成長して、私の両親は私にお金を節約することの重要性を教えてくれました。お金を貯めれば、大人になるまでには十分だという考えでした。

悲しいかな、私が年をとったとき、私はインフレの現実にさらされました。 0.5%p.aを見てください。私の銀行口座の金利も役に立ちませんでした。 (銀行でより多くのお金を節約している場合は、より高い金利を利用できる可能性がありますが、ほとんどの銀行は最大4%を支払います。)

しかし、状況は変わりました。暗号通貨とDeFiの出現により、私たちは今、より高い年間収益を約束する暗号通貨普通預金口座にアクセスできるようになりました— 19.5%にもなる!

次のセクションでは、検討できる最高の暗号貯蓄口座について説明します。この記事では、ステーキングやその他の形式のDeFi歩留まり生成プロトコルについては触れないことに注意してください。

目次ただし、最初に、概要を示す比較表を次に示します。

(さらに右にスワイプまたはスクロールし、ヘッダーをクリックして並べ替えます。)

| Ethereum APY | USDT APY | DAI APY | USDC APY | UST APY | ||||

|---|---|---|---|---|---|---|---|---|

| 7.46% | 7.46% | 12.73% | 8.32% | 12.73% | - | いいえ、ただしNexus保険に申し込むことはできます | はい、コインによって異なります | |

| 7% | 7% | 12% | 12% | 12% | - | はい、コインによって異なります | はい、0.02% | |

| 6.25% | - | - | - | 9.50% | - | はい、管理人のBitGo経由 | はい、コインによって異なります 1日あたりの引き出し限度額があります | |

| YouHodler | 4.80% | 5.50% | 12.30% | 12.00% | 12.00% | - | はい、100米ドル相当 | |

| 6.20% | 5.35% | 10% | 10% | 10% | - | はい、管理者のFireblockを介して | ||

| CakeDeFi | 3.5%+潜在的なボーナス2.5% | 3.5%+潜在的なボーナス2.5% | 7% | - | 7% | - | はい、コインによって異なります | 4週間の保有期間、貸付はバッチで実行されます |

| 4.50% | 5.00% | 9.50% | 9% | 9% | - | 最小保留期間はありませんが、引き出しの処理には1日かかります | ||

| aax | 4.00% | 4.00% | 6.35% | 2.50% | 6.50% | - | はい、コインによって異なります | はい、コインによって異なります |

| 1.49% | 2.05% | - | 7.99% | - | 7.99% | |||

| Crypto.com | 1.50% | 3.50% | 6% | 6% | 6% | - | はい、コインによって異なります | |

| 4.00% | 4.00% | 8.00% | 8.00% | 8.00% | - | |||

| Yearn.Finance(dApp) | - | 1.63% | 4.27% | 4.80% | - | - | いいえ、ただしセキュリティプロトコルを実行します | いいえ。ただし、20%の成功報酬と2%の管理報酬があります |

| - | - | - | - | - | 19.50% | いいえ、ただしNexus保険に申し込むことはできます | 1 | はい、引き出し金額によって異なります |

| - | - | 5% | $ 200 |

P.S.暗号通貨を初めて使用する場合は、次のライブマスタークラスに参加して基本を理解してください。

暗号通貨の普通預金口座は、従来の銀行口座のように機能します。アカウントにお金を預け入れ、利息を受け取り、お金の流動性を享受します。

従来の普通預金口座と暗号化普通預金口座

| 従来の普通預金口座 | 暗号普通預金口座 | |

|---|---|---|

| デポジット | フィアット | 暗号 |

| 歩留まり | 0.5 – 4% | 1 – 13% |

| 流動性 | 高 | 高 |

| 市場リスク | 下 | 高い(ボラティリティが高いと仮定) |

| 規制 | 政府は通常銀行を規制しています | すべての暗号普通預金口座が規制されているわけではありません |

| 保険: | シンガポールでは、各銀行の最大75,000ドルの預金が預金保険制度によって保護されています | すべての暗号貯蓄プラットフォームが預金を保証するわけではありません |

では、なぜ銀行はあなたに利子を支払うのですか?

ええと、通常、銀行はあなたの「貯められた」お金を貸します。あなたのお金を使うことと引き換えに、彼らはあなたと利益のごく一部を共有します。暗号普通預金口座も同じように機能します。したがって、それらは暗号貸付口座と呼ばれることもあります。

これを書いている時点で、Hodlnautはビットコインで最高の貯蓄率を提供しています。あなたがビットコインを購入してhodlすることを計画しているなら、それはあなたが価格の上昇とボラティリティに乗っている間あなたがあなたのビットコインを成長させることを可能にするかもしれません。 Hodlnautの最新の金利はここで確認できます。

Hodlnautは、ホドラーが暗号通貨を最大限に活用できるようにするために作成されたシンガポールベースのプラットフォームです。

彼らはシンガポールと香港に事務所を持っており、MASによる決済サービス法の免除を受けています。これは、MASが暗号会社を規制する方法を理解している間、彼らはライセンスを保持することを免除されることを意味します。

簡単に言えば、これは、Binance.comが最近行われたようにそれらが禁止されることを心配する必要がないことを意味します。

提供される暗号通貨

Hodlnautは、ビットコイン、イーサリアム、ダイ、USDC、USDT、WBTCの6つの暗号通貨でのみ利回りを提供します。

保持期間なし

保有期間はなく、利息は毎週支払われます。したがって、見栄えの良いNFTを購入するためにコインを引き出す必要がある場合は、いつでもそうすることができます。

法定通貨を使用して資金を調達したり、暗号通貨を直接購入したりすることはできません

Hodlnautは取引所ではないため、直接コインを購入することはできません。これは、暗号通貨取引所から手動でコインを入金する必要があることを意味します。

Gemini(無料の引き出しが付属)のような取引所を使用してコインを購入し、Hodlnautに転送することができます。

引き出し手数料+直接法定紙幣の引き出しはありません

Hodlnautはコインに基づいて引き出し手数料を請求することに注意してください:

執筆時点では、S $ 100は約0.0012BTCです。 0.0012BTCを引き出すとすると、取引コストは33%になります。

そうは言っても、月に1回無料で引き出すことができます 、これはホドラーには十分なはずです。

保有物をすぐに法定紙幣に引き出すこともできません。代わりに、持ち株を取引所に引き出し、そこから現金化する必要があります。

保険はオプションです

Hodlnautは、クライアントの暗号通貨に直接保険をかけることはありません。ただし、Hodlnautがハッキングされた場合や、90日以上引き出しを停止した場合に備えて、資金を保護するためにNexus保険を購入することを選択できます。

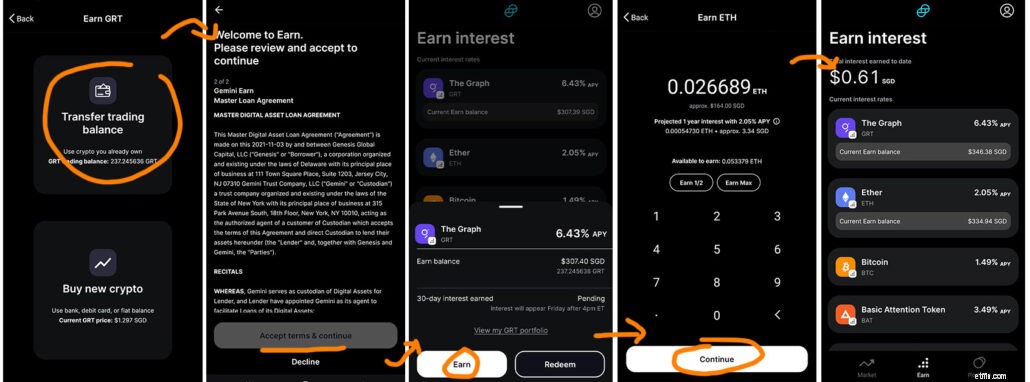

簡単に始められます:2つのステップでより高い関心を解き放ちます

私の意見では、Hodlnautの主な魅力は、たった2つのステップでより高い関心を獲得し始めることができるということです。

転送が成功すると、利息が発生し始めます。また、毎月1回の無料引き出しにより、暗号通貨を任意の取引所に送信し、そこから現金化することができます。利回りを稼ぎ始める簡単な方法。

Hodlnautによると、KYCプロセスには3〜5営業日かかるとのことです。しかし、私の経験では、約7営業日かかったので、辛抱強く待つ必要があるかもしれません。

ここでHodlnautアカウントにサインアップできます(紹介リンク)。

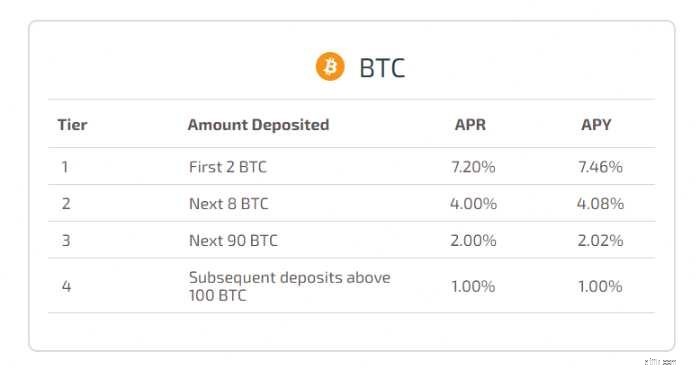

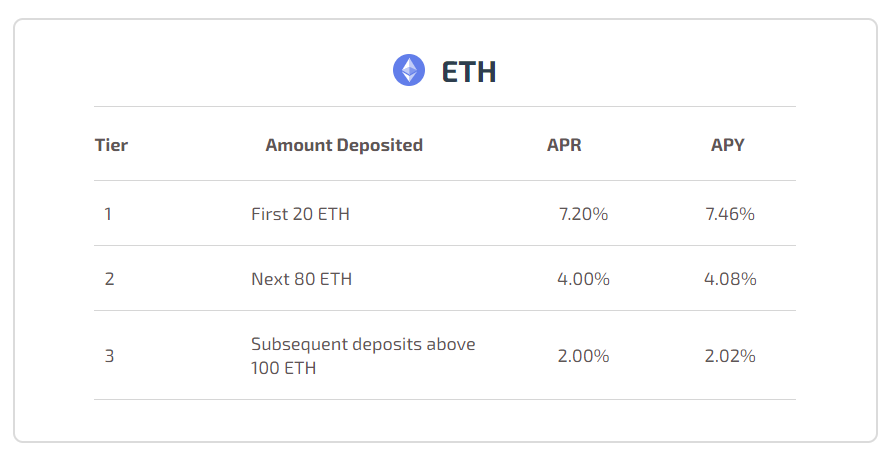

イーサリアムの最高の利回りを持つ暗号普通預金口座もHodlnautであり、イーサリアムで最大7.46%のAPYを提供します。

Youhodlerは、ユーザーが最大90%のローン対価値比率を借りることができるもう1つの暗号通貨貸付プラットフォームです。

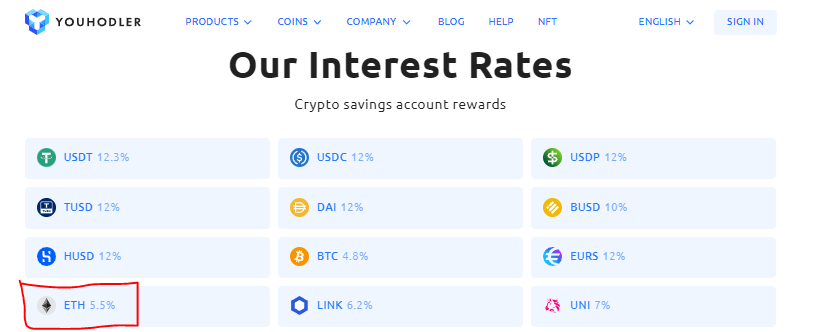

執筆時点で、USDTで最大12.3%のAPYを提供しています。ここで彼らの最新の金利をチェックすることができます。

提供される暗号通貨

Youhodlerの39の暗号通貨で利息を稼ぐことができます。

SGDを直接受け入れません

YouHodlerはシンガポールドルを受け入れません。

Youhodlerプラットフォーム内で暗号通貨を購入するには、銀行振込を行うことができます。この時点では、USD、EUR、GPB、およびCHFのみを受け入れます。料金がかかる場合があります。

APYがあなたを魅了する場合、それを転送する前にGeminiから暗号通貨を購入する方が簡単(そしておそらく安価)であることがわかるかもしれません。

手数料の引き出し

同様に、銀行振込を使用して、保有物を法定紙幣に引き出すことができます。または、暗号を別のウォレットまたは取引所に転送することもできます。料金はコインごとに異なり、公に共有されることはありません。

資金はLedgerVaultで保険がかけられています

YouHodlerは、LedgerVaultによる最大1億5,000万ドルの保険に加入しています。彼らの資金はすべて、ホットウォレットとコールドウォレットを組み合わせて保管されています。

BlockFiは、一致するプリンシパルウォレットと貸付プラットフォームを搭載した人気のあるDeFiプラットフォームです。

これにより、個人はBlockFiインタレストアカウント(BIA)を介して暗号通貨の保有に関心を持ち、デジタル資産を借り入れ、取引の手数料をゼロにすることができます。

提供される暗号通貨

BlockFiを使用すると、13の暗号通貨に関心を持たせることができます。

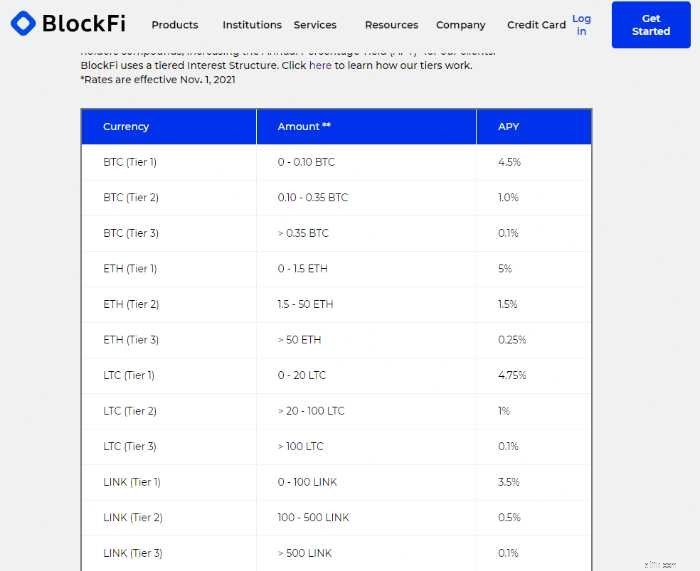

あなたが得るAPYはあなたが持っているコインとあなたがBIAに割り当てる量に依存します。ここでBlockFiの最新料金を確認できます。

最低5000ドルの引き出しに加えて、米ドルをシンガポールの銀行に戻すための手数料がかかります。

ただし、BlockFiは、毎月、暗号通貨に対して1回の無料引き出しと、ステーブルコインに対して1回の無料引き出しを提供しています。したがって、コインを別の暗号通貨ウォレットに引き出したり、ジェミニのように交換したりできます。そこで、それを法定紙幣に戻し、シンガポールの銀行口座に送ることができます。

これは人気のあるプラットフォームですが、現時点でBlockFiが提供する金利は最も魅力的ではありません。

ステーブルコインは、価格が実世界の資産に関連付けられている暗号通貨です。このため、安定した値を維持することができます。いくつかの例には、Tether(別名USDT)、CircleによるUSDC、およびDaiが含まれます。

多くのプラットフォームは、ステーブルコインで貯蓄/貸付サービスを提供しており、これらは最高の利回りを提供します:

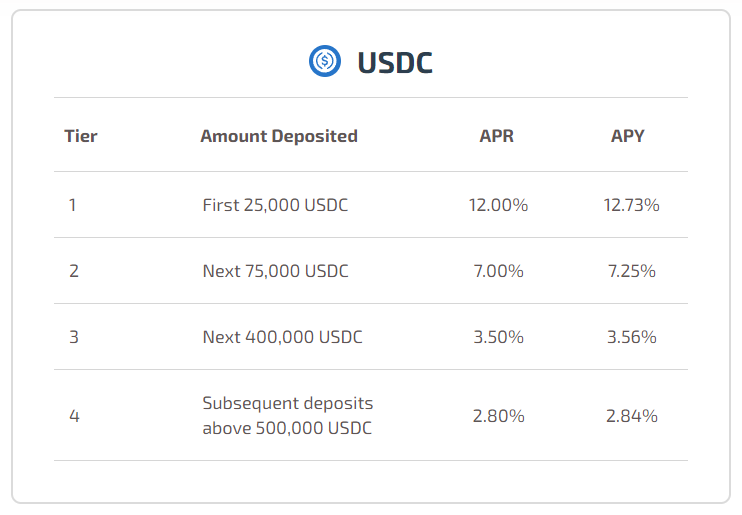

繰り返しになりますが、Hodlnautは魅力的なAPYでリストのトップに立っています:

Hodlnautの利回りは段階的であることに注意してください。これは、預金が増えると、資格のある利回りが低下することを意味します。ただし、回避策があると確信しています。

Youhodlerは、USDTで12.3%、USDCで12%のAPYを達成しています。

Daiを使用して節約したい場合は、YouHodlerが適している可能性があります。

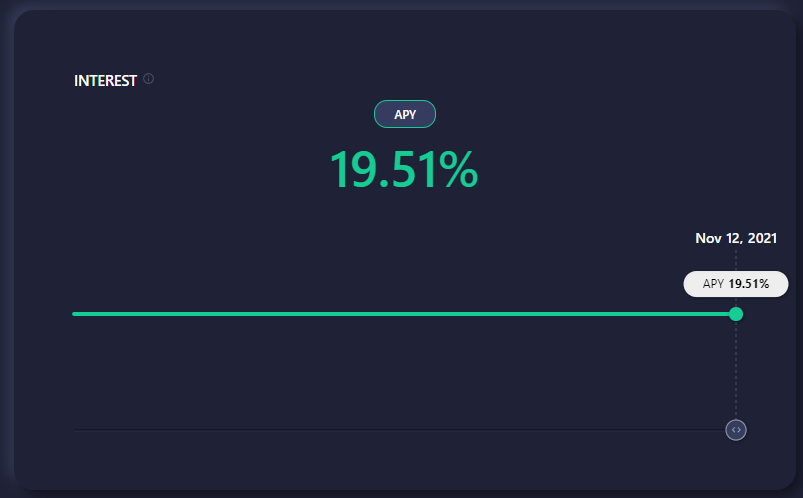

アンカーは、Terraブロックチェーン上に構築された節約プロトコルdAppです。これにより、Terraステーブルコイン預金の低ボラティリティ利回りにアクセスできます。執筆時点では、USTの利回りは19.51%APYです。 USTまたはTerraUSDは、Terraブロックチェーンのステーブルコインです。

アンカーを使用すると、ユーザーはUSTを借用し、プロトコルでLUNAを結合することもできます。

あなたのUSTに興味を持ってもらうために、あなたは最初にあなたの法定紙幣を暗号交換でUSTに変換する必要があります。次に、USTをTerraStationウォレットに送信し、アンカーにデポジットする必要があります。

ウォークスルーに興味がある場合は、下のコメントでお知らせください。

詳細については、AnchorProtocolのホワイトペーパーとTerraホワイトペーパーをご覧ください。

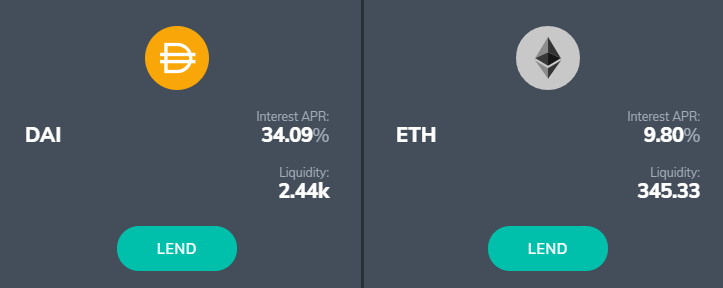

Fulcrumは、融資と証拠金取引のためのDeFiアプリです。これはbZxプロトコルで実行され、ユーザーがイーサリアム、ビットコイン、ポリゴンのブロックチェーンで暗号通貨を貸し出すことができます。

フルクラムの金利は常に変化しており、魅力的に見える週があります:

Fulcrumは安全に使用できると主張していますが、いくつかの危険信号がありました。

要約表にないのはなぜですか?!

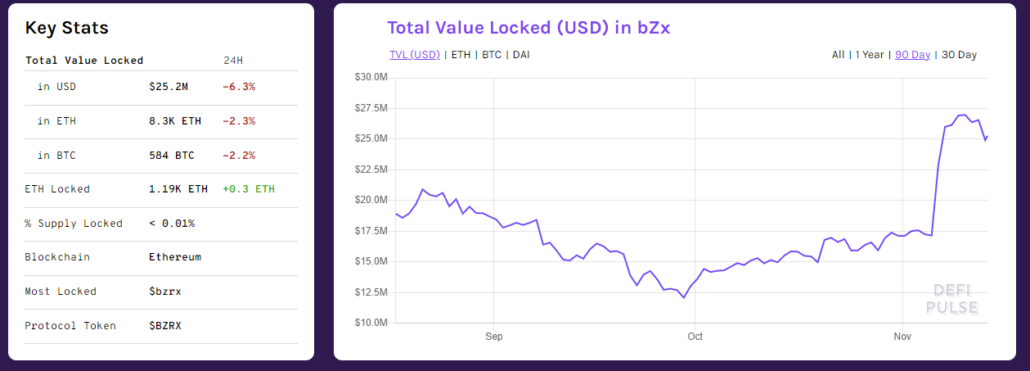

Fulcrumの料金は魅力的であり、市場に出回っているAPYを提供できる可能性があります。 DeFi Pulseによると、bZxプロトコルには約2400万米ドルの価値があります。

問題は、彼らが約束された利益を果たすことができるかどうかにありません。代わりに、それはプロトコルの脆弱性にあります。

脆弱性

通常、プロトコルまたはdAppが一度ハッキングされた場合でも、ユーザーは2度目のチャンスを与えるのに十分快適です。これは、チームが警戒を怠らず、セキュリティを強化するためにより多くの努力を払うためです。

残念ながら、このプロジェクトについて同じことを言うことはできません。本当に suay (または、チームは気にしないかもしれません)、複数の「ハッキング」によってかなりのお金を失ったためです。

あなたは彼らのプロトコルを使って高収量を追いかけることができます。ただし、これは非常にリスクの高いプレイであることに注意してください。また、DeFiの成長を考えると、Fulcrumに似たdAppが存在するでしょう。つまり、高いリスクとともに高い利回りをもたらすプラットフォームです。

そのため、苦労して稼ぐお金を投入する前に、常に自分で調査することを忘れないでください!

上記の利回りは確かに魅力的に見えます。それでも、コインを送金しなければならないのは面倒だと感じる人もいるかもしれません。他の人は、扱うべき財布や口座がたくさんあることを考えると、資産をどこに駐車したかを忘れてしまうのではないかと心配するかもしれません。

それがあなたなら、私はあなたにいくつかの良いニュースがあります。あなたの暗号交換は、それが何であれ、おそらくそのインターフェース内で「稼ぐ」または「節約」プログラムも提供します。怠け者の場合は、その単一のプラットフォームで法定通貨と暗号通貨を預け入れ、購入し、保持するだけです。

ビットコインとイーサリアムで7%のAPY、Dai、USDT、USDCなどのステーブルコインで12%

TokenizeExchangeの本社はシンガポールにあります。持ち株会社であるAmazingtechPteLtdの下でMASPS Actから免除されています。その名前が示すように、これは暗号交換でもあります。

提供される暗号通貨

その暗号獲得サービスの下で、あなたは47の暗号通貨の利回りを賭けて稼ぐことができます:

30日間の最小保持期間と、各暗号通貨に必要なさまざまな最小量があることに注意してください。 TKX、Tokenize Exchange独自のトークンを賭けることで、より高い利回りと柔軟な預金期間のロックを解除できます。

ステーキングTKXには、この記事の範囲を超える他のメンバーシップ特典も付属しています。

引き出し手数料が適用されます

暗号通貨をTokenizeExchangeプラットフォームから移動するときは、引き出し手数料を支払う必要があります。これらの料金は暗号通貨の種類によって異なるため、このリストで最新の料金と引き出し限度額を確認できます。

資金には保険がかけられていません

あなたの資金には保険がかけられていませんが、Tokenizeは、「クライアントの資金は資本スタックの最上位にあるように構成されており、Tokenizeはどのクライアントよりも先に損失を被るでしょう」と述べています。

1か月間資金が滞るリスクや、ブラックスワンイベントの場合に撤退できないリスクに不安がある場合は、Tokenizeの高利回りは適切ではない可能性があります。

銀行からSGDを入金できます

TokenizeでSGDに資金を提供し、取引するのは非常に費用がかかります。 「通常」階層のほとんどのユーザーの場合、Xferを介してアカウントに資金を提供する必要があります。すべてのデポジットには0.55%の手数料がかかります。

プレミアム(160 TKX *の費用)およびプラチナ(800 TKX +ステーク800TKXの費用)のメンバーは、銀行から直接無料でSGDを入金できます。または、米ドルでアカウントに無料で資金を提供することもできます。

*執筆時点では、TKXは約US $ 10で取引されています。

取引手数料は少し高い

通常のTierユーザーの場合、法定通貨から暗号通貨への取引の取引手数料は0.8%ですが、暗号通貨から暗号通貨への取引は0.25%です。代わりに、Geminiのような取引所を使用して、ステーブルコインを購入してTokenizeに転送することをお勧めします。

とは言うものの、彼らの貯蓄率は執筆時点で最も高く、PS法から免除されています。したがって、私はTokenize Exchangeアカウントを使用して、Ethereumのほとんどを処理します。

あまり手間がかからない場合は、ここでアカウントにサインアップできます。

ビットコインとイーサリアムで4%のAPY、Dai、USDT、USDCなどのステーブルコインで2.5〜6.5%

AAXは、ロンドン証券取引所グループのミレニアム取引所マッチングエンジンを搭載した香港ベースのプラットフォームです。それが既存の証券取引所と提携していることを知ってより安全だと感じるなら、これはプラスの要因です。 TradFiにリンクされているという考えが気に入らない場合は、これがマイナスの要因になる可能性があります。

AAXは、MASのPS法に基づくライセンスの保持を免除されています。

提供される暗号通貨

AAXの普通預金サービスは、さまざまなリターンで、柔軟な貯蓄と固定預金の両方を提供します。 $ PSGや$ SHIBなど、100以上のコインの節約オプションを提供します。

執筆時点で、彼らは固定貯蓄のプロモーションを行っています。これらは固定預金プランのように機能するため、最小サブスクリプションとロックアップ期間に注意してください:

保険はかけられていませんが、「暗号通貨セキュリティ標準(CCSS)」に準拠しています

AAXによると、セキュリティは最優先事項です。彼らのデジタル資産のほとんどは、おそらく安全なオフラインストレージ施設に保管されています。

SGDを入金できません

執筆時点では、ユーザーはフィアットSGDをAAX.comに直接入金することはできません。代わりに、アカウントのアドレスに暗号通貨を送信できます。

引き出し手数料

AAX.comは、コインごとに異なる引き出し手数料を請求します。料金の完全なリストはここにあります。

補足:1BTC未満での入金、送金、引き出しのみを目的としている場合は、AAXでKYCを実行する必要はないようです。

ビットコインで1.49%APY、イーサリアムで2.05%APY、DaiやUSTなどのステーブルコインで7.99%APY

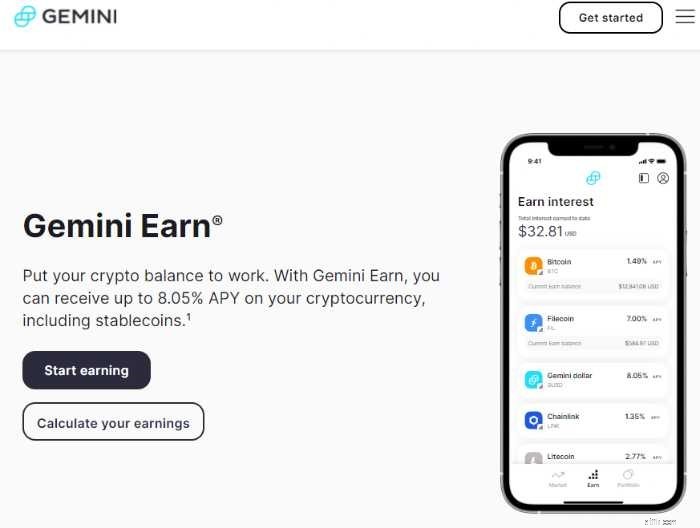

Geminiは、私たちが推奨する暗号通貨交換所です。 MASのPS法に基づくライセンスの保持は免除されます。

すでにGeminiを使用している場合は、その貸付プログラムであるGemini Earnを使用して、暗号通貨の利息をすぐに得ることができます。

Bitcoin、Ethereum、さらにはAxie Infinityなどの40以上の暗号通貨や、TerraUSDやDaiなどのステーブルコインで関心を集めることができます。

最低入金額や保有期間はありません

強制される最低額や期間はありません。コインをEarnに移動した翌日から、利息は毎日支払われます。

料金はすでにAPYに反映されています

ジェミニはあなたに支払う前にローンの代理人手数料を取ります。したがって、反映されるAPYは、獲得する金額です(これらは、市場の需要に応じて変動する可能性があることに注意してください)。

これは、あなたが見るものがあなたが得るものであることを意味します。

執筆時点では、BTCとETHのレートは1〜2%です。ただし、DaiやTerraUSD(UST)などのステーブルコインで最大7.99%のAPYを得ることができます。最新のジェミニ獲得率はこちらで確認できます。

Gemini Earnは、米国、シンガポール、香港でのみご利用いただけます。

割り当てと引き出しが簡単

数回タップするだけで、Geminiモバイルアプリまたはアカウントを使用して、コインをGeminiEarnに割り当てることができます。

法定紙幣を引き出すには、コインを売ってから引き出しを開始します。 FASTを使用して現金を引き出すことができますが、処理には1日かかります。 Geminiからの引き出しごとにS $ 20,000の上限があることに注意してください。

Gemini Earn Fundsは、サードパーティのパートナーによって保険がかけられています

ジェミニはそのセキュリティを重要視しています。 Digital Asset Insuranceを通じて顧客の資金に保険をかけ、ユーザーの暗号を冷蔵保管します。

ただし、Gemini Earnプログラムに基づく資金は、Geminiによって保険がかけられていないことに注意してください。代わりに、サードパーティのパートナーが保有しています。

現在、ジェネシスはジェミニアーンのメインパートナーです。これはデジタル通貨グループの子会社であり、その管理下にあるすべての暗号通貨に保険をかけると主張しています。

ビットコインとイーサリアムで4%のAPY、DaiやUSDCなどのステーブルコインで8%

Touted as the largest crypto lender, Nexo was launched in 2018. It also has an exchange from which you can buy and sell crypto. Its UI is pretty easy to navigate.

Although it offers better rates among exchanges, Nexo is NOT exempted from holding a licence under MAS’ PS Act.

This means that while we still have access to Nexo, we face the risk of having to shift assets if the platform is forced to stop serving Singapore users in the future. After all, this is happened to Binance.com and Huobi Global uers.

Cryptocurrencies offered

Nexo allows users to earn interest from 24 cryptocurrencies.

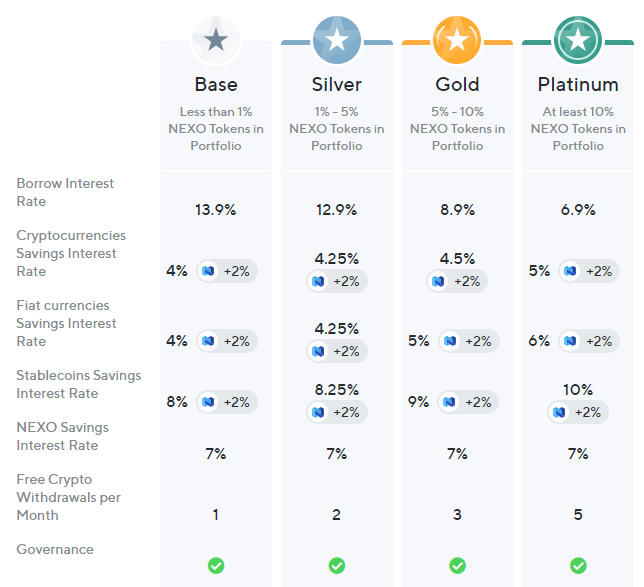

Higher yields and other perks with their loyalty program

Nexo seems to be building a loyalty-based ecosystem. Users are granted loyalty tiers based on the amount of NEXO Tokens held.

You will be rewarded with perks like free withdrawals and better yields based on your loyalty tier.

At the lowest tier, you can earn 4% on your Bitcoin and Ethereum holdings:

You can also earn 8% on stablecoins:

Opting to earn using NEXO tokens unlocks an additional 2% yield. However, you should note that NEXO tokens are not stablecoins, which means you will be exposed to further volatility.

If you want to chase higher yields, you can try to find a comfortable balance between the risk and reward of holding NEXO.

Your holdings are insured

Nexo stores its clients’ assets with BitGo, an insured qualified custodian. It insures against commercial crime for up to USD100M. It is also working with Ledger to insure assets up to USD375M.

Free Withdrawal (fiat)

Nexo mentions that it follows a #ZeroFees policy. This means that users can “make unlimited free-of-charge fiat withdrawals, crypto, and fiat transfers into their Nexo Wallet.”

All users are also entitled to one free crypto withdrawal per month. You can get more of this by holding the NEXO token (more on this below).

That said, there are three things to note:

1.5% APY on Bitcoin, 3.5% APY on Ethereum, and 6% on stablecoins like Dai, USDT and USDC

Crypto.com is another crypto exchange that is exempted from holding a license under MAS’ PS Act. Like others that were mentioned in this article, it has a service that lets its users earn interest on their coins.

Although it claims to provide up to 14.5% on its main page, actual yields are lower if you don’t plan on holding many CRO tokens. You can check the latest APYs that Crypto.com Earn offers here.

For even higher yields, you can choose to stake Crypto.com Coins (CRO). Stakers can also enjoy benefits on Crypto.com’s VISA card. It grants you a free Spotify subscription for staking USD400 worth of CRO.

Although similar in concept, staking is a whole other can of worms that should be covered in a separate article.

You may be able to get higher yields by fulfilling certain criteria on Crypto.com. However, I personally feel like it’s too much work. Plus, I don’t like the idea of having to stake USD400 in CRO to unlock higher yields.

Minimum deposit amount

There’s a minimum deposit required. This threshold depends on the coin you’re depositing into Crypto.com Earn. You can refer to the full list here.

At the time of writing, you need about $500 worth of BTC or $950 worth of ETH to start earning on Crypto.com.

Your deposit will earn interest in the same currency, and yields will be deposited into your crypto wallet every seven days.

Funds are insured

Crypto.com has an insurance fund that is said to cover all uncovered losses.

Furthermore, they hold the cryptocurrencies of all their users in a cold storage powered by Ledger Vault, which is secured by a USD750M cold storage insurance. In theory, this would reduce the risk of losing your cryptocurrencies to hacks and third party theft.

Suppose you want to beat the average yield of a traditional bank savings account, but don’t want to buy cryptocurrencies directly.

What if there’re platforms that let you deposit your fiat SGD, do all the work for you and lets you earn higher interest at the same time? Let’s explore an option and your potential risks:

If all the aforementioned options are too complicated for you, DeZy is a good way to start growing your money while you learn about crypto and DeFi yields. (But, they give you $10 just for signing up and verifying your account. #freemoney)

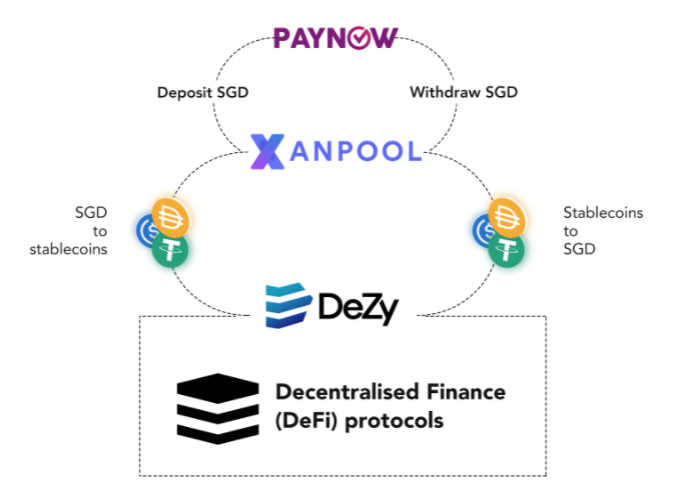

What is DeZy?

DeZy allows users to grow their money at an annual percentage yield of 5%.

The main draw to using DeZy is its simplicity. You can deposit Singapore Dollars directly through PayNow and immediately start earning 5% APY. There is no need to buy cryptocurrencies nor understand the underlying DeFi protocols.

The platform is created for the non-crypto audience, so the process to start is simple:

How does it work?

On the backend, DeZy will take your fiat SGD and convert it into a pool of stablecoins via Xanpool. Then, it will generate a stable yield by deploying the stablecoins through various DeFi protocols.

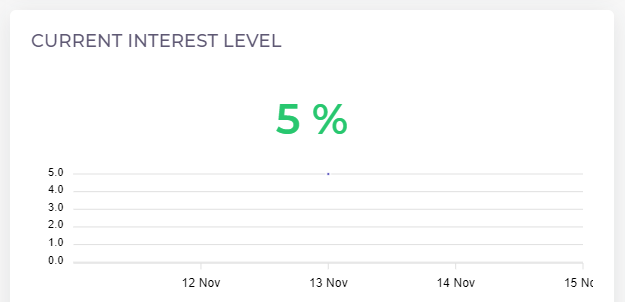

These transactions are said to be processed using “automation and programmatic processes,” and DeZy aims to provide a stable yield of 5.25% APY over the long term. At the time of writing, the interest level is at 5%.

DeZy mentions the use of DeFi protocols like Unagii, Vauld, and Orion on its FAQ page.

Key Risks

DeZy sounds like a great platform to start with, but there are a few issues that may be a cause for concern.

i) Lack of MAS license or PS Act exemption

First, DeZy is not exempted in the PS Act. According to their FAQ, they do not handle the custody of your funds; instead, the funds are distributed across DeFi protocols.

To me, this is a major risk because they could shut down their website anytime and users would not be able to get their funds back. I raised this concern in their Discord and was referred to this article where they state that “your funds are still present and recoverable on the blockchain. Through our on-boarding partners and through the security of the blockchain, your funds would still be technically retrievable.”

That said, given the minimalist UI and lack of accessible information, users with zero experience in crypto will definitely have trouble finding the relevant blockchain transaction details should DeZy go down.

ii) The question of credibility

Secondly, although their business is registered in Singapore, there is a lack of coverage about the project and the team. There are also little reviews online about the platform. All we know is that DeZy’s co-founder and CEO, Eric Dadoun, is a founding Partner at Impiro, a Singapore based VC fund that is backing DeZy.

Another thing that stood out to me is its security page, where there seems to be an over-emphasis on keeping your DeZy account safe using things like 2FA. However, there is little explanation of its “automation and programmatic processes 」。 There is just a brief mention of some of the DeFi protocols it uses to generate yields under its FAQ page.

That said, DeZy is a relatively young company (it was founded in May 2021) and they might still be in the process of building up their documentation and website.

Their CEO Eric Dadoun answered questions regarding the risk of using DeZy in his recent interview with Yield Labs (from 1:01:01 onwards):

In the interview, he mentions a few key takeaways that you should note before considering DeZy:

Convenience comes with a price

I think that the risk is reasonable if DeZy allows you to grow your money faster than traditional banks. You may not understand how it works under the hood, but for a 5.25% APY, it seems like a fair price to pay.

However, you may think that it’s not worth the risk. After all, DeZy’s APY is still lower than the other platforms we looked at in this article. If so, then I would encourage you to learn more about DeFi. I also suggest that you use crypto savings accounts or protocols that could deliver higher returns for a similar risk to reward ratio.

That said, DeZy is giving new users $10 just for signing up and verifying their account. You can get your free $10 here.

Similar to DeZy, Outlet Finance allows users to deposit fiat cash and grow their money at higher yields.

But unlike DeZy, Outlet Finance has several (good) reviews on Trustpilot, and they have a smart contract insurance by Nexus Mutual. They have also launched a debit card for US users on Luna.

Unfortunately, it is not available for Singapore users yet.

There’s no free lunch. Although the yields of crypto savings accounts are highly attractive, they come with considerable risks.

Cryptocurrency is a new frontier. While governments are still wrapping their heads around the concept and figuring out ways for fiat currencies and markets to co-exist with cryptocurrencies, regulations remain relatively loose.

This also means that:

In Singapore, up to $75,000 of your deposit in each bank is protected by the Deposit Insurance Scheme. However, not every crypto savings platform provides insurance on your deposits.

The platform risk is very real. There has been a history of platform hacks like the infamous Mt Gox hack. Do keep in mind that you are taking on the risk of losing your deposits in the case of such hacks.

If you value security over yield, read our guide on crypto hardware wallets instead.

Depending on the platform you use, you may not have the liquidity that bank savings accounts can give you.

On platforms like Nexo and protocols like Yearn Finance, there are lock-up periods where you would not be able to withdraw your coins in exchange for higher yields.

Meanwhile, withdrawals on platforms like Gemini and Youhodler might take a few days. This leads to the next risk:

While earning higher yields, your crypto portfolio remains susceptible to market volatility. For example, earning 7% on Bitcoin during a bear market may be uncomfortable for you, given that there had just been a price drop of 40%. That said, if you’re planning to hodl for the long term, you should be mentally prepared for this risk.

Now, price volatility doesn’t apply if you’re capturing yields using stablecoins. However, stablecoins do come with their own set of risks:

Although stablecoins provide a range of utility across various protocols, their underlying value remains debatable.

Koning suggests that stablecoins are like loans. You lend them to stablecoin entities like Tether and Circle (behind USDC), and as it is with any credit, there is a possibility that you would never get your principal back.

時は金なり。 In summary,

The information is accurate at the point of writing, but you should check for the latest rates before deciding if this is for you.

I like to keep things simple. I do not earn on my Bitcoin, instead opting to store it in a hardware wallet like Ledger. Meanwhile, I earn yields on Ethereum in Hodlnaut, stablecoins like UST via Anchor and for altcoins with smaller positions, I just use Gemini Earn.

And since I’m lazy, I tend to avoid platforms with convoluted reward tiers or those that require me to hold the platform’s native coins. If you don’t mind putting in the extra effort and taking up a little more risk, you could consider unlocking higher yields on platforms like Nexo.

The best crypto savings account for you is the one that suits your risk appetite and convenience. Remember that there are risks involved, so do your own research and only use money you can afford to lose.

If you’re looking to get started in cryptocurrency, join our crypto trainers for a live masterclass to get your basics down.