借金をせずに学部教育を終えることは十分に可能だと思いますが、医師、歯科医師、弁護士、その他の高収入の専門家にとっては、その可能性はますます低くなりつつあります。この長い記事では、学生ローン免除プログラムから学生ローン借り換えに関するお得な情報まで、厄介な学生ローンの管理について知っておくべきことをすべてカバーします。この学生ローン 101 を検討してください。この投稿をトレーニングのレベルごとに分けているので、自分に当てはまる部分まで読み飛ばしていただければ幸いです。この投稿が、医学部の借金の重荷に苦しむ人々に希望をもたらしますように。

学生ローンは、教育費とそれに伴う生活費を支払うために学生に発行されるローンです。したがって、他の目的でそれらを取得または使用することは詐欺とみなされます。住宅ローンや自動車ローンとは異なり、これらのローンは差し押さえることができません。お金を払わないと誰も開頭手術を受けに来ません。ただし、その代わりに、かなり厄介な条件が 2 つあります。

<オル>学費に必要以上にお金を借りないでください。一部の金融援助機関は、生活費を賄うために追加のローンを組むことを推奨しています。生活費をまかなうために必要最小限の金額を持ち出すようにしましょう。ローンで贅沢な生活を送るために、必要以上に借金をしてしまう人もいるかもしれません。これは決して良い考えではありません。学生ローンをどうやって生きていくかについて詳しくは、「医学部での借金の正しい使い方」をご覧ください。

学生ローンに関して行う決定は、簡単に数万ドル、さらには数十万ドルの価値がある可能性があります。しかし、連邦返済プログラムが急速に変化するにつれ、その管理は年々複雑になってきています。この投稿を学習ツールおよびガイドとして使用することをお勧めしますが、独自の状況に応じた計画を立てるために、推奨される学生ローン アドバイザーのいずれかに相談することをお勧めします。彼らはこれらのプログラムを隅々まで熟知しており、最大限の費用を節約するための最新情報を提供しています。

連邦学生援助 (FASFA) の無料申請フォームに記入して、連邦学生ローンを申請します。あなたの結果によって、財政援助のオファーが決まります。

学生ローンを受け取る前に、入学カウンセリングを受けてローン返済の義務を理解し、ローン条件に同意する拘束力のある契約であるマスター約束手形に署名する必要があります。詳細については、学校の財政援助オフィスにお問い合わせください。

民間学生ローンの申し込みプロセスはさまざまですが、ほとんどの民間ローンの申し込みはウェブサイトからアクセスできます。

連邦学生ローンと民間学生ローンはどちらも通常、住宅ローンや自動車ローンなどの他の分割払いローンと同じように扱われます。毎回の支払いを期限内に行うと、信用履歴が構築され、信用スコアが向上する可能性もあります。支払いを滞納したり、学生ローンを滞納したりすると、信用スコアが打撃を受ける可能性があります。延滞や債務不履行に陥る前に、適切な収入主導型返済 (IDR) プランに加入していることを確認して、手頃な支払い額を確保してください。

多額の学生ローンを抱えて住宅の購入を考えている医師は、収入に対する負債の比率が高いため、住宅ローンを確保するのが難しいと感じるかもしれません。検討すべきオプションは、医師住宅ローン(医師住宅ローンとも呼ばれます)の利用です。医師住宅ローンは、学生ローンの負債対収入比率が高い高所得の借り手に特別な待遇を与える融資プログラムです。医師住宅ローンは、歯科医、獣医師、CRNA、PA、弁護士なども利用できることが多いです。

詳細についてはこちらをご覧ください:

医師住宅ローン

学生ローンは主に 2 つのタイプに分かれています。連邦ローンです。 (直接ローンとも呼ばれます) とプライベート ローン .

教育資金を借りる方法を決めるときは、私立よりも連邦で借りてください。連邦政府のローンは当初より低い金利を提供することができ、民間の学生ローンが提供していない連邦政府の保護が豊富にあります。民間ローンでは、収入に応じた返済、公共サービスローンの免除、IDR の免除は提供されていません。死亡または完全障害時に常に免除される連邦学生ローンとは異なり、民間学生ローンの免除ポリシーは標準化されておらず、貸し手によって異なります。

連邦融資は一般に金利が低く、特別な所得ベースの支払いプランや免除プランもあります。一般的なルールは、民間ローンを利用する前に、連邦融資プログラムで借りられる額を最大限に増やすことです。

ただし、外国の医学校の中には連邦融資の対象となるものとそうでないものがあります。外国の医学部に出願して入学する前に、必ずこのページのリストを参照してください。カリブ海の医学部は連邦融資の資格がないことで有名ですが、適合率が最も高い大学 (セント ジョージズ、サバ、アメリカン カリビアン大学、ロス) は資格を得る傾向があります。

連邦学生ローンは一本化することができます。このプロセスでは、多数のローンがすべて 1 つのローンにまとめられ、金利が平均化されて 1/8 ポイント単位に切り上げられます。これは、一般的に金利が引き下げられる借り換えプロセス (民間金融機関のみが利用可能) とは異なります。

資格要件は次のとおりです。

補助付きローンは、教育省が学部教育のために利子を支払うローンです。適格な借り手は経済的ニーズを示しており、在学中に未払い利息を支払う必要はありません。大学院および専門学位プログラムでは、補助金付きのローンは提供されなくなりました。補助金なしのローンは、受け取った瞬間から利息が発生し始めます。 PLUS ローン(卒業生または親)は補助金なしのローンです。補助金なしのローンを利用する前に、補助金付きのオプションをすべて使い尽くしてください。

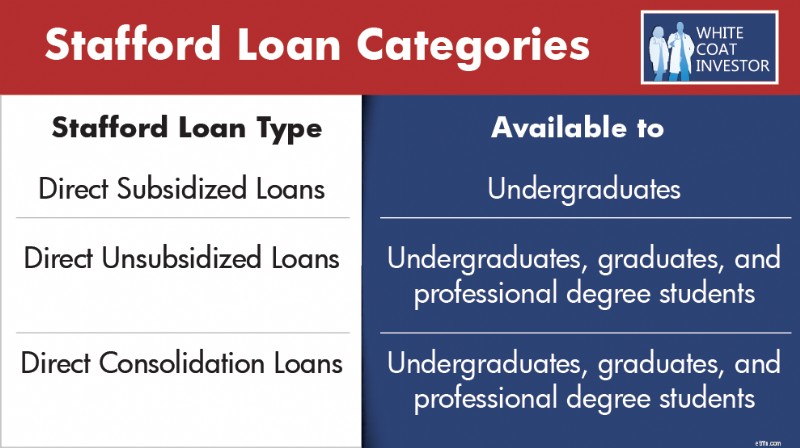

スタッフォード ローンは直接スタッフォード ローンとも呼ばれ、ウィリアム D. フォード連邦直接ローン (直接ローン) プログラムに由来します。直接スタッフォード ローンは最も一般的な学生ローンであり、現在、高等教育の費用をカバーするために発行されています。

スタッフォード ローンには 3 つのカテゴリがあります:

<オル>統合前のスタッフォード ローンは次の対象となります。

Grad PLUS ローンとしても知られる PLUS ローンは、ダイレクト ローン プログラムと FFEL ローン プログラムから提供されます。借り手は授業料をカバーするためにスタッフォードローンを使い果たした後、これらのローンが発行されます。 Grad PLUS ローンは廃止されます 2026 年 6 月 30 日以降にプログラムの借り入れを開始する人が対象です。

統合前は、Direct PLUS ローンは次の対象となります :

統合前の FFEL PLUS ローンは以下の対象となります :

統合後、FFEL PLUS ローンは次の対象となります。

親プラス ローンは、子供の教育資金を調達するために親に発行されます。これらは学部生、大学院生、専門学位の学生を対象に提供されています。以前は、Parent PLUS ローンの借入に制限はありませんでした。ただし、OBBBA は、子供 1 人あたり 65,000 ドル、年間最大 20,000 ドルという借入上限を設けました。

統合前は、Parent PLUS ローンは次の場合にのみ対象となります。

統合後、Parent PLUS ローンは次の対象となります。

OBBBA に従い、IDR プログラムの資格を維持するには、親の PLUS ローンを 2026 年 7 月 1 日より前に統合する必要があることに注意してください。つまり、IDR プランの資格を得たい場合は、今年できるだけ早く親の PLUS ローンを統合する必要があります。その日以降に統合または借入されたローンは、現在、IDR プランの対象外となります。所得条件付き返済 (ICR) プランは、これまで親借り手が利用できる唯一の IDR プランでした。以前は、借り手はより寛大な IDR プランにアクセスするために、複雑で面倒な二重統合プロセスをナビゲートする必要がよくありました。現在、親のPLUSローンが2026年7月1日より前に統合されている限り、ICRプランで1回の支払いを行った後、より寛大な所得ベース返済プランの対象となります。二重統合の抜け穴は、親の借り手にとってもはや問題ではありません。

2010 年以前は、家庭連邦教育ローン (FFEL) プログラムが連邦学生ローンの主な資金源でした。 プログラムは 2010 年に終了しました。 現在、すべてのローンは上記の直接ローン プログラムに基づいて発行されています。

統合前の FFEL ローンは次の対象となります。

統合後、FFEL ローンは次の対象となります。

連邦パーキンス学生ローン プログラムは、特定の経済的ニーズを持つ学生に大学への資金を提供するために創設されました。 プログラムは 2017 年 9 月 30 日に終了しました .

パーキンス ローンは、統合されるまで、所得主導型返済 (IDR) や公共サービスローン免除 (PSLF) などの多くの連邦プログラムの対象となりません。

統合後、パーキンス ローンは次の対象となります。

ほとんどの連邦学生ローンでは、実行時にローン手数料が発生します。料金は、在学中に受け取る各ローン支払いから比例して差し引かれます。つまり、実際に借りた金額よりも受け取れるお金が少なくなるということです。また、受け取った金額だけでなく、借りた金額全体を返済する責任があります。

以前は、民間の学生ローンは一般に、借り手が連邦ローンの上限に達した後にのみ利用され、Grad PLUS ローンが残りの資金ニーズのほとんどを満たしていました。 2026 年の秋以降に借り入れを開始する学生にとって、Grad PLUS ローンは選択肢から外れることになります。つまり、借り入れプロセスのかなり早い段階で民間ローンが利用される可能性が高くなります。連邦融資の資格がまったくない特定の国際医科大学に通う学生には例外が残されており、その場合は民間融資が唯一の選択肢となる可能性があります。

民間の学生ローンを利用する場合、連帯保証人は必要ありませんが、借り手がローンを確保し、より良い条件を得るのに役立ちます。連帯署名者の基準には次のようなものがあります。

一番最初から始めましょう。学生ローンはいくら借りるべきですか?真実を言えば、学部のために借金する必要はありませんし、借金すべき人はほとんどいないと思います。学部の学費には非常に幅があり、実際の教育の質の幅よりもはるかに広いです。いくつかの賢明な決断を下し、学部生として一生懸命勉強すれば、最終的に医師になる人のほとんどは、学部時代の借金をまったく負うことを避けることができます。独身生活を借金なしで終えるために実行できる、実行すべき手順は次のとおりです。

<オル>学位取得のために借金をすることになった場合は、補助金付きの借金のみを引き受けるようにしてください。そうすれば、医学部や研修医の間に興味が高まることはありません。医学部のためにローンを組む予定がある場合は、学部の 4 年生の終わり頃にその目的でローンを組むことを検討してください。金利が低くなるだけでなく (2025 ~ 2026 学年度では 6.39% 対 7.94%)、最初の 5,500 ドルも補助されます。

詳細についてはこちらをご覧ください:

借金をせずに学部を卒業しましょう!

医学部に入学する方法

最高の学生ローンは決して借りないものです。学費の負担を減らすためのテクニックはたくさんあります。

医学生および歯科学生向けの連邦学生ローンの借り入れが大幅に変更されました。 2025 年 7 月に One Big Beautiful Bill Act が署名されて以来、連邦政府の大学院生 PLUS プログラムは、2026 年 6 月 30 日以降に借り入れを開始する学生には廃止されます。ほぼ 20 年間、大学院生および専門学位の学生は、Grad PLUS ローンにより、出席費の全額まで、および標準的な直接補助なしの限度額を超えて借りることができました。現在、2026 年秋以降にプログラムを開始するユーザーには、そのオプションは存在しません。プログラムのその日付より前に借入を開始した場合は、古い借入ルールが適用されます。

大学院および専門教育(医学部/歯学部)に対する連邦政府の融資は、補助金のない直接融資に限定されます。補助金なしの借入は年間最大 50,000 ドルに制限されており、医学部または歯学部の場合は生涯で 200,000 ドルの制限があります。大学院の場合は年間2万500ドルが上限となり、生涯の上限は10万ドルとなる。すべての連邦借入 (学部/大学院/専門職) の生涯限度額は 257,500 ドルです。多くの学生は、連邦政府の上限が低く設定されているため、教育費を機関および民間の学生ローンで補うことを検討する必要があるでしょう。

詳細についてはこちらをご覧ください:

医学部の学費を支払うために軍隊に入るべきでしょうか?

医学博士課程および医学生向けの経済的なヒント

インターンとして純資産 0 ドルを達成

医学部を卒業したら、 学生ローンの管理を民間ローンの 2 つのカテゴリーに分けるのが最善です。 そして連邦融資 .

原則として、医師は民間の学生ローンを返済することになるため、発生する利息を最小限に抑えることが重要です。最善の方法は、医学部を卒業したらすぐに学生ローンを借り換えることです。金利を引き下げ、通常よりも低い支払い額 (月額 0 ~ 100 ドル) を享受できる「居住者プログラム」を提供する企業がいくつかあります。この支払いはローンに発生する利息をカバーするものではありませんが、金利が 6% ~ 10% から 3% ~ 6% に引き下げられるため、最終的に支払う利息は全体的に少なくなります。以下の WCI パートナーは、特別な居住者向け学生ローン借り換えプログラムを提供しています。

ローレル ロード $100/月のお支払い

SoFi 月額 100 ドルの支払い

スプラッシュ $100/月の支払い

民間の学生ローン貸し手は通常、居住中にローンを返済するための主な4つの方法を提供しています。一部のプログラムでは、在学中にさまざまな程度に支払いを延期できますが、利息はあなたまたはあなたの学校がローンから資金を受け取った日から発生することに注意してください。

入学後であっても、ローンの支払いからすぐに支払いが始まります。これは 4 つの支払いオプションの中で最も低いコストであり、初日から元金と利息の両方の支払いを開始できます。

この制度では、在学中は利息のみをお支払いいただきます。ローン残高は完済されませんが、 利息の支払いは続けられるので多額の借金はありません。 学業終了時のローン残高。

このオプションでは、学校に在籍している間、低額の固定支払いを支払う必要があります。居住終了時にはローン残高はさらに多くなりますが、総負債額は減少する方向に進むでしょう。

完全に延期することを選択した場合、卒業後の 6 か月の猶予期間を含め、在学中に必要な支払いを支払う必要はありません。これは 4 つの支払いオプションの中で最も高価です。

連邦学生ローンの借り手の多くは、ローン返済のための標準的な 10 年間の支払いプログラムに登録しており、10 年間で 120 回の固定支払いでローンを完済します。ローン額と金利に基づくこれらの月々の支払いは、6桁の借金を抱える典型的な低所得者が支払える金額よりもはるかに高い。ただし、収入主導型返済 (IDR) プログラムは、借り手に収入と家族構成に基づいて他の選択肢をローン返済できるようにする支払いプランです。

IDR プログラムは、文字通り学生ローンの標準的な支払いを支払う余裕がない居住者にとって非常に有益です。自由裁量収入の割合に基づいて支払いが行われる場合、月々の支払額は 0 ドルほどになる場合もありますが、100 ドルから 400 ドルの範囲になる可能性が高くなります。 IDR プランに準拠し続けるために、年に 1 回、収入を証明する必要があります (通常は納税申告書または給与明細を提出します)。

さらに、IDR プログラムは、公共サービスローン免除 (PSLF) や長期収入に基づく返済免除などの連邦ローン免除プログラムの対象となる返済プログラムです。

一部の IDR プランの主な欠点は、未払い利息をカバーできないことです。 200,000ドル、6%の学生ローンで毎月1,000ドルの利息が発生することを考えると、IDRの支払いでは通常、発生する利息をカバーするのにも遠く及ばず、滞在中にローンの額は増え続けることになります。後ほど、利子を補助する返済支援プラン (RAP) と呼ばれる IDR プランを導入する予定です。

IDR プログラムにより、連邦学生ローンの管理が非常に複雑になります。借り手にとって、未払い利息を最小限に抑え、最大限の免除レベルで最も手頃な支払いを見つけるために利用可能なオプションを理解することが重要です。連邦政府は収入主導型返済 (IDR) 計画を定期的に変更しており、最近では 2025 年 7 月に法律に署名された OBBBA を通じて変更されています。

どの IDR プログラムを利用する場合でも、収入がない場合でも医学部最後の年に納税申告書を提出する必要があることに注意してください。これにより、どの IDR プランでも、最初の 1 年間の支払いを非常に低額 (約 0 ドルから 10 ドル) で済ませることができます。

所得条件付き返済 (ICR) は、実際には従来のプログラムに近いものです。このプログラムに登録している医師に会ったことはほとんどありません。 ICR では、支払いはあなたの自由裁量収入の 20% です。 ICR が他のプログラムに比べて優れている点の 1 つは、統合後に Parent Plus ローンと併用できることです。親からのローンがない限り、ICR よりも優れた支払いオプションを提供する他の収入ベースの支払いプログラム (後述) が見つかる可能性があります。

ご注意ください , この支払いプログラムは、OBBBA により 2028 年の夏に廃止されます。その時点で、別の IDR プランを検討する必要があります。 ICR プランのみの利用資格がある親借り手の場合は、ICR プランで 1 回支払いを行い、その後、より有利な IBR プログラムに切り替えることができます。

資格 :部分的な経済的困難は必要なく、 ローンが最初に発行された日付も関係ありません。

検討すべき対象者 :親借入者

所得に基づく返済 (IBR) は、新しく改良された ICR です。主な機能は次のとおりです。

資格 :以前、IBR プランには部分的経済的困難と呼ばれる収入要件がありました。このルールは OBBBA の逝去により段階的に廃止されました。借り手は、 収入や負債に関わらず IBR に登録することができます。

旧 IBR は、2014 年 7 月 1 日より前に少なくとも 1 つの連邦学生ローンの未払いがある借り手に適用されます。

新しい IBR は、2014 年 7 月 1 日以降に連邦学生ローンを借り始めた借り手、またはその日以降に新たにローンを組む前に以前の連邦ローンをすべて返済した借り手に適用されます。

検討すべき対象者 :共働きの借り手とローン免除を受けようとしている人。ただし、旧 IBR の資格がある場合は、月々の支払額を抑えるために、以下で説明する PAYE プランまたは RAP プランを検討することをお勧めします。

Pay As You Earn は、新しく改良された IBR です。 PAYE の主な機能は次のとおりです。

ご注意ください , この支払いプログラムは、OBBBA により 2028 年の夏に廃止されます。その時点で、別の IDR プランを検討する必要があります。

資格 :部分的な経済的困難が必要です。したがって、出席者になる前に、PAYE に登録していることを確認してください。

To qualify for PAYE, you must have taken out your first federal loan after September 30, 2007, and received a loan disbursement after September 30, 2011.

FFEL loans are not eligible for PAYE unless they are consolidated through a direct federal consolidation loan.

Who Should Consider :Dual-income borrowers and those going for loan forgiveness.

Learn more about partial financial hardship

Learn more about interest capitalization

The Repayment Assistance Plan (RAP) was created by OBBBA in July 2025. The plan is supposed to be available July 1, 2026. Here's the main features:

Eligibility: Any borrower with direct federal student loans.

Who Should Consider :Borrowers with student debt that exceeds their income and/or those considering loan forgiveness.

The Saving on a Valuable Education (SAVE) program was introduced in the summer of 2023 replacing the old Revised Pay As You Earn (REPAYE) Program. The program ultimately ended in December 2025, following the resolution of a long-standing lawsuit brought by the state of Missouri. That litigation, which began in the summer of 2024, placed approximately seven million SAVE borrowers into a processing forbearance. Initially, the forbearance paused both payments and interest accrual through August 2025; once interest resumed, many borrowers began evaluating alternative repayment options for their federal student loans. Eventually all those still in SAVE will be forced to select another IDR plan or be automatically moved.

Partial Financial Hardship (PFH) is an eligibility requirement under the Pay As You Earn Repayment (PAYE) plan. In order to qualify, your monthly payment in PAYE must be lower than the standard 10-year repayment plan. If your payment in PAYE is above the standard 10-year payment, you do not qualify for a PFH,

However, if you’ve enrolled in PAYE while you qualified for a PFH you can continue in the plan even if your income grows and would make you ineligible thereafter. This is very common when income jumps as trainees become attendings.

Resident income = $60K

Student loan debt = $300K

Interest rate = 7%

Household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $60K – $23,940 =$36,060 × 10% =$3,606 / 12 =$301

The payment cap is $3,483 for this borrower. The monthly payment in PAYE is below the standard 10 year payment and eligible for a partial financial hardship.

Attending income = $450K

Student loan debt = $300K

Interest rate = 7%

household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $450K – $23,940 =$426,060 × 10% =$42,606 / 12 =$3,551

The monthly payment in PAYE has passed the standard 10 year payment due to the large increase in income as attending. Since the monthly payments are higher than the standard 10 year payment this borrower no longer qualifies for a partial financial hardship. They are no longer able to enroll into PAYE.

However, if the borrower enrolled in PAYE as a resident or before income has jumped, they are able to stay in the program as long as they don’t switch repayment plans.

Attending income = $441,900

Student loan debt = $300K

Interest rate = 7%

household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $441,900 – $23,940 =$417,960 × 10% =$41,796 / 12 =$3,483

The breakpoint is reached when your payment in PAYE equals the Standard 10 year payment.

Interest capitalization occurs when unpaid interest is added to the principal amount of your federal student loans. This increases the principal balance on the loan. The interest rate is now charged on that higher principal balance increasing the overall cost of the loan.

Principal balance = $200K

Accrued interest = $50K

Total balance = $250K

Interest rate = 7%

Annual interest charge = $200K × 7% =$14K

Principal Balance = $250K

Accrued Interest = $0

Total Balance = $250K

Interest Rate = 7%

Annual interest charge = $250K × 7% =$17.5K

After the accrued interest of $50K capitalizes the annual interest charge will increase by $3.5K

Interest capitalization can be inevitable, but should be avoided when possible. Here's when this happens:

In addition to the more well-known Public Service Loan Forgiveness (PSLF) program, several of the IDR programs have their own forgiveness programs. Remember none of these federal programs have anything to do with private or refinanced loans.

詳細についてはこちらをご覧ください:

How to Receive Student Loan Forgiveness

The IBR forgiveness program requires 20 to 25 years of payments, but you may make them while working for any employer or not working at all. New IBR is over 20 years and Old IBR is 25 years. There are two issues with this forgiveness program.

First, most physicians will have paid off their loans completely in less than 20/25 years because after they finish training, their payments will be equal to those under the standard 10-year repayment program. Perhaps that would not be the case for a very poorly paid physician with a very high student loan burden (3,4,5x their income), but for most, there just won't be anything left to forgive.

Second, the forgiveness is taxable, and after 20/25 years, the “tax bomb” could grow to as much or more than the original debt, at least on a nominal (non-inflation adjusted) basis.

PAYE offers forgiveness after just 20 years. However, it is still fully taxable at your ordinary income tax rate in the year you receive forgiveness. PAYE is being phased out in summer 2028, so if you are hitting forgiveness after that date you need to look at IBR or RAP as an alternative. And depending on when you started borrowing, you could end up with more years of payment and a higher monthly payment.

RAP has a generous interest subsidy but is the longest IDR forgiveness track at 30 years. RAP would likely have a lower loan balance leftover for the tax bomb versus PAYE and IBR, but is really only going to work out if you have massive loans as compared to your income. And, do you really want to carry your loans around until you reach your 60s?

Staying up to date on IDR forgiveness can be tough, especially since the timeline can span decades. Temporarily, there was a tracker on studentaid.gov, but the Department of Education took it down. Rather than relying on back of the envelope math, here's a hack that can show you an estimated payment count on your IDR plan.

<オル>Public Service Loan Forgiveness is the granddaddy of the federal forgiveness programs and the only one most doctors should be looking at. Not only does it offer tax-free forgiveness, but it also offers it after just 10 years of payments. If you make a bunch of tiny IBR, PAYE, or RAP payments during your training, you may only have to make 3-7 years of “full” payments as an attending before having the rest forgiven. There is a catch, however. You have to be directly employed full-time by a non-profit (501(c)(3)) while making all of those payments in an eligible payment program—or they don't count. You also have to make sure you can prove you made all of those payments since the federal student loan servicing companies have a nasty habit of not being able to count payments accurately.

詳細についてはこちらをご覧ください:

Public Service Loan Forgiveness

Dave Ramsey's Bad Advice About PSLF

Many residents are tempted to put their student loans into deferment or forbearance during residency and/or fellowship. This is almost always a mistake. Nothing makes me cry more than to run into a doctor who should only be 2-3 years away from receiving PSLF who had their loans in forbearance during a lengthy training period. I hate breaking the news to them that they've basically thrown away a benefit worth hundreds of thousands of after-tax dollars. It's like working for a year or two as a doctor without being paid at all. Deferment is slightly better than forbearance for some people, but they are both very similar for most high-income professionals with loans—you make no payments but the debt continues to grow, sometimes very quickly.

Deferments are granted in six-month increments by your loan servicer and subsidized loans don't accrue interest. Unsubsidized loans both accrue and capitalize interest. There are several reasons you can get a deferment, but the main one most residents would use is economic hardship, which is limited to just three years. Other reasons include active-duty military, unemployment, and going back to school.

With forbearance, interest accrues on both subsidized and unsubsidized loans. Just think of it as a 12-month pause on payments. For most medical students, it is no less attractive than deferment and it is easier to get. There are two types of forbearance.

<オル>I tell you about these two programs and give you these links because people wonder about them, not because I think people should actually use them. If you are seriously considering deferment or forbearance, you would almost surely be better off with an IDR plan. Not only would your payments count toward possible forgiveness down the road, but they may be as low as $0 a month anyway. In RAP, if your payments don't cover all the interest, all of that interest is forgiven by the government and is NOT added back on to the loan amount.

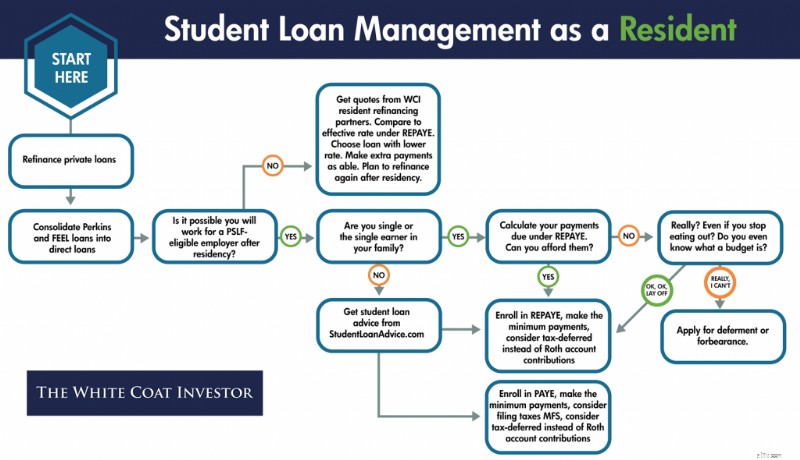

Let's summarize what to do with your student loans if you are a resident. The sooner you know if you are going for PSLF, the easier your decisions become. If you are single, or the sole earner in a married couple, it can also be very easy. But many people would benefit from getting formal advice from a specialist in student loan management. If you are married to another earner and one or both of you is going for PSLF, consider shelling out $400-$700 one-time fee as an intern to get advice. It could save you tens, or even hundreds of thousands of dollars. It is relatively easy for them to identify the red flags that indicate you're doing things wrong and they can help you run the numbers to make the difficult student loan management decisions that involve choosing an IDR program, choosing how to file your taxes, and even choosing whether to use a traditional or Roth IRA or 401(k).

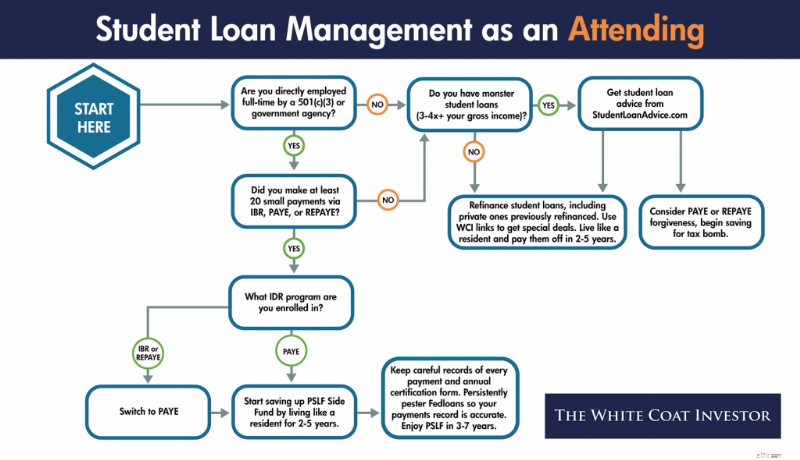

In contrast to residency, where student loan management can be very complicated, involving your taxes and even your retirement account contributions, management as an attending is generally very simple.

Your private loans, which you probably should have refinanced in residency, can be refinanced again and again as long as you can get a lower rate (and you usually can as a new attending). Obviously, refinancing doesn't actually make them go away, but it helps make more of your monthly payments go toward principal instead of interest. The way you make them go away is by living like a resident and dumping a huge sum on them every month. Even half a million in student loans doesn't last long against a five-figure monthly payment assault.

Regarding your direct federal loans, you need to finalize your decision of whether to go for PSLF or not. This is usually relatively easy. If you can answer BOTH of the following questions positively, you should go for PSLF:

If you cannot answer both of those questions positively, refinance your student loans and live like a resident for 2-5 years until they are gone.

詳細についてはこちらをご覧ください:

10 Reasons to Pay Off Your Student Loans Quickly

How Fast Can You Get Out of Debt?

The X Factor

What Does Live Like a Resident Really Mean?

Here are the best deals on student loan refinancing I've managed to negotiate with the top student loan refinancing lenders:

The secret to refinancing your student loans is to do it early and often. If you ask your fellow White Coat Investors for their regrets, many say they wish they had done it earlier because it was much easier than they thought. While it may appear intimidating at first, most of the companies will give you an accurate estimate of the rate you will eventually receive in 2 minutes online. You'll need to gather and submit some paperwork, but it's mostly all the same for all of the companies. So once you gather it and submit it to one, it is very easy to submit it to 2 or 3 more (or even all of them). Then just take the one that offers the lowest rate.

The rates offered to you will depend on your credit score, your debt-to-income ratio, and your desired loan terms. Unlike the federal government, which loaned you money just for getting into school, these private companies actually want to make a profit. They only want to loan money to people they think will be able to pay the money back.

The best way to get the lowest rate is to accept a 5-year term and a variable rate. If you are willing to live like a resident for 2-5 years after residency and pay off your loans quickly, these terms should be acceptable to you. While there is some legitimate fear of rising rates with a variable rate loan, the truth is that rates have to rise dramatically and/or early in the term in order for you to come out behind with a variable rate loan. If you can afford the worst-case scenario, I would at least consider a variable rate loan, and run the math under various interest rate scenarios.

Think of a fixed-rate loan as a variable rate loan plus an interest rate insurance policy. Since you should only buy insurance against financial catastrophes, someone planning to throw $10K a month at their loans every month for 2 years should not pay extra for a fixed rate. Just having a little more of your payment go to interest instead of principal for a few months is not a catastrophe. Even if rates rise early and dramatically, it will likely only delay paying the loan off by a month or two for someone truly committed to getting rid of them.

Some doctors fear refinancing because they are worried about what will happen to them if their income drops, if they die, or if they become disabled. This is a good reason to avoid putting a co-signer on your loans, but if you read the fine print you will see that most private companies have some accommodations for these situations. Often they will give you up to a year without payments in difficult situations (although the interest will continue to build). Loans are also often forgiven at death and sometimes even for disability. Be sure to read the fine print before signing on the bottom line so you know what to expect if any of these unlikely situations happen to you. Even if the company does NOT offer a death or disability plan, realize that purchasing enough term life insurance or disability insurance to cover the loans or its payments is likely cheaper than paying the extra interest in the government programs!

A lot of people get confused about loan consolidation, and in fact, use the term consolidating when they mean refinancing.

Consolidating generally means taking a bunch of loans and making one loan out of them. While that may increase the convenience of management, it does not actually reduce the interest rate. In fact, it may increase it. With federal loans, the weighted average of your loans is taken and rounded UP to the nearest 1/8th of a percentage point. You can consolidate your loans with the federal government, but to refinance them you must go to a private company and lose the benefits of federal loans such as the income-driven repayment programs and the forgiveness programs.

So why would anyone consolidate their loans if it increases your interest paid? Aside from the benefit of only having one loan to manage, the main reason is that you can turn some loans that were NOT eligible for IDR plans and PSLF into loans that are. The classic examples are Federal Family Education Loans (FFEL) and Perkins loans. By themselves, they are not eligible for those programs, but if consolidated into a direct loan, they become eligible. If you fall in this situation and want to use the IDR or PSLF programs, consolidate here.

Another reason to consolidate your loans is when you’re fresh out of med school and enrolling in IDR. Consolidation would allow you to opt-out of your grace period and begin making payments 3-4 months earlier. However, it can be a huge mistake for those who’ve been in training for a couple of years or attendings. Payment history is completely wiped out when you complete a direct federal consolidation—meaning those 3 years you’ve done to PSLF would be gone and you’d be starting over. I can’t tell you how many emails I’ve received from docs who’ve done this and were just a few years out from PSLF. Only to have the rug pulled out from them.

Things are a little more complicated for attendings who wish to go for Public Service Loan Forgiveness. These are generally academicians, or at least people who are willing to be academicians for a few years at the beginning of their careers. However, working for the military or the Veterans Administration or other government agencies can also count. There are also a few non-profits out there who directly employ their docs who should qualify for PSLF. Often these jobs pay less than a private practice job, so you need to take into account that sometimes you would be better off with a better paying job and paying off your loans, then going for forgiveness.

The big downside of going for PSLF is that you cannot refinance your loans. Only direct federal loans can be forgiven. So in the event that legislative or regulatory risk rears its ugly head, changing the program, or that you simply change your career goals such that you no longer qualify for it, you will end up paying more interest than you otherwise would have. But for those who stand to get tens of thousands forgiven, I think it is worth running those risks.

In order to maximize how much is forgiven under PSLF, you want to make as many tiny loan payments as possible. That means getting started as soon as possible, and that may be even earlier than you think. The more time you spend in training, the more you stand to have forgiven. If you spend 5 years in a surgery residency, then do a one-year burn fellowship and a one-year trauma fellowship, you may only make three years of “full” attending-size payments, leaving the vast majority of your debt to be forgiven, tax-free.

When going for PSLF, you must continue to make payments in an eligible program. For up to a year after leaving residency, those might still be relatively small payments, further increasing the amount eligible to be forgiven. But eventually, as an attending, you'll be making “real” four-figure payments toward your loans. At this point, IBR or PAYE might be the best program to be in because of the cap on the payments at the standard 10-year repayment program amount. That means if you were using RAP during residency and/or fellowship, you might want to switch to PAYE/IBR. Mortgage-sized student loan payments will start quickly as you juggle several competing financial priorities:

However, it is probably worth it. Of course, if you were in a situation in residency where you weren't going to qualify for a significant RAP subsidy anyway (usually due to a high-earning spouse), you should just use PAYE (or IBR if ineligible for PAYE) instead of RAP all the way through. But remember, under RAP, you could file under Married Filing Separately to avoid having to use the income of your high-earning spouse.

Another major complaint of those going for PSLF is that the student loan servicing companies such as MOHELA provide terrible service. Make sure you stay on top of everything. Not only do you need to be an expert at the requirements of the PSLF program (which of your loans qualify, which repayment programs have payments that qualify toward the 120 required monthly payments, and working full-time for a 501(c)(3)), but you must keep track of all the paperwork, including evidence of every single payment AND a copy of your annual certification forms. The certification is now done electronically (highly recommend over the paper form) and tracked through the studentaid.gov dashboard. Remember, you could end up going to court with the government in order to receive your promised forgiveness. Make sure you have the evidence you need.

In addition, you cannot just assume you will receive forgiveness. Not only could the program change and you not be grandfathered in, but your employment plans may simply change. Going for PSLF does NOT excuse you from living like a resident for 2-5 years out of residency. However, instead of sending those big 4-5 figure payments to your federal loan servicer, you need to send them to yourself. To your investment accounts, to be specific, creating a “PSLF Side Fund.” This way, even if PSLF doesn't happen for you, you're not behind the eight ball.

Hopefully by living like a resident you've been able to max out your retirement accounts AND save this side fund up in a taxable account, and you can simply liquidate the taxable account and use the proceeds to pay off the loans. But even if most of that savings ends up in retirement accounts and you can't (or don't want) to immediately eliminate the loans at that point, at least your net worth will be where it should be.

Let's summarize what to do with your student loans as an attending. Private loans should be refinanced whenever possible and paid off quickly by living like a resident. Federal loans should also be refinanced and paid off quickly unless you are directly employed by a 501(c)(3) AND made a lot of tiny payments during your training.

Remember that SAVE has been eliminated

If you die or are disabled, what happens with your private loans will be dictated by the terms on their promissory notes. Worst case scenario, if you die they are assessed against your estate. Your parents or siblings etc are never responsible for your loans, but your heirs could be indirectly.

In the event of death, your federal loans are discharged. With Parent Plus loans, the loans are discharged if the student OR the borrower dies.

In the event of permanent disability, federal loans are also forgiven. In a temporary disability, however, you may be limited to use of the IDR programs, deferment, or forbearance.

Student loans generally survive bankruptcy, meaning you cannot wipe them out simply by declaring bankruptcy. However, if you can prove undue hardship, you may be able to have them discharged. Defining undue hardship is going to be up to the judge, but I can assure you that if you qualify for it, you're going to be in a terrible place financially either way.

Depending on what happens to your loans at death and disability, consider carrying a little extra term life and disability insurance coverage to make up for it.

In the event of school closure you may be able to have your loans discharged. This tends to come up more in for-profit institutions, but it’s very rare.

In the event of the school falsely certifying your eligibility to receive a loan, you may be eligible for loan discharge. But this is very complex and unusual.

Some people with low-interest rate student loans wonder if they should really pay their loans off rather than invest. While it is intuitively attractive to borrow at a low rate and earn at a higher rate, this decision often ignores two factors.

The first is that most people simply don't invest the difference. Behaviorally, it is more difficult to maintain focus on building wealth once you have decided to make minimum payments and end up spending the money instead of investing.

The second is that an investment that provides a rate of return higher than the guaranteed return available by paying off your loans usually involves significant risk of loss. However, if you would like to carry your loans a little longer in order to invest inside retirement accounts, I think that's okay. But I would still plan to have them paid off within five years of finishing training. The financial muscles you develop paying off your loans quickly are the same ones you will use to build wealth toward financial independence afterward. I do not recall ever meeting a physician who regretted paying off their student loan quickly. In fact, most express a feeling of massive relief such as this email I received a few days ago from a two doctor couple who paid off over $700,000 in student loans in 16 months:

This student debt problem is so huge and overwhelming. I had many poor nights of sleep during training fretting about, “How do we pay off this 3/4 million dollar debt?” I feel now an immense stress has been lifted. We can now go forward and make some real decisions about how we want to live out the rest of our lives.

You can slay the student loan dragon. Sit down and get started today. Figure out where you stand; list out your loans by amount owed, payment, and interest rate and add up the total. Then start working on a plan to handle them. You can do it, the entire White Coat Investor Community is rooting for you!

詳細についてはこちらをご覧ください:

Pay Off Debt or Invest?

What's Your Investment-to-Debt Ratio?

Student loans and the many programs and options are challenging to navigate. If you need help, look to StudentLoanAdvice.com, a WCI company that helps the average client save $160,000 in loans! Check it out today!

どう思いますか? What other information belongs in the ultimate guide to managing physician student loans? Have you paid off your loans? What other advice do you have about them for your fellow White Coat Investors?