NPS is a retirement product. Specifically targeted to accumulate funds for retirement.

Here is how NPS can help you accumulate funds for retirement.

<オル>しかし、上記のすべて (およびそれ以上) を投資信託でも行うことができますよね?

<オル>NPS と投資信託はどちらも市場連動商品です。あなたの資金はプロの資金管理者によって管理され、リターンはファンドのパフォーマンスによって決まります。

In that case, which is a better vehicle to accumulate your retirement corpus? NPS か投資信託か

この投稿では、NPS と投資信託をさまざまな側面から比較し、これらの投資のさまざまなニュアンスを検討してみましょう。

メモ :NPS and mutual funds are NOT only investments for retirement. There are many others too and such investments can be part of your retirement portfolio too.ただし、この投稿では分析を NPS と投資信託に限定します。

Both are market linked investments.

No guarantee of returns.

NPS を使用すると、資金を株式ファンド (E)、国債 (G)、社債 (C) に分割できます。 アセット クラス A もあり、REIT、INVIT、AIF などの代替資産へのエクスポージャーが得られます。

さまざまな資産クラスまたはファンド (E、C、G A) への配分を決定するアクティブな選択を選択できます。 Maximum equity allocation can be 75%. Maximum allocation to A can be 5%.

または

You can opt for Auto-choice. Choose from 3 life cycle funds (Aggressive, Moderate, Conservative).ライフサイクルファンドでは、E、C、G ファンドへの配分がマトリックスに従って事前に定義されており、ポートフォリオ内のリスク (E へのエクスポージャー) は年齢とともに低下します。 Portfolio rebalancing also happens automatically in the auto-choice lifecycle funds.

投資信託には選択肢がありません。 You have several types of equity and debt funds.金、銀、さらには外国株式にも投資できます。 You can decide asset allocation and choose funds freely.

NPS is quite strict here. Expected too from a retirement product.

NPS では 60 歳になるまで辞めることはできません。 したがって、あなたのお金は事実上 60 歳まで固定されます。

注意事項 :60 歳になったら NPS を終了しなければならないという要件はありません。NPS の規則では、75 歳まで NPS からの終了を延期することができます。

At the time of exit, you can withdraw up to 60% of the accumulated corpus as lumpsum. You must utilize the remaining 40% to purchase an annuity plan.ただし、ご希望であれば、全額を年金プランの購入に利用することもできます。 0-60% lumpsum withdrawal. 40-100% annuity purchase.

Yes, you can exit NPS prematurely too once you complete 10 years. ただし、途中で退職する場合は、蓄積されたコーパスの 80% を年金プランの購入に使用する必要があります。 Only 20% can be taken out lumpsum. NPS also permits partial withdrawals in certain situations.

With mutual funds, there is no restriction on exit from any scheme. You can sell whenever you want. The only exception is ELSS where your investment is locked in for 3 years from the date of investment.

In case of NPS, annuity purchase will happen with pre-tax money.

You can purchase annuity plans using your MF proceeds too. However, please understand, in case of mutual funds, annuity purchase will happen with post-tax money. You will sell your mutual funds to buy an annuity plan and sale of MFs will result in capital gains liability.

Own Contribution to NPS account

If you are filing ITR under Old tax regime 、Tier-1 NPS への投資に対して、セクション 80CCD(1B) に基づいて会計年度あたり最大 50,000 ルピーの税制上の優遇措置が受けられます。 This tax benefit is available over and above tax benefit of Rs 1.5 lacs under Section 80C.

セクション 80CCD(1B) に基づく特典は、新しい税制では利用できません。

NPS アカウントへの雇用主の拠出

これは給与所得者のみが対象となります。そして、そこでさえ、すべての雇用主がこれを提供しているわけではありません。ただし、雇用主が NPS を提供している場合、雇用主が NPS アカウントへの寄付を申し出れば、大幅な税金を節約できます。

NPS、EPF、スーパーアニュエーション口座への雇用主の拠出金は、年間 7.5 ルピーまで税金が免除されます。 NPS の場合、この免税には追加の上限があります。この拠出額は基本給の 10% を超えてはなりません。州および中央政府の職員の場合、上限は 14% に増加します。

この投稿では、NPS に言及するときは常に、Tier-1 NPS を意味します。 NPS-Tier 2 もあり、条件付きで Tier-2 NPS への投資に対して税制優遇を受けることができます。ただし、Tier-2 NPS は純粋な退職後の製品ではないため、ここでは考慮しませんでした。さらに、 全国民モデルや企業NPS モデルについても言及しています。

投資信託の場合、投資に対する税制優遇はありません ELSSを除く。 ELSS への投資は、所得税法第 80C 条に基づく税制優遇の対象となります。

NPS :退出時に、一括出金 (蓄積されたコーパスの最大 60%) は所得税から免除されます。

残りの金額(40%)は年金プランの購入に使用する必要があります。年金プランの購入に使用されるこの金額には課税されませんが、年金プランからの支払いは収入に追加され、スラブ レートで課税されます。

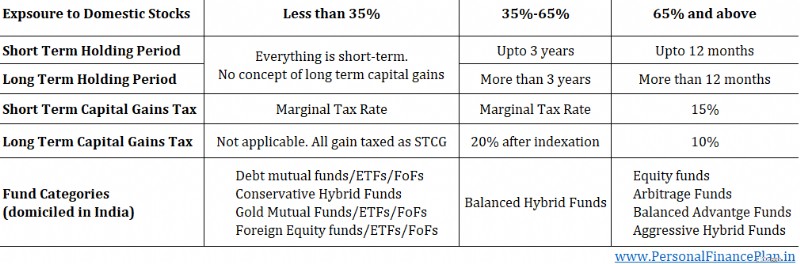

投資信託への課税は、投資信託の種類と基礎となる国内株式エクスポージャーによって異なります。

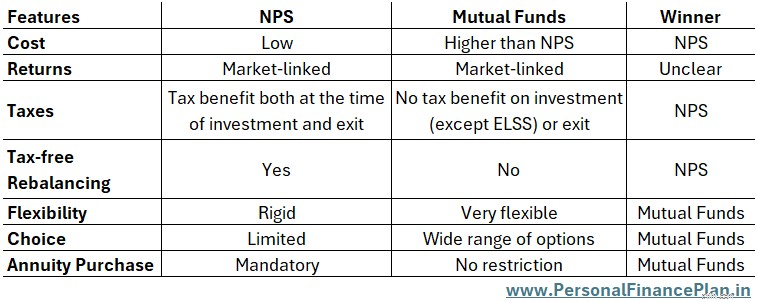

このコンテストではNPS が楽勝です。 NPS の最大のメリットは非課税リバランスです。

NPS では、税金が問題になるのは NPS からの退出時のみです。それ以前ではありません。したがって、税金の摩擦によって妨げられることなく、お金を増やすことができます。

異なる種類のファンド間で資金を切り替えたり、別の年金ファンドマネージャーに切り替えたりしても、キャピタルゲインは発生しません。したがって、キャピタルゲイン税はかかりません。

これにより、ポートフォリオのリバランスが非常に節税効果的になります。

したがって、あなたの NPS ポートフォリオが 50 ラックだとします。 アクティブ チョイス NPS .

E では 30 ラック、E と G では累計 20 ラック。

目標配分は株式:負債 50:50 ですが、株式市場の高騰により株式:負債 60:40 になりました。 E:C:G への配分を少し調整するだけで (たとえば 51:25:24)、ポートフォリオが目標レベル (それにかなり近い) にリバランスされます。 NPS でのリバランス中に税金を支払う必要はありません。

自動選択 NPS では、誕生日にリバランスが自動的に行われます。アクティブな選択では、 これを手動で行う必要があります。

過去 10 年間で投資信託への課税がますます不利になっていることを考慮すると、これは重要です。

2015 年 :デットファンドの長期保有期間が1年から3年に延長されました。それほど問題ではありません。

2018 年 :株式ファンドに導入される長期キャピタルゲイン税。会計年度内に 1 ラックルピーを超える株式/株式 MF を販売する LTCG には 10% の税金がかかります。

2023 年 :負債ファンドから長期キャピタルゲインを取り除いた概念。 2023 年 3 月 31 日以降に購入されたデット MF ユニットの場合、そのようなユニットの売却から生じるすべてのキャピタルゲインは短期利益とみなされ、所得税スラブ税率 (限界税率) で課税されます。これが最大の問題です。

Clearly, if you must rebalance a portfolio of mutual funds, there will be leakage in the form of taxes.これでは調合が妨げられます。 さらに、リバランスだけではありません。あまり好きではなくなった投資信託に投資したことがあるかもしれません。税金がなければ、もっと気に入った投資信託に乗り換えるだけです。ただし、税金のせいでこの作業全体が困難になります。

バランスの再調整については、場合によっては使用できる小さな回避策があります。 Instead of shuffling old investments, tweak the incremental allocation. たとえば、目標とする資本と負債の配分が 50:50 であるとします。最近の市場下落のため、資産配分は現在、株式:負債 45:55 となっています。資産配分が目標配分に戻るまで、すべての増分キャッシュフローを株式ファンドに振り向けることができます。何も売らないので税金の問題はありません。 個人的には、これだけのアプローチは少し面倒で実行が難しいと感じます。いずれにせよ、 このアプローチはより大きなポートフォリオには機能しません。

60 歳ではなく 55 歳で退職すると決めたらどうしますか?

NPS は厳格です。退職とは 60 歳以上を指します。

したがって、早期退職を選択し、退職金のほとんどが NPS にある場合は、問題が発生します。

55 歳で退職する場合は、蓄積されたコーパスの 80% を年金プランの購入に使用する必要があります。

仕事をやめたときに NPS アカウントを閉じる必要はないことに注意してください。退職後もアカウントを継続できます。したがって、55 歳で退職したとしても、60、70、または 75 歳までは NPS アカウントを継続し、寄付することもできます。

投資信託を使えばこの問題に直面することはありません。いつでも好きなときにお金を引き出すことができます。引き出しには年齢は関係ないのです。

余談ですが、NPS は柔軟性の点で MF に劣るかもしれませんが、他の年金商品よりもはるかに優れています。

私はNPSとインドの生命保険会社の年金商品を比較しています。生命保険会社は、リンク型と非リンク型の両方の年金商品を発売しています。

NPS では、投資が体系的である必要はありません。多額の一括投資も可能です。制限はありません。他の年金商品では、毎年一定額の保険料を納める必要があります。補充するのは簡単ではありません。

Proceeds from ULIPs (with annual premium> 2.5 lacs) and Traditional plans (with annual premium> 5 lacs) are now taxable. NPS ではそのような問題は発生しません。

In NPS, you can withdraw 60% of accumulated corpus tax-free.保険会社の年金制度では、累積コーパスの 1/3 のみを非課税で引き出すことができます。

NPS で投資できる株式ファンドは 1 つだけです。 C ファンドやG ファンドも同様です。

株式 (E)、国債 (G)、社債 (C) は異なる年金基金マネージャーからのものであっても、NPS ポートフォリオには株式ファンドが 1 つしかありません。 1 つのアクティブ運用株式ファンド。 I would expect these equity funds from NPS to have a large-cap tilt.

各年金基金管理者 (PFM) は、1 つの E、1 G、および 1 C のファンドを提供しています。投資できるファンドはE、G、Cのいずれか1つのみです。同じまたは異なる PFM から。 2つの株式ファンドに投資することはできません。 Or equity funds from 2 pension fund managers.

Mutual funds offer a much wider variety of choices.大型株、中型株、小型株のファンドがあります。アクティブにもパッシブにも。 Flexicap, Factor, Sectoral, Thematic.外国資本。名前を付ければ、それが手に入ります。

When it comes to investments, less choice is not necessarily bad. However, most investors would not want to keep all their equity money in a single actively managed fund, as is the case in NPS.

リターンを比較したくありません。 Simply because NPS funds have much lesser restrictions on where they can invest. What should be the true benchmark for an NPS Equity fund?ニフティ50、ニフティ100、ニフティ500? Which equity mutual funds should I compare the performance with?

You can check the returns of various NPS schemes here.

NPS は最も低コストの投資商品です。 The Investment management fee is less than 10 bps.

投資信託の支出ははるかに高くなります。複数の要因に依存します。通常または直接。 Equity or Debt. Active or Passive.

With an annuity plan, you pay a lump sum to the insurance company.また、保険会社は生涯にわたる収入源を保証します。

Mandatory annuity purchase has been highlighted a major problem of NPS.

However, I do not see mandatory annuity purchase as a problem. Any good retirement product should have the facility to divert an allocation towards annuity purchase. However, you must buy the right variant at the right age.

Yes, if you are smart with money, you can manage without an annuity plan. However, most investors would struggle to generate regular cashflows during retirement from a market linked portfolio. If payouts from an annuity plan can cover a portion of your expenses, I do not see much problem there.

Even if you are smart, you must consider following points.

<オル>A quick comparison on all the aspects we discussed above.

<オル>メモ :In case of NPS, annuity purchase will happen with pre-tax money. In case of mutual funds, annuity purchase will happen with post-tax money.

So, which is a better investment vehicle for retirement savings? MFs or NPS?

ここで客観的な勝者がいるとは思えません。 NPS fares better on cost, taxes, and a critical area of portfolio management, portfolio rebalancing. MF is an outright winner in flexibility and choice of funds. Hence, the answer depends on your requirements and preferences.

Moreover, it is not an either-or decision.両方使うことも可能です。

When you are planning for retirement, you do not have to keep all your retirement money in a single vehicle. You can use multiple vehicles for the same goal.

Hence, you can invest in both mutual funds and NPS for your retirement.

If the rigid exit rules or the lack of choice of funds in NPS worries you, you can invest more in mutual funds.

If tax-free rebalancing is a high priority, you can allocate a sizeable amount in NPS.

Yes, you can have other products too in your portfolio such as EPF, PPF, Gold, bonds etc). For this post, I am limiting discussion to MFs and NPS.

An example of how you can benefit from tax-free rebalancing feature of NPS.

Let us say, for your retirement portfolio, you have Rs 40 lacs in NPS and Rs 40 lacs in mutual funds.

NPS :E:24 ラック、G:8 ラック、C:8 ラック

Mutual funds:Equity Funds:28 lacs, debt funds:12 lacs

Total equity allocation =24 + 28 =Rs 52 lacs, which is 65% allocation to equities.

But you wanted 60:40.

If you sell equity funds and buy debt funds, you will have to pay tax.

一方、NPS-Equity (E) ファンドから 4 ラックルピーを G および C ファンドに移すことができれば、税金を支払うことなく 60:40 の目標配分に戻すことができます。 And you can do that by simply changing asset allocation in NPS to 50:25:25 (E:G:C).

Personally, I prefer to have the bulk of the money in mutual funds. Greater choice of funds.パッシブ投資の利用可能性。 Better disclosures than NPS funds.より重点を置いた規制当局 (SEBI 対 PFRDA)。 At the same time, having a decent allocation to NPS would not harm because of the tax-free rebalancing feature. In fact, the allocation to NPS can come in handy since you can purchase an annuity plan from pre-tax money after you retire.

What do YOU prefer for your retirement savings:NPS or Mutual funds?

Image Credit :アンスプラッシュ

免責条項:SEBI によって付与された登録、BASL のメンバーシップ、および NISM からの認定は、仲介業者のパフォーマンスを保証したり、投資家への利益を保証したりするものではありません。証券市場への投資には市場リスクが伴います。 Read all the related documents carefully before investing.

この投稿は教育のみを目的としており、投資アドバイスではありません。これは、特定の製品に投資する、または投資しないことを推奨するものではありません。引用されている証券、商品、または指数は説明のみを目的としており、推奨するものではありません。私の見解は偏っている可能性があり、あなたが重要だと考える側面には焦点を当てないことを選択するかもしれません。あなたの経済的な目標は異なるかもしれません。異なるリスク プロファイルがある可能性があります。あなたは私とは異なるライフステージにいるかもしれません。したがって、私の文章に基づいて投資を決定しないでください。 投資に万能の解決策はありません。特定の投資家にとって良い投資であっても、他の投資家にとっては良い投資ではない可能性があります。そしてその逆も同様です。 したがって、 投資する前に商品の利用規約を読んで理解し、リスクプロファイル、要件、適合性を検討してください。 あらゆる投資商品において または投資アプローチに従ってください。