。上で説明したように、超富裕層は、限られた財産計画上の給付金や終身生命保険の資産保護給付金をより多く利用しています。要するに、人生全体に特有の収益の低さは、あなたにとっての問題よりも彼らにとってははるかに小さいということです。

終身保険のセールスマンは、若いうちに購入したほうが終身保険がずっと安いと好んで指摘します。 55歳で保険に加入するよりも25歳で保険を購入した方が保険料が安いのは事実ですが、お金の時間的価値と、さらに30年間保険料を支払うことになるという事実を考慮すると、若い年齢での投資が高齢になってからの投資よりも優れているというわけではありません。アクチュアリーは非常に賢い人たちで、死亡などのモデル化が比較的容易なリスクについては、非常に効率的に保険の価格設定を行うことができます。

保険料の安さ以外にも、若いうちに買った方が良いと思われる理由は他にも2つあります。まず、手数料はより多くの年にわたって分散されるため、全体的な収益への影響が少なくなります。しかし、手数料をまったく支払わないという選択肢の方がはるかに魅力的です。第二に、人生の後半では、健康状態が悪化したり、危険なスポーツを始めたりする可能性があります。これは、生命保険を投資として利用する場合の重大な欠点の 1 つです。誰もが利用できるわけではありません。まったく加入資格がないか、保険価格が高すぎて投資収益率が通常よりもさらに低くなっているかのどちらかです。それが若いうちに買う理由ではなく、まったく買わない理由だと思います。バンガードが S&P 500 ファンドを購入させる前に、あなたの家に救急隊員を派遣して採血させたらどうなるか想像できますか?

終身保険は障害から退職後の収入を守る最良の方法ではなく、障害保険が最適です。終身保険の保険料は非常に高額で、障害が発生した場合に保険料を支払うのが困難であることを認識し、保険会社は障害が発生した場合に保険料を免除する特約の提供を開始しました。この特典に対して追加料金を支払う必要がないように見える場合もあります。この戦術に引っかかる人はいくつかの点を見逃しています。まず、保証は無料ではありません。保険会社が保証に追加料金を請求するか、「保険に組み込んで」非表示にするかにかかわらず、すべての保証には収益が低下するという形で費用がかかります。

第二に、障害保険は複雑であり、障害の定義はすべて重要です。障害補償を希望するほとんどの医師は、障害が発生した場合に会社が支払わなければならないことを確認したいため、「職業」の補償を含む広義の障害を含む非常に優れた保険に多額のお金を費やしています。終身保険で販売されている特約はそれほど包括的ではなく、障害がよくあるグレーゾーンの部分で支払われる可能性ははるかに低くなります。プレミアム特約を生涯免除するよりも、より大きな障害保険を購入した方が良いことはほぼ確実です。障害保険には退職金補償特約が付いている場合もあります。これらにも問題はありますが(主に給付金の支払方法に問題があります)、終身保険から障害保険を得ようとするよりは優れています。

私と同じように早期リタイアを計画している人は、少なくとも数年間多額の貯蓄をした後であれば、退職金を守るために障害保険は必要ないことに気づくかもしれません。 40 歳で 75 万ドルのポートフォリオを持つことを考えてみましょう。退職後には現在のドルで 200 万ドルが必要だと考えます。あなたは、50 歳でそれを達成して退職できるように、多額の貯蓄を計画しています。障害を負い、お金をすべて貯められなくなった場合のバックアッププランは何ですか?障害保険は 50 歳まで支払われるだけではなく、65 歳まで支払われるため、その 15 年間をカバーするポートフォリオは必要ありません。障害給付金がなくなるまでに社会保障給付金の受け取りを開始することもできます。ポートフォリオに手を加える必要がないため、ポートフォリオは成長し続けることができます。インフレ後も 5% 成長すると、65 歳になる頃には現在のドルで 250 万ドル以上の価値があることになります。必要のない保険には加入しないでください。しかし、何らかのポートフォリオを構築する前であっても、退職後の貯蓄を守る最善の方法は、終身保険から保険を得ようとするのではなく、より多くの障害保険に加入することです。たとえ追加の補償を利用して退職後のポートフォリオを提供できたとしても、それを高いリターンの投資に投資できる必要がありますが、これは生涯を通じて得られる可能性は低いです。障害のある場合の主な収入である障害保険金は非課税となるため、積極的に投資する課税口座は問題ありません。

代理店は新しい保険を販売するたびに新しい手数料を受け取るため、たとえ同じ会社の古い保険を交換する場合でも、代理店があなたに推奨することには重大な利益相反が生じます。私はこのブログで多くの保険代理店と交流していますが、「適切に構成された」終身保険がどのようなものであるかについて他の保険代理店と同意する人は一人もいません。つまり、2番目のエージェントに行けば、ほぼ確実に、もっと良い方法があると教えてくれるでしょう。しかし、ある政策を別の政策に交換する価値があるためには、特に数十年後には元の政策が絶対にひどいものでなければなりません。その理由は、終身保険の収益率の低下が初期に集中しているためです。最近ある政策を調べてみました。これは、最初の 25 年間は追加料金が支払われる投資として設定されました。これは、保険契約の収益を最大化するための代理店の最善の試みでした。年率換算のリターンは次のとおりです。

保証 予測 最初の 10 年間 - 1.84%0.98%次の 15 年間 2.55%5.47%次の 25 年間 1.99%5.13%これは、悪い収益が初期に非常に集中していることを示しています。この特定の政策では、25 年後には有償加算が停止されるため、収益は実際に減少します。より伝統的なポリシーでは、3 列目は 2 列目よりわずかに高くなります。しかし、この話の教訓は、まず「正しい保険」を購入するべきだということです。たとえ 10 年以上経ったひどい保険であっても、真新しいより優れた保険よりも優れたものになるでしょう。これは、たとえ最初に加入したのが間違いだったとしても、古い終身保険を維持し続けることが良い考えである理由でもあります。また、保険会社が実際にリスクをほとんど負っていないことも注目に値します。保険会社は、現金の価値がインフレに追いつくことさえ保証していないからです。

自分の死亡時に所得税を免除して相続人にお金を渡す唯一の方法は終身ではありません。実際、Roth IRA は最良の方法ですらない。あなたが死亡すると、相続人は所得税が免除される死亡保険金を受け取ることができます。エージェントが言及し損ねていることが多いのは、あなたが亡くなったときに相続人が受け取るものはほぼすべて所得税がかからないということです。死亡時基準の引き上げのおかげで、家具、自動車、株、現金、投資信託、不動産など、退職金口座以外のものはすべて死亡日に再評価されます。基準が価値と同じになったため、キャピタルゲイン税はかかりません。退職口座、特に税金がすでに支払われている Roth 口座を継承するとさらに良い場合があります。 You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] 。 The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance.気分を悪くしないでください。 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

冗談ですか? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

<オル>It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . 。 .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

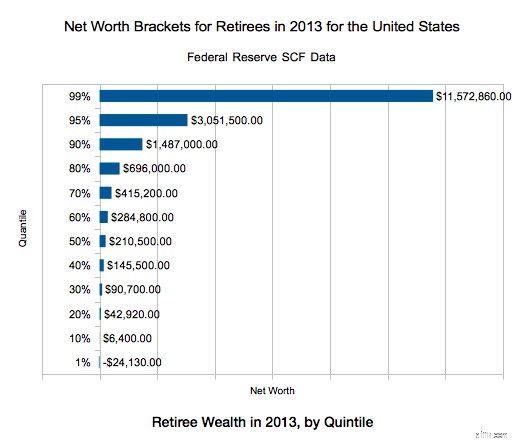

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

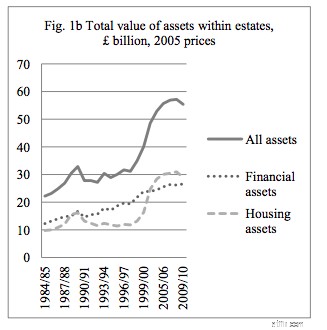

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

さあ、どうぞ。 Forty reasons for buying whole life insurance debunked.心配しないで; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

<オル>The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.

Have more questions about life insurance and what kind of policies would be best for you? Hire a WCI-vetted professional to help you sort it out.

Agree? Disagree? Please reference which “myth” you're referring to in your comment and keep comments civil and on topic. Ad hominem attacks will be deleted.

[This updated post was originally published as a series from 2013-2019.]

The White Coat Investor may receive compensation from White Coat Insurance Services, LLC; licensed in all states including MA and DC; CA license #6009217; NY license #1758759 (exp. 6/2027); Registered address:10610 S. Jordan Gateway, #200 South Jordan, UT 84095. This does not affect the cost or coverage of insurance.