あなたがまだこれに気付いていないのなら、私は一種の目標設定フリークです。

一部の人々は新年の決議をします。それは素晴らしいことですが、より一貫した基準で目標を再検討する必要があると思います。私にとって、それは90日ごとです。

他の人はわざわざ目標を設定しません。彼らは、少なくとも無意識のうちに、運に頼ることを選びます。

目標は夢や願いよりも実質的なものであることを前もって確立しましょう。

彼らは夢や願いとして始めることができますが、彼らの背後には、欲望を現実のものに変換する方法を説明する行動計画があります。

これは、財務目標に関しては特に重要です。それらは長期間にわたって定期的なお金と労力の投資を必要とするため、それらを実現するための実行可能な計画を立てる必要があります。

いくつかの財務目標を設定することから始めます。これについてあまり考えたことがない場合は、ここに10の優れた財務目標があります 2022年には誰もが優先すべきだと。

私たちは通常、緊急資金を持つことを短期的な財政目標と考えています。そして、機械的な観点からは、それは真実です。ただし、緊急資金には長期的に重要なメリットがあります。そのため、緊急資金は、達成を計画する必要のある優れた財務目標の1つです。

豊富な緊急資金があなたの人生を通してあなたに提供できる利点のほんの一部がここにあります:

強力な緊急資金を持っていることから来るすべてを考えるとき、それはそれを優先順位のはしごを数段上に移動する必要があります。緊急資金の普通預金口座の主なオプションは次のとおりです。

お金による広告。このad.Adをクリックすると、報酬が支払われる場合があります。 ハイイールド普通預金口座付き。あなたはそれを稼ぎながらお金を節約することができます。スマートで効果的な貯蓄のために、高利回り普通預金口座は実行可能なオプションです。以下の州をクリックして、今すぐアカウントを開設してください。 Open an Account Today

ハイイールド普通預金口座付き。あなたはそれを稼ぎながらお金を節約することができます。スマートで効果的な貯蓄のために、高利回り普通預金口座は実行可能なオプションです。以下の州をクリックして、今すぐアカウントを開設してください。 Open an Account Today The great thing about this goal is that anyone can do it, regardless of income or wealth level. And if you want to get the most out of your finances, it’s virtually a requirement that you get out of debt.

For the moment, let’s ignore the good-debt-versus-bad-debt debate. At some point in your life, all debt is bad debt and needs to be paid off. That includes the mortgage on your home. Although the purpose of that debt may be noble at the beginning, it’s no less a drag on your income than any other debt as time goes on.

There are more reasons to get out of debt than I can list here, but here are just a few of them:

Before starting my career, I fell into the debt trap. I had accumulated over $20,000 of student loan and credit card debt and I wasn’t slowing down anytime soon.

Thankfully, my girlfriend (now wife) helped me to see debt for what is really is – EVIL.

After we were married, it became both of our goals to become debt free and never carry a credit card balance. I’m proud to say that after over 10 years of marriage, that’s a goal that we’ve stuck to.

Take that, Debt!

You can set all of the good financial goals that you want, but it will be difficult to achieve any of if you are carrying a significant amount of debt for the rest of your life.

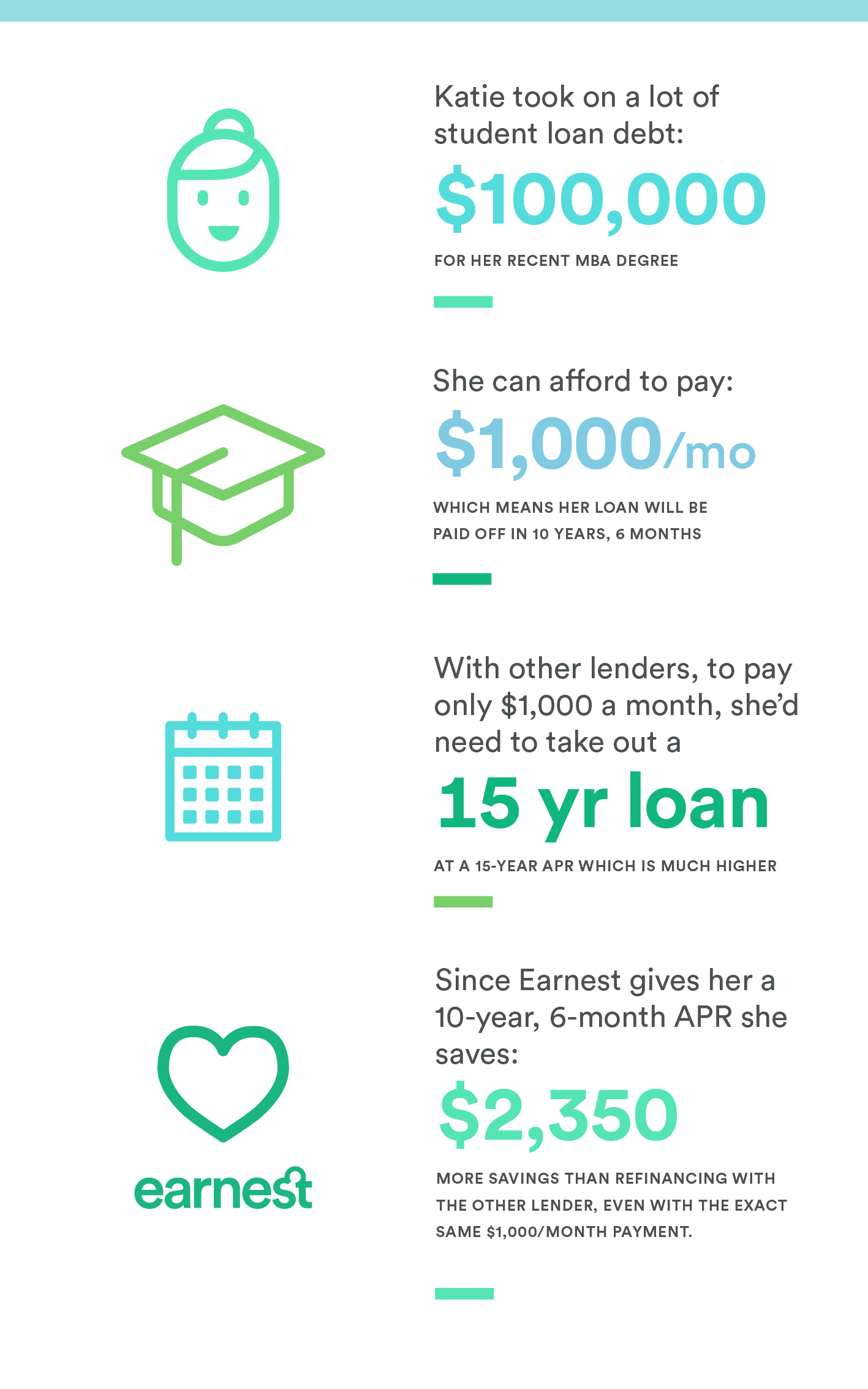

If you have high interest credit card debt or several different credit card bills to pay every month, it can make a lot of sense to take advantage of a 0% APR balance transfer offer as well.

The Chase Slate ® card, for example, gives you a 0% APR for a full 15 months, and all without a balance transfer fee of any kind. With this offer, you could transfer several high interest debts and save hundreds – or even thousands of dollars – over the introductory APR period.

When I started as a financial advisor and finally grasped the concept of compound interest, I was determined to put myself in situation where I could retire by the age of 50 if I wanted to. I don’t know if I’ll ever really retire, because I absolutely love what I do.

Even if you absolutely love what it is you do for a living, planning for early retirement is one of those top-rated good financial goals.

A recent survey from Provision Living suggests that 43% of millennials have $5,000 or less stowed away for retirement. The survey also revealed that most millennials are concerned about their retirement and doubt they will have enough to live on.

Here’s why planning for retirement is crucial:

There’s one other advantage to planning to retire early, and it’s a big one. By working toward early retirement, you will be front-loading your retirement investment portfolio. That will give you a larger portfolio early, which will mean that you won’t have to work so hard saving for retirement later in life when doing so may be more complicated.

For me, that was opening a Roth IRA and maxing it out. My wife, too. In addition, I was putting as much money into my 401k that I could.私を信じて。 As a brand new financial advisor, I wasn’t making much but I still manage to prioritize my spending and save a significant amount.

Early in my career I had witnessed too many couples in their 60’s that hadn’t save enough to retire at all, yet retire early. I made it a goal (and a mission) that I wouldn’t let that happen to me.

Even if you love your job, creating multiple income streams is a form of income insurance 。 For that reason alone, it needs to be on your list of good financial goals.

But here are even more reasons:

Reading Rich Dad, Poor Dad was a defining moment for me. Before then I was oblivious to the concept of having multiple streams of income. Over the years, I dabbled in many side hustles looking for “it”. That included a few multi-level marketing companies that proved to be a flop.

I eventually took a stab at real estate and also failed miserably. Many would perceive these as failures, but I view them more as valuable life lessons that eventually led me to start this blog. Now I have more than a few sites that yield over 6 figures per year. Not too shabby for a guy that had no web marketing experience before I started.

Give this goal some serious thought, even if you’ve never considered it before. It’s a goal that could open the door to a lot of other goals.

Insurance is something of a tough call. A lot of people don’t have nearly enough coverage, while many others are paying too much for the coverage that they have. Striking a balance between the two is another of those good financial goals.

Here are some strategies in striking that balance:

Part of your goal should be to work with a knowledgeable insurance agent on a regular basis to make sure that you have just enough – but never too much – insurance coverage. Oh by the way, did I mention that I’m also a co-founder of an independent insurance agency?

I’ve covered this topic in other articles, but it is well worth repeating here since it is one of the most necessary of all good financial goals. By learning to live on less than you earn – no matter what – you will always have plenty of income. That means that you’ll have plenty of income for savings, investments, and for paying off debt.

It’s important to always be on the hunt to increase your income. But that strategy will only be effective to the degree that you are able to live on less than you earn so that you can put the difference to better use to improve your life.

This may not be a financial goal in and of itself, but it is an obstacle that will stand in the way of all good financial goals, no matter what they are.

An addiction to stuff can be like a financial parasite. A disproportionate amount of your income and financial reserves will go to pay for your need for stuff.

This will present several problems:

I love this quote from Joshua Becker, author of Simplify:7 Guiding Principles to Help Anyone Declutter Their Home and Life ,

“Removing possessions begins to turn back our desire for more as we find freedom, happiness, and abundance in owning less. And removing ourselves from the all-consuming desire to own more creates an opportunity for significant life change to take place.”

If you even suspect that you may have an addiction to stuff, then make it a financial goal to end that addiction once and for all. Your life will go better if you do.

Ultimately, the purpose of improving your finances should be to provide you with independence in your life. That means that it should afford you the ability to do what you want when you want. If that isn’t one of the good financial goals, then I don’t know what is.

A recent Gallup Poll suggests that engagement at work, defined as enthusiastic involvement and commitment at work, is at an all-time national high at 34%. While that number may be higher than in the past, it still only constitutes 1/3 of American workers. That means quite a percentage of the population is indifferent, or in some cases, downright miserable, when it comes to their job.

Getting out of debt, preparing for early retirement, developing multiple income streams, and ending your addiction to stuff, should clear the way for you to be able to do the kind of work that you really love. That should be true even if the work doesn’t pay nearly as much as you’re being paid now.

But that will be possible only if you have no debts to pay, if you can live on less than you earn, and if you have a large investment portfolio to back you up.

Why is doing work that you love a worthy financial goal? Very few people will actually be retiring to the beach for a life of blissful nothing, no matter what you see on TV. If nothing else, it’s likely that you will work just as a matter of personal satisfaction – or an attempt to avoid boredom.

Since you will be working all of your life – one way or another – the work that you do shouldn’t just be about earning money. It should be something that makes you feel good about your life and good about the person you are.

If you can’t get comfortable sharing your good fortune with people who are less fortunate – perhaps out of fear that you will end up broke as a result – then money has complete control over your life. It doesn’t matter how much money you amass in your life, it should never control you.

There are numerous reasons why giving to others will be good for you:

Is giving one of those good financial goals? I think that if you look at many of the most famous wealthy people in the world, you will see a distinct pattern of giving to others along the way.

However you live your life, it should be a goal to make sure that your loved ones are left at least a little bit better off as a result of your life. That means not only making adequate provisions for those who are dependent upon your financial resources but also making sure that you don’t leave them with a financial mess to clean up.

Here are some steps you can take to leave your financial house in order upon your death:

Reaching a point of financial independence in life has nothing to do with luck or magic. It’s simply a matter of setting good financial goals and having a concrete plan as to how you will achieve them. Once that plan is established, and working toward those goals becomes part of the habits that make your life what it is, achieving financial independence can almost seem as if it’s happening on automatic pilot.

But only if you make it happen.

When’s the last time you wrote down your goals? More importantly, when’s the last time you’ve revisited them?