私はサンドイッチ世代に属しています。

実は、私はサンドイッチではありません。私はただのハムです。私の両親と子供たちはパンです。一緒にサンドイッチを作ります。

サンドイッチ世代は新しい問題ではありませんが、日常的にそれについて実際に話し合う人は誰もいません( 時間はどこにありますか? 。

この投稿が長いことを知っています。そのため、今すぐ読む時間がない場合は、ここからダウンロードして後で読むことができます。

私たちハムは最近、NTUC Incomeの広告を通じて、サンドイッチ世代がいかに厄介であるか、そして将来の世代が私たちと同じ運命をたどらないようにするために財務計画を真剣に受け止めるべきかについて思い出させられました。

>

サンドイッチ世代の生活の要求はこれらです。

これらは私たちの人生の期待になります。真実は、ある程度の妥協なしに上記のすべてをうまく行うことは難しいということです。

そして、これが 幸福の方程式です。 言う:幸福=現実–期待

言い換えれば、私たちの期待が低ければ、私たちが幸せになるのは簡単です。

私たちの期待が非常に多く、高い場合、私たちは簡単に不幸になります。現実は私たちの期待に決して屈することはありません。それがまさにその通りです。

時々、期待を再調整する必要があります。

たぶん、これらの期待のいくつかは、私たち自身の両親や社会全体によって課されたものです。私たちに根付いているこれらの期待は、私たちが人生で望んでいることを真に反映していない可能性があります。

マーク・マンソンは、質問を逆にすることで見つける良い方法を持っています。

「人生で何が欲しいのか」と尋ねる代わりに、「何のために苦労したいのか」と尋ねるべきです。

だからあなたの期待を再検討してください。あなたはあなたの追求と闘争に値しないいくつかの期待を発見するかもしれません。

それらを識別し、すばやくドロップします。

これは、自分を幸せにするための期待を無差別に下げることを意味するものではありません。あなたの期待のいくつかは本当の欲望になります。

私たちは絶対にできます 期待を私たちが目指す目標に変えます。私たちは野心的でありながら、同時に満足することができます。

ジェームズ・クリアはそれをこの記事にうまく入れています:

ですから、ハムのように塩辛いのは意味がありません。私たちは確かに今日の財政について何かをすることができます( そうでなければ明日もまた、最初に読み終えることができます 。

サンドイッチ世代であることの多くの経済的側面についての私の見解を共有したいと思います。反対する人もいると思います。誰もが自分の見解を得る権利があります。私は自分にとって最善だと思うことをします。あなたも同じようにすべきです。

このガイドが1人の人だけに役立つのであれば、私の考えを書き留めておくと便利だったと思います。

私は家族の中で一人っ子です。

私の両親は裕福ではありませんでしたが、私たちはいつもテーブルに食べ物を置くことを心配することなく快適に暮らしました。しかし、彼らはシンガポール経済の信じられないほどの成長をあまり利用していませんでした。多くのシンガポール人は、過去50年間、活況を呈している不動産市場から何百万ドルも稼いでいます。当時、彼らには不動産に投資するお金がなかったので、私は彼らを責めません。

私は一人っ子なので、子供の頃から注目を集めていました。私はかつてゴーストバスターズの車、マシュマロの男、そして私たちが買うことができるどんな豪華なおもちゃでも所有していました。それが続く間、それは良かったです。

今、私は両親の世話をする時が来たことに気づきました–一人で。私を助ける兄弟はいない。彼らは彼ら自身の引退のためにほとんど節約していません、そして私は彼らのCPFだけでどのように十分であるかわかりません。

私の両親はまだ健康で、自分の家計を稼ぐことができるので、今日も働いています。彼らは私に一定額の手当を要求したことはなく、私が彼らに与えた金額を受け入れます( 収入広告の父とは異なり、tsk tsk )。

私には自分の核家族がいるので、彼らは私にとってそれが簡単ではないことを知っています。私の妻も、2人の息子と私の義母を支援するために働いています。

サンドイッチは次のようになります:

妻と私がいくらお金を稼いだとしても、7つの口すべてを養うのに十分ではないかもしれないというこのしつこい気持ちが常にあります。多分これは私たちが受け継いだことわざのkiasuシンガポールの特徴または慎重なアジアの価値です。十分な量がないことへの恐れは、私たちをさらに一生懸命に働かせます。

多くの場合、それは否定できないストレスの原因になります。

私は幸運にもこれを早く認識し、大学在学中に自分の財政を担当し始めました。資本主義社会ではお金が最も重要な資源だと思いました。それが不足していると、結果は悲惨です。

私は空軍でキャリアをスタートさせました。私は適度によく支払われ、節約して投資しました。絆が終わり、ウェルス博士を始めた後、私は最終的に空軍を去りました。

自分の財政を管理することや、お金に精通した他の友人や投資家との交流について、私が学んだことはたくさんありました。

サンドイッチ世代のシンガポール人を助けるために、私の考えと経験をこのガイドに入れる時が来ました。

私たちの多くは、私たちのキャリアから純資産のほとんどを獲得しています。幸いなことに、サンドイッチ世代の私たちのほとんどは、両親よりも教育を受けています。資格が高いということは、高給の仕事を指揮できることを意味します。しかし、資格は面接またはあなたの最初の仕事までしか私たちを得ることができません。

今後は、成績だけでなく、あなたの能力を証明できなければなりません。うまくいくには、実体と形の両方が必要です。

ほとんどのシンガポール人は形が欠けています。仕事が上手であることが必要ですが、私たちもそれが上手であることを他の人に知らせなければなりません。特に私たちの上司と彼の上司です。

私たちが良いことを誰も知らなければ、昇進の対象となることは決してありません。私たちは自分の能力を認識していないことで上司を非難し、自分の机に嫌がらせをすることになります。それは「わがまま」ではありません。それは世界に私たちの価値を伝えることです。

誇らしげに刺すべきだと言っているのではありません。

私たちは巧妙である必要があり、故意に印象を与えるようなものに出くわさないようにする必要があります。仕事で最も苛立たしいのは、実体がなくても形を誇張している人たちです。

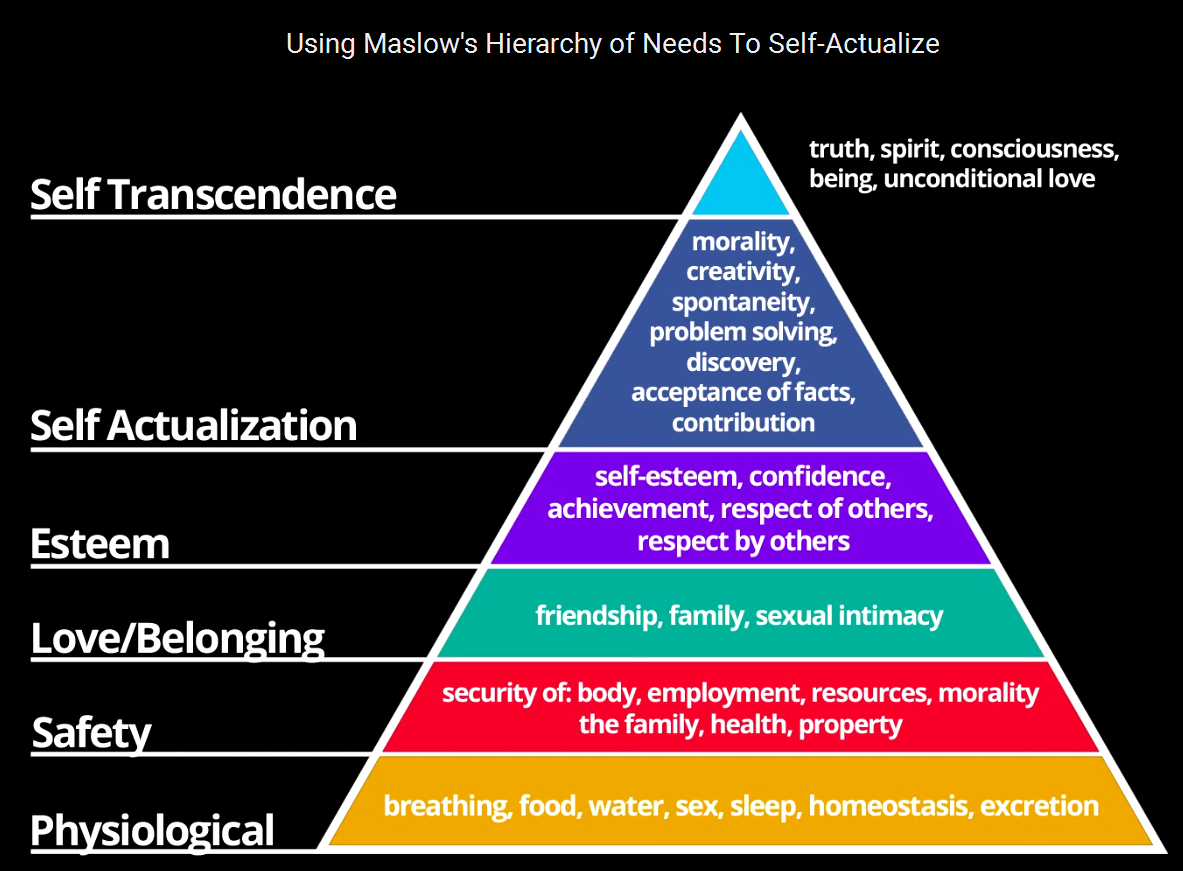

サンドイッチ世代であるということは、私たちに願望がないという意味ではありません。

私たちは有意義な仕事をしたり、私たちの情熱に従いたいと思っています。マズローの欲求階層説にさらされています。

また、好きな仕事でお金がほとんどかからないか、あまり好きではないけれど気にしない仕事で、どちらがより多くのお金を払うかを選択しなければならない場合があります。

ほとんどの場合、後者を選択しますが、毎日、仕事中に私たちのごく一部が死んでいるように感じます。私たちは時々人生の意味に疑問を投げかけ、ラットレースから抜け出すのに十分なお金を持てることを願っています。私たちは早期退職を夢見ています。

ここに F ** k You Money を入力します 概念。ナシム・タレブからこの用語を選びました。

これが彼の F ** k You Money の定義です。 、

F *** You Money があるので、このコンセプトが好きです。 自由を意味します。

それはあなたがするすべてのことにあなたに熱意を与える強力な人生の目標です。そして希望は強力なものです。

しかし、それを達成するためには、経済的自由を達成することに注意する必要があります。

早期にキャリアを辞めただけで、引退が退屈だと感じた人もいます。私たちは皆、何かすることと楽しみにすることが必要です。したがって、あなたはあなたが何をしたいのかを知らなければなりません。それはただ自由を持つことではありません。 それはあなたが好きなことをする自由を持つことです。

2番目の部分を決して忘れないでください。

F *** You Moneyの蓄積をスピードアップする際に、起業家精神に頼る人もいます。

幼い頃に必要な正しい考えを得るのは非常に難しいので、学校を卒業してすぐにビジネスを始めることはお勧めしません。

できる人は少数ですが、ほとんどの人はできません。空軍と結ばれていたので、選択の余地がなかったのは幸運でした。

そこでの数年間、私は自分自身と世界がどのように機能するかについて多くを学びました。私は非常に理想主義的であり、後でビジネスを始めたら失敗したであろうことに気づきました。したがって、ある程度の成熟度と定着性を持つことは、実際には、起業家精神の成功の確率を向上させるでしょう。

実際、ほとんどの人は起業家精神に適していません。

あなたは自分自身を知る必要があります。はい–成功すればたくさんのお金を稼ぐことができますが、失敗するリスクはかなり高くなる可能性があります。

サンドイッチ世代にいるということは、リスクを単独で負っていないことを意味します。あなたの扶養家族はあなたと一緒に危険を冒しています。

困難な起業家精神の旅を乗り切るためには、親しい人たちのサポートを得ることが重要です。

起業家精神があなたのやり方ではない場合、あなたの引退まで雇用されることは悪い選択肢ではありません。

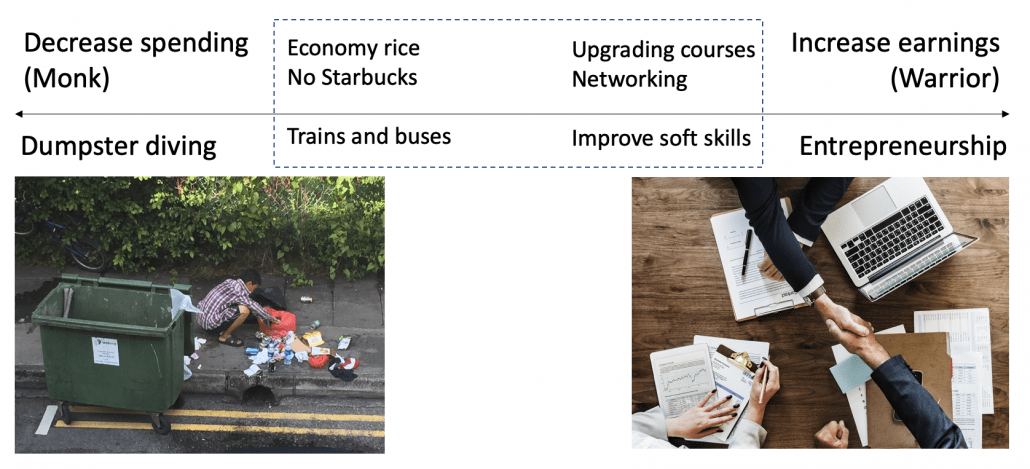

投資やビジネスを行わずに一貫して富を築くには、主に2つの方法しかありません。収益を増やすか、支出を減らすかです。

成功した起業家は多くの富を生み出すことができますが、高給を稼ぐことができる企業登山家もいる可能性があります。

収益を増やすことができない場合は、 F ***あなたのお金を貯めるために支出を減らす必要があります 。

それはすべて、あなたの許容できる生活水準に要約されます。ゴミ釣りに積極的な人がいることを私は知っています–無料の使用済みのものと不要だが食用の食べ物を手に入れます。もちろん、スペクトルのその端に行く必要はありません。

シンガポールは高価な場所ですが、安く暮らす方法もあります。本当に選択です。

このスペクトルの両端について、ここで詳しく説明しました。

私は若い頃からお金を節約するのに問題がありました。私はすべての手当を使い、受け取ったらすぐにお金を稼ぎました。

私が空軍に加わって給料を受け取り始めたとき、私は自分自身を救うことを強制しなければならないことを知っていました。

あなたが私と同じ問題を抱えているなら、私がした次のことがあなたを助けるかもしれません。

まず、POSBSave-As-You-Earnと呼ばれる定期的な貯蓄プログラムを設定しました。それを通して、私は毎月数百ドルを自動的に吸い取った。

第二に、私はすべての貯金を隠しておくために別の銀行口座を始めました。私のメインの銀行口座は、請求書と経費の支払いに使用されました。これは、貯金に没頭しないようにするためでした。

封筒を使って予算を組む人もいます…

またはマネージャーシステム

基本的に、持続可能な方法で長期的に行動を改善するためのシステムを作成します。始める前にやめた人ではありません。

過剰な支出を正当化するためにあらゆる種類のストーリーを発明するので、自分を信用しないでください。

有名な物理学者のリチャード・ファーンマンが言ったように、 「最初の原則は、自分をだましてはいけないということです。あなたはだまされやすい人です。」

代わりにシステムを信頼してください。

時間が経つにつれて、お金を節約することが習慣になるように、お金を大切にするという考え方にシフトしたいと思うでしょう。しかし、誤解しないでください。経費はすべて悪いわけではありません。あなたはまだ人生で素晴らしいものと経験を持っている必要があります。使う必要がある、または使いたい場合は、それが価値があることを確認してください。

あなたがお金を大切にするのを助ける一つの方法は、生命エネルギー交換の観点からお金を考えることです。ほとんどの人はお金と引き換えに働かなければなりません。たとえば、LVバッグを購入する前に、それを支払うために働く必要がある時間数を計算します。数が400時間または2か月の仕事であることが判明した場合、それはあなたがそれを購入するのをやめさせるかもしれません。このアイテムがあなたの人生から差し引かれるその時間の量の価値があるかどうか自問してください。それでも価値があると思うなら、それを選んでください。

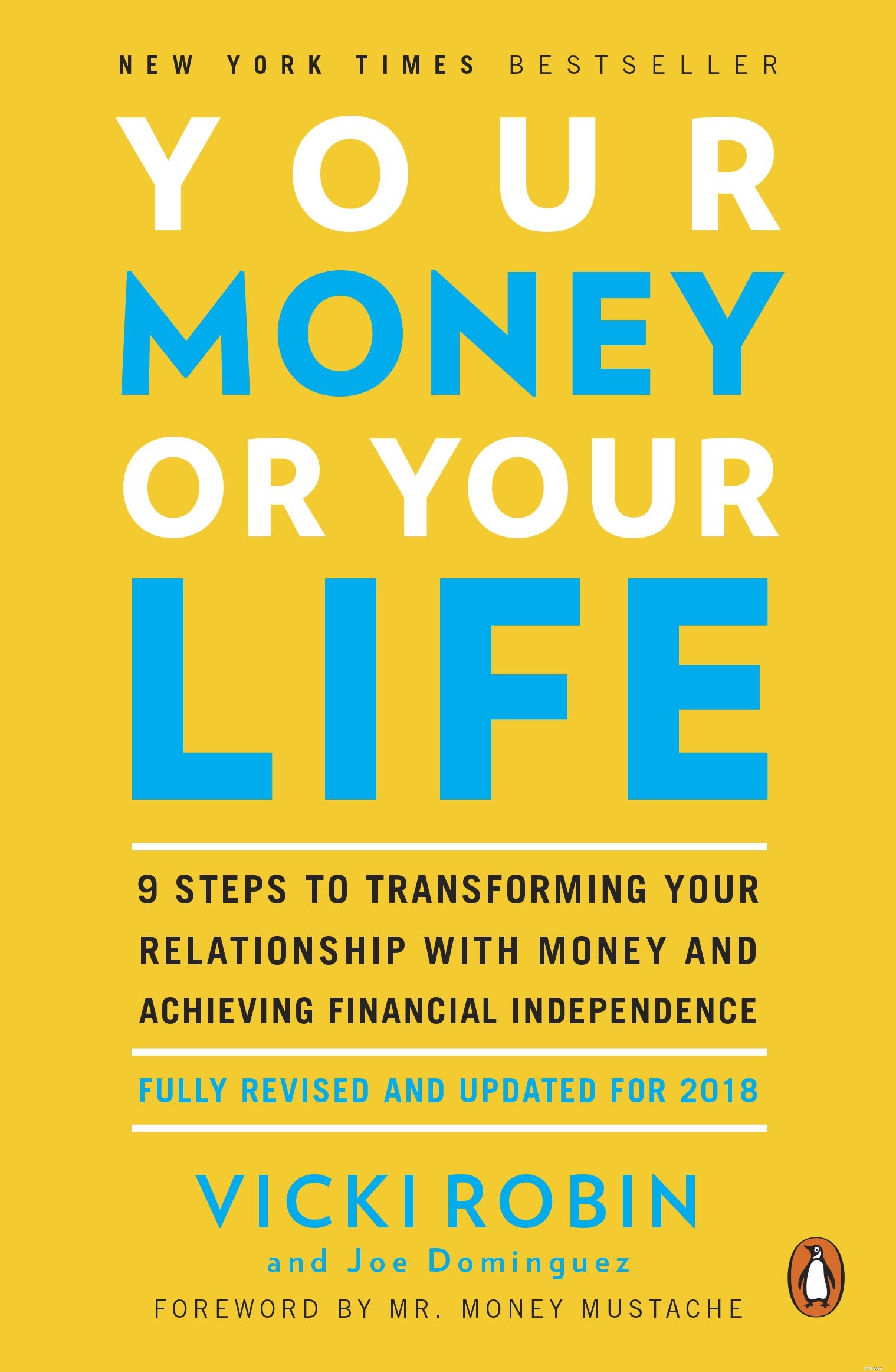

この概念は、本「あなたのお金またはあなたの人生」で詳しく説明されています。 。

何に費やすかを決める際の経験則は、物ではなく経験を購入することです。この原則は、幸福に関するこの研究から外されています。

それが意味することは、フェラーリを購入しないでください。フェラーリには、メンテナンスや安全な駐車場を常に見つけなければならないなど、所有権の問題がたくさんあるからです。 1つを借りて、体験のためにそれを運転してください。記憶は長続きします。最も重要なことは、物事の代わりにあなたの年老いた両親の経験を買うことです。それらの経験に参加する方が良いでしょう。あなたの交際は彼らが最も望んでいるものです。

旅行は体験を買うことでもあります。ただし、旅行したくない場合は旅行しないでください。シンガポールに滞在して好きなことをやっていて元気な人を知っています。ソーシャルメディアの知人は全員そうなので、旅行にプレッシャーをかけないでください。また、旅行する場合は、旅行の終わりに向けて最高の思い出を保存することを忘れないでください。これは、心理学者が、人間が経験のピークと終わりを覚えている一方で、他のすべてのことをほとんど忘れていることを観察しているためです。

親として、私たちは子供たちが人生で成功するための最高のチャンスを得られるようにするために教育に多くを費やしています。これは、私たちの社会が学業成績を過度に強調している結果です。それは教育的な軍拡競争となり、子供たちに数え切れないほどの授業料と充実の時間を費やすことを含みます。授業料以外の方法で子供を育てるのにお金を使うのが理にかなっている場合があります。ここに他のヒントについて書きました。

ウォーレンバフェットの投資見積もりは、それを支出に適用する場合にも関連します。「価格はあなたが支払うものであり、価値はあなたが得るものです。」

最後に、あなたの財政を追跡することを忘れないでください。管理のことわざにあるように、測定されるものは改善されます。

あなたのお金がどこに行ったかを知るためにあなたの費用を追跡することは間違いなく良いことですが、それはこの経済的な旅であなたを焼き尽くすかもしれません。私は1年間それをしました、そして私は私がどのようにお金を使うかについてかなり良い考えをほとんど得ます。私はそれを継続的に行うように訓練されているわけではなく、あなたに最適なものを決定するのはあなたに任せています。今は簡単な予算編成をしているので、どの分野で支出しがちなのかがわかり、最終的にはそれらの分野をより注意深く見守ることになります。

多くの金融ブロガーはこれについて非常に良いアドバイスをしています。 Thomasは、なぜ予算(YNAB)アプリケーションが必要なのかについて書いています。 Kyithはまた、予算を立てる方法や、経費の追跡が面倒な場合に純資産を追跡する方がよい理由について多くのアイデアを持っています。あなたのために働くことは何でもしなさい。それがあなたが長期間にわたって追いつくことができるものであることを確認してください。

お金の節約に関するこのセクションを締めくくるには、次の3つのヒントを覚えておいてください。自動的にお金を節約するのに役立つシステムを作成します。あなたが費やす必要がある場合は、それが本当に価値があることを確認してください。あなたの財政を追跡しますが、それを持続的に行います。

あなたは一握り以上のファイナンシャルアドバイザーに会う予定であり、あなたはすでにいくつかの政策を購入していると思います。保険に関する基本的な知識を身に付けておくことを強くお勧めします。

保険は、数年後の次のレビューや生活環境が変化するまで、私たちが購入して取っておくことです。保険業界の動向を追うには時間がかかり、時間のかかる費用ではないと思います。専門家に仕事をさせ、その時点で市場で最高のポリシーを推奨させます。

あなたの仕事は、適切な質問をするのに十分な業界の第一原理を理解することです。あなたの仕事はまた、そこにいる良いアドバイザーと悪いアドバイザーを区別できるようにすることです。

保険のトピックは、製品が構造化され、販売のために一緒にバンドルされる方法のために混乱する可能性があります。それらを全体的に理解するために一歩後退しましょう。以下は、頻繁に遭遇する一般的な用語です。

保険には2つの経験則があります。

両方のルールに合格する必要があります。

これらのルールを適用すると、投資商品は明らかに除外されます。保険会社から投資商品を購入することはありません。

私は保護と投資を別々に保つことを好みます。

保護にはコストがかかります。

保護と投資の両方の動機を同時に満たそうとすることは、2-in-1シャンプーとボディウォッシュを使用するようなものであり、この製品はどちらの仕事も得意ではありません。たとえば、私は定期保険に加入することを好みます。そうすれば、十分な補償を受けることができます。

生命保険契約の予想満期価値に誘惑されるのは非常に簡単です。対照的に、タームポリシーは、毎年多くのお金を払っており、最終的には何も得られないと見なしているため、人々を先送りにします。保険会社はこの癖をよく知っています。生命と投資の方針を捏造することははるかに簡単であり、それらは人が買うことができる保護のはるかに高価な形です。

私の意見では、入院計画は最も重要な保険です。私たちの政府がMediShieldLifeをすべての人に義務付けたのには理由があります。これは、医療費の大部分をカバーし、財政からそれを前に出す負担を取り除くためです。入院するのに十分深刻な病気は多くの費用がかかり、入院計画はそのほとんどをカバーする必要があります。

それがあなたがむしろ余裕がない何かであるならば、あなたは入院計画へのライダーを排除することができます。これは、ライダーが通常、控除対象と共同保険をカバーしているためです。控除対象はあなたが支払う必要がある最初のS $ 3,500です。共同保険とは、請求額の10%を自己負担する必要があることを意味します。これらの支払いをカバーするためにライダーを購入することができます(現在、ライダーとの共同保険は5%にしか下げることができません)。

ルール番号に基づく1、控除対象と共同保険は、大きな経済的打撃を与える可能性が低い管理可能な金額である傾向があるため、それらはちょうど良いものです。

経済的支援をあなたに頼っている扶養家族がいる場合(あなたはサンドイッチ世代にいるので間違いなく)、あなたが彼らを養うためにもう周りにいないときにあなたの扶養家族が空腹にならないようにあなたはあなたの死に対して保険をかける必要があります。定期保険を利用すると、生命保険よりも費用対効果が高いため、十分な補償が受けられます。お金を取り戻すことを心配する必要はありません。保険は費用です。頭の中でそれをドリルします。

残りの保険は持っているのが良いです。たとえば、事故計画を見てみましょう。交通事故で視力を失ったと想像してみてください(木に触れてください!)。あなたは入院する予定であり、その一連の費用は入院計画に基づいて請求されます。事故計画は現金の一括払いをする予定です。はい、あなたが働くことができないので、現金は重宝します。事故計画は通常高価ではありませんが、ポリシーは合計されます。 1つしか買えないのであれば、事故の方針を確約するよりも、入院計画が水密であることを確認したいと思います。

もう1つの例は、重大な病気の保険です。あなたは、初期の重大な病気が規則番号を通過すると主張するかもしれません。治療費が高いので1。しかし、問題は、ほとんどの人にとってコストがかかりすぎることです。したがって、ルール番号に失敗しました。 2.

補償範囲が限られているので、出産保険の大部分に時間を無駄にすることはありません。申し立てを行う可能性は低く、申し立ても多額にはなりません。

しかし、私の顧問の1人が、妊娠費用を保証する非常に非正統的な方法を紹介してくれました。彼は自分のためにそれをしました、そして彼はそれからお金を稼ぎさえしました。

私はこれについて豆をこぼしているので、彼が動揺するかどうかはわかりません。

基本的に、地元のシンガポール人でも購入できる海外駐在の医療保険があります。ポリシーは実際には包括的な入院計画です。地元の入院計画にはない出産費用をカバーします。

さらに、このポリシーは新生児の補償範囲も拡大します。新生児の最初の15日間は保険を購入できないため、これは重要です。母親を介してポリシーを購入することは、子供に何かが起こった場合の天の恵みです。

問題は、ポリシーが施行されてから12か月後にのみ出産関連の申し立てを行うことができるということです。

このポリシーは、月額約S $ 300の費用がかかる可能性があるため、安くはありません。これは、年間S $ 3,600の保険料になります。ただし、通常の配信ではS $ 8000からS $ 12,000の費用がかかるため、ROIは良好です。赤ちゃんを作るタイミングを正しくとる必要があります。

すべての親は子供たちに最善を尽くしたいと思っています。彼らは、子供たちのために保険を購入することで、彼らに悪いことが起こるのをひどく防ぐことができると考えています。彼らはそれを安心と呼んでいます。

私の方針は、必要なものだけを購入することです。

赤ちゃんには稼ぐ力がないので、生命保険や定期保険は必要ありません。彼らの人的資本に保険をかける必要はありません。実際、家族に新たに加わった場合、保険をかける必要があるのは稼ぎ手である両親です!

稼ぎ手は家族を金銭的に支えている人であり、今では仕事をやめる余裕はありません。したがって、何らかの理由で労働力を離れることを余儀なくされた場合は、子供を育て、高齢の親の世話をするのに十分なお金が残っていることを確認してください。

一つの議論は、生命保険と定期保険の完全な恒久的な障害補償もあるということです。

繰り返しになりますが、子供ではなく、稼ぎ手の報道を増やすことがより重要だと思います。あなたが余剰予算を持っているならば、あなたは考慮することができます。また、将来何らかの状況が表面化した場合に備えて、子供たちが健康なときに購入することもできます。

同様に、重大な病気や事故の計画は、余裕があれば持っておくとよいでしょう。治療費がはるかに高くなることを考えると、重大な病気が優先されると私は考えています。

適切な入院計画が必要です。

最適に統合されたシールドプランを購入します。ライダーはオプションで、持ち運びに便利です。子供用のライダーを購入しました。私の長男は気道が敏感で、多くの医師や小児科医を訪問したにもかかわらず、彼の状態は改善しませんでした。

推薦により、トムソンメディカルで彼を治療できる小児科医を見つけました。

彼は気管支炎のために数回入院しました。

トムソンメディカルでの5日間の滞在は、毎回最大15,000ドルかかる場合があります。幸いなことに、それらはすべて保険によって支払われました。そうそう。入院計画を躊躇しないでください。

サンドイッチクラスにいるということは、両親が病気になったときに両親の世話をする必要があることを意味します。

私の親世代の高齢者の中には、情報に基づいた選択をするのに十分な保険を理解している人はほとんどいません。

負担は今私たちにかかっています。

彼らが言うように、シンガポールは死なない高価な場所です。

最大の心配は、両親のために法外な医療費を請求する必要があるということです。私は多くの仲間と話をしましたが、私たちの多くは両親の保険の必要性に十分な注意を払っていないという結論に達しました。

経験則では、家族の誰かが病気になったときに請求書を提出するように求められる場合は、彼らに支払うリスクを確実に保護する必要があります。

高齢の親は、支払いと保険料を正当化するのに十分な人的資本がないため、生命保険や定期保険が必要になる可能性はほとんどありません。それらはもはや機能しておらず、とにかくサポートをそれらに依存していません。したがって、老後の死亡をカバーするために高額の保険料を支払うことに意味はありません。障害に関しては、金銭的支援を提供するCareShieldLifeがあります。

私はここで壊れた記録のように聞こえますが、これを十分に強調することはできません– 入院計画は、あなたが両親のために購入できる最も重要な方針です。

両親が統合シールドプランを選択した場合、保険料の一部は現金で支払われる可能性があります。

これは、彼らの年齢では、保護のコストがかなりの額になるためです。

その上、統合されたシールドプランのプレミアムに対して、Medisaveを使用して年間300〜900ドル(年齢によって異なります)を支払うことしかできません。現金の要素を買う余裕がない場合は、プランをダウングレードして、許可された控除額の範囲内で保険料を下げる必要がある場合があります。これは、あなたの両親が公立病院を訪問し、特定の病棟クラスに滞在することしかできないことを意味します。

あなたはあなたの保険証券のあなたの受益者を決定するために指名をすることができます。保険金の受益者をカバーする意志を作ることもできます(ポリシーに指名がない場合)。

遺言はCPFの支払いを指示することはできず、CPF理事会に個別に指名する必要があります。意志がない場合、あなたの資産は無遺言継承法またはイスラム教徒の相続法によって決定されます。

私たちが心配する必要があるのは、死亡時の金銭の指示だけではありません。私たちは長生きしており、認知症などの病気の可能性が私たちを襲う可能性があります。その場合は、お金の使い方を決めるために信頼できる人を任命する必要があります。これは、「Lasting Powers of Attorney」(LPA)を介して行うことができます。

サンドイッチ世代として多くの扶養家族がいるので、できるだけ早くこれらの手配をしてください。

私たちの住宅物件の大部分が公営住宅であるシンガポールに住んでいてうれしいです。価格は何年にもわたって上昇していますが、それでもほとんどのシンガポール人にとって手頃な価格です。

はい、BTOフラットは苦痛な待機になる可能性がありますが、その満足を遅らせることができるのであれば、なぜですか?あなたが急いで家を必要とするならば、考慮すべきバランスの販売フラットがあります、あるいはあなたは再販フラットのためにわずかなプレミアムで逃げることさえできます。

ほとんどのシンガポール人が信じていることに反して、私は財産を富への唯一の方法とは考えていません。私の家は投資ではなく、避難所だと思っています。私は何年も後にかなりの利益のために彼らの最初の家を売り払った友人を知っています。しかし、彼らのほとんどは、アップグレードして別のより高価な物件を購入することになり、売り上げはすぐに戻って、より長い保有期間でさらに大きなローンを借りることになりました。

My view is that unless you own a second property and beyond, it is difficult for you to really make good money from properties (we would cover more about investments in the latter part of this guide.)

If you use your CPF to buy a house, you would also need to pay the accrued interest when you sell it. You would have earned the CPF interest should you not use it to pay for your house. Few property investors take this into consideration.

Sandwich Generation peeps, we should all assume that we are going to live until roughly 90-100 years old. This means we are going to spend more years in retirement than previous generations and we will need even more money to fund our golden years.

We have to take care of our own retirement years if we want to be the last Sandwich Generation.

Investing will be key to fund our retirement.

You can consider investment income and CPF in totality to provide the cash flow you need. But I would rather be more conservative and rely solely on my own investments. Whatever remains in the CPF then becomes a bonus.

This is somewhat unconventional because most people would think the opposite way – CPF is the baseline and personal investment returns are a bonus.

Do what works for you, just make sure you have a plan to fund your retirement.

The Government launched CPF Life (L ifelong I ncome F or The E lderly ) Scheme in view that our people are going to live longer than they used to. It is an annuity plan which guarantees a payout in retirement ages until death occurs.

I think this is a good solution for our society but I don’t think the payout is sufficient for myself. This is the reason why I want to take control of my retirement funding and not simply rely on the CPF.

You can augment CPF Life with private annuities which are offered by insurance companies. If you believe that you would live a long life as your parents and grandparents have proven so, annuities might be a good deal for you.

Some Singaporeans believe that topping up their CPF is a good way to earn the guaranteed interest on their money. They may even transfer their CPF OA monies to CPF SA for even higher interest.

To me, it isn’t worthwhile because of the restricted use of CPF monies. Cash has a lot more uses than CPF monies. Topping up means trading the freedom or optionality away.

For example, you cannot use CPF to buy medicine or pay for medical treatment or even hire a domestic helper to help with the aged. Trading away such freedom may be a high price to pay. You don’t want to be asset-rich (high CPF savings) but cash-poor.

We must understand that the purpose of allowing individuals to top up their CPF is to make sure they have enough money for retirement. It is not for people to earn extra interest on the cash they think they don’t need. Do not be penny-wise, pound foolish.

CPF top-up for parents is an exception. If you are planning to give them allowances when they stop working, you might as well use the money to do the top-ups to earn higher interest and get tax relief at the same time.

This is my favourite topic and it is the most difficult activity for most people. We all know that we should invest in order to grow our money. But investments are volatile in nature. Some years we lose money and some years we make money. This makes it very difficult for us to handle. We want to make money and enjoy the capital guarantee at the same time.

It sounds like buying bonds would solve this problem. But we cannot assume bonds are safe because they can default too. Moreover, bonds with better credit-ratings offer very low interests, a very slow way to grow your wealth. Hence you should get exposure to some stocks to boost your gains unless you are super risk-averse and you know you cannot take fluctuation or even accept years with negative returns.

The challenges we faced in investing can be traced back to our ancestry. Our brains are not originally designed to make us good investors. We are wired to find comfort in herds and to run away from danger. We know it isn’t a good idea to buy when the masses are buying (greed drives up prices) and sell when the masses are selling (fear drives down prices) but we cannot help it because of the software that has been programmed in us.

This problem doesn’t go away even if you delegate investing to a professional. Because you can still get greedy during good times and add more capital to your fund manager or advisor to manage, and get fearful during bad times by pulling out your funds.

If you decided to invest, be prepared to lose some money to learn about the markets. In doing so, you will also learn much about yourself. Every successful investor I have met has always learned by losing money first. Sometimes for many years.

On the other hand, I believe the Sandwich Generation cannot afford NOT to invest. We have to take care of many people and at the same time must have enough for retirement. We are left with no choice but to squeeze growth out of every dollar we have.

Currently, the picture doesn’t look very rosy.

Singaporeans are underinvested. Looking at the household balance sheet, Singaporeans have about half of their assets in properties and 20% in cash 。 Less than 5% is in stocks, bonds and funds.

We can definitely do more to make our money work harder.

I would like to document a few approaches to tackle investments.

Most Singaporeans would find investing a very hard subject and would profess that they do not have the necessary skills to make proper investment decisions. Hence they would delegate the task to financial advisors, bankers or even Robo-advisors.

There’s nothing wrong with that but do make sure you are getting your money’s worth if you are paying someone else to invest for you.

Similar to insurance products, you need to find professionals who are the real deal, who are able to deliver returns that are better than what you can get by buying a plain vanilla low-cost fund.

Financial advisors and bankers are likely to construct portfolios consisting of stocks and bonds unit trusts. They follow the Modern Portfolio Theory which posits that allocation to different asset classes (mainly stocks and bonds) would drive most of the returns. One should diversify widely in many stocks and bonds to reduce exposure to any particular stock or bond which may underperform.

Typically the industry has three types of portfolios for you. Stable portfolios are mainly in bonds so they don’t fluctuate that much. This will be highly recommended if you are deemed to be risk-averse.

The Balance portfolios are a good mix of stocks and bonds. You get more returns than the Stable portfolios, while at the same time experiencing higher volatility. In other words, when the market declines, you will also feel it more than the investors who have opted for the more stable option.

Lastly, the Growth portfolios are recommended to the aggressive investors who feel that they can take volatile investments. These portfolios are made up of a greater proportion of stocks.

A risk profiling exercise will determine the degree of your risk tolerance and then the relevant portfolio will be recommended to you.

Most of the time the advisors would use the company’s recommendations rather than customise the portfolios for you because the latter requires a lot more work and experience. It is ok as long as it can deliver performance.

Some advisors would offer to customise for you.

They would say that it is easier to pick funds than stocks. This is where I disagree because I think it is equally hard to make the right choice either way. While there are indeed more options in the universe of stocks, there are also tens of thousands of funds out there. Regardless of funds or stocks, the selection is not just a skill. There is also a big element of luck is involved because we do simply not know what will happen in the future.

From an investor standpoint, it is hard for you to tell luck from skill when evaluating an advisor or fund manager. Investing is far from easy.

There’s a new breed of digital advisors called Robo-advisors. You can easily set up an investment account by answering a few questions. They will size up your risk profile and investment objective and automatically recommend an investment portfolio for you. Most of them would still largely follow the Modern Portfolio Theory to build the portfolios. Some investors like them because they tend to charge lower fees. They also tend to be more fuss-free because everything can be done online. There are others who do not like Robo-advisors because they are pretty new and they lack a proven track record.

The bottom line is, you can consider delegating your investments if you don’t know how to do it, have no interest to learn, or no time to do it yourself. But you will have to pick the right people to do it because you don’t want to end up paying more fees and end up with subpar performance. Don’t ask for low fees, ask for advisors who are worth the fees.

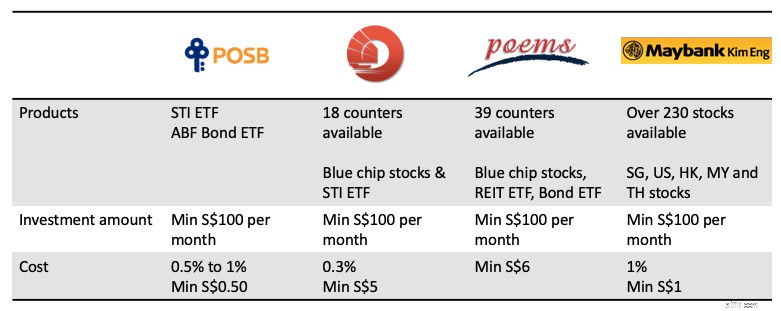

If you have decided to take things in your own hands, the simplest way to go about it is to invest using one of those regular investment plans whereby you can start off from as low as S$100 per month.

You will be able to buy familiar blue-chip stocks or Exchange Traded Funds (ETFs, as the name suggests, these are funds traded on the stock exchange such that you can buy and sell as if they are stocks). Below is a comparison table of the various companies offering such investment plans. It is good to check the costs and terms before investing as the details may change from time to time.

This is one of the lowest barriers to start investing. My wife doesn’t trust anyone to invest for her and she doesn’t have the knowledge to do it herself. So I encouraged my wife to start this program and she was able to set up an account via her banking app. It was fuss-free enough for her to cross the hurdle and make her first investment.

But don’t expect it to do instant magic for you. The investments will still go up and down and sometimes the returns may be disappointing even after a few years. As I said earlier, investing is hard and you are going to experience some real heartaches along the way.

Once your capital gets bigger, you should start to consider building your own portfolio so that you can manage your risks better. While the monthly investment plan is an easy way to start and to accumulate investment capital, you would end up with a haphazard portfolio that may not meet your risk profile.

Remember also that I mentioned that the financial advisors and Robo-advisors are using the modern portfolio theory to construct the portfolio for you?

You can actually build it yourself without much fuss as well.

There are many platforms that allow you to buy unit trusts directly. You can also use ETFs too. Costs have gone down over the years and information has become more abundant for you to learn how to DIY.

I have given numerous talks on this matter and this is a recent one at an SGX event.

These portfolios are called Lazy Portfolios. As the name suggests, you do not need to spend a lot of time on it. Just a day a year to do some buy and sell for your portfolio. There are many types of Lazy Portfolios for your reference.

Permanent Portfolio is one of the Lazy Portfolios with relatively low volatility. This would help ease investors who cannot withstand large swings in their portfolio value. It was championed by Harry Browne and first described in his book, Fail-Safe Investing. Craig Rowland wrote a more detailed account on how to set up a Permanent Portfolio and the thinking behind it. I wrote a book on how to implement a Singapore Permanent Portfolio.

Active investments would give you the most amount of headaches and heartaches. Many people have tried and most have given up. It takes a lot of love and commitment for active investing to make it work.

I am not sure if this is for you. Based on statistics, most people are better off investing passively. If you think you fall into the minority category, be sure to read on.

One of the first decisions you have to make is which asset class you want to excel in.

Is it going to be properties, stocks, bonds, forex, cryptocurrency or something else?

There are a million ways to make a million dollars. You just need to be an expert in one and not become a jack of all trades. I realised that many investors keep hopping from one asset to another instead of becoming very good in one.

You need to have deep expertise and be in the top 10% in order to beat the majority of the people.

I have never met anyone who became rich because he invested in a ton of things. Usually, they got rich because of one thing and subsequently they move on to other things to diversify. So pick one asset and stick to it until you become better than most people.

I am biased towards stocks when it comes to investing. I know that real estate investing has been very popular among Singaporeans. I know people who are successful in real estate investing but I am not going to cover it here because I’m not an expert in this area. You can check out Vina’s blog about property investment.

The second decision to make is the strategy or approach you are going to use. There are many approaches even for stock investing alone. Some people go long and some go short. Some use a top-down macro approach while others do bottom-up stock picking. Some do fundamental analysis and others practise technical analysis. Some prefer a more methodical quantitative approach while others are more qualitative in their analysis.

It is thus very common for beginners to feel overwhelmed by the number of approaches and to be confused about which strategy to use.

Worse, each advice tends to contradict the next. It is hard to tell who is speaking the truth. It is hard to tell who can be trusted.

At the end of the day, no one has a complete understanding and view of the markets. It is almost impossible.

As trader Van Tharp said, “we don’t trade the markets, we trade our beliefs of the markets”.

So investing is like a religion. Everyone has his own beliefs. Their beliefs often contradict others’ beliefs. There’s no end arguing about who is right or who is better. Practise some tolerance and do what you think is right for yourself. You invest your own money and you answer for it. You don’t need to care about how others invest their money.

When I embarked on my active investing journey, I tried almost everything there is out there. I did structured warrants, trend following on stocks using CFDs, fundamentals analysis stock picking, forex trading and selling naked options on futures. I read a lot of books and attended numerous seminars and courses. Results were a mixed bag. But I persevered until I finally saw results by applying a more methodical factor-based investing approach.

It is like a rite of passage. At the end of the journey, you will discover what suits you. Think of it like dating. Some investors meet the right partner from the start while others have to try a lot more and spend more time to get to the suitable approach. You may ask how do you know if a strategy suits you. I would say if you don’t know if it does, then you have not found the right strategy yet.

Personally I practise the principles of factor-based investing. I have detailed the approach here if you are keen to find out more.

This has always been a controversial issue.

Investment courses are always seen as get-rich-quick promises that cost a lot and are useless in the end.

I don’t blame people adopting such a perception because indeed there are a lot of audacious promises made by various trainers to entice people to sign up.

But we know investing is a journey and a very tough one. No one can predict or control the outcome of investing. It is too easy for the high expectation to be disappointed by reality.

Dr Wealth runs investment courses.

We want to paint the reality as closely as possible to set the right expectations. We always say that investing is a long term endeavour. It is not an overnight success avenue that would provide you with immediate F*** You Money for you to quit your job the next day.

Most people are not suited for active DIY investing.

I know of investors who became successful without attending any courses. It is natural for them to they think investment courses are a waste of money and time.

But we cannot assume that everyone is self-disciplined enough to wade through uncharted waters and to eventually come out ahead. I have paid for investment courses and I felt that my learning was accelerated and I could understand things better than I could on my own.

Secondly, I could also implement an investment strategy after the class and be confronted with some real-life training. It is after testing a few investment approaches that I could decide what suits me.

It is up to you whether you think a structured way of learning would be beneficial to you.

Some of you might be thinking of investing your CPF Ordinary Account money.

My rule is always to invest the spare cash first before touching the CPF. You must also be proficient enough to start investing your CPF monies. This is because cash has much lower opportunity cost than CPF OA funds. Deposit interest on cash is negligible but CPF OA is earning 2.5% at the time of writing.

This means that your investments have a higher hurdle rate to climb to make it worthwhile.

Those who have funds in SRS accounts should invest otherwise they will sit idle without any returns. A little-known issue is that you can end up paying more tax if you are a very good investor when you use your SRS account.

SRS can help you defer your tax to a later stage. This helps because when you withdraw money at a later age, you are at a lower tax bracket (hopefully) since you won’t be drawing a salary. But if your withdrawal amount is large due to the success of your investments, you might end up paying more taxes. Your capital and dividend gains which are not taxable when you use cash would become taxable at SRS withdrawals.

In general, I do not like to use SRS for the same reason with CPF top-ups – you would lose the freedom of money. Moreover, policies may change over time and there’s a possibility that the advantages may diminish.

There’s just so much noise in this Information Age. Basically the advent of online social media has resulted in fake news travelling faster and wider than ever in history.

It is often hard to tell the signal from the noise. For example, you can get very polarising and opposite advice about how you should manage your finances on social media. You have to think about how relevant it is for your context.

You cannot be gullible and believe everything you read or hear. You must be able to exercise critical thinking and decide what is suitable for you. Arming yourself against noise is a key skill to survive in today’s world.

Investment scams are indeed one of the most dangerous fake news ever. You’ve got scams in land banking, foreign properties, pre-IPO stocks, gold, agarwood, wine, bitcoin, etc.

There are moments in life where being the Ham in the Sandwich gets so tiresome and you feel like you could really do with some help to break out of the cycle. That is when quick get rich schemes so inviting. You are willing to take the chance because you have just put yourself into a trance. You bite it and eventually, it sets you back by $50,000.

This is not easy but you have to constantly protect yourself (and your family and friends) from such scams. Having a sceptical mind as a default would help greatly.

You can take this interesting Calling Bullshit Course to hone your critical thinking skills. It’s free and awesome.

To be the last Sandwich Generation, you have to start taking on more responsibility. You have to believe that you have some degree of control to influence future outcomes.

Money is a core resource in a capitalistic society and you must be able to master your personal finance. You can have some control of your life as long as you can control money. The lack of it will ruin your life in almost every area. So take responsibility from today onwards.

But don’t be too competitive about money. Don’t try to keep up with the Jones’. Run your own race.

You don’t need to be richer than your childhood friend or your arch-enemy. Warren Buffett has always advocated having an inner scorecard instead of an external one.

Do you really want something?

Or is it just an act to garner validation from others around you?

As much as we want to control our outcomes in life, we are still subjected to the luck factor. Things happen and often outside of our plans. We can get lucky. We might meet misfortunes. Know what you can control and what you cannot.

For those who tend to live a more carefree life, you need to put in more control in your life.

For those who are OCDs, you need to acknowledge that life doesn’t always unfold as you plan. Stop fretting about things outside of your control.

Life will throw you a curveball once in a while. How you respond matters.

Self- help gurus have a useful equation:Event + Response =Outcome

You cannot control a bad event from happening but your response can change the outcome.

Whatever you do, don’t practise self-pity and sit there and complain about why the world is unfair to you.

Do something about it.

Every generation has its unique challenges.

My grandparents had to live through wars and worry about survival, putting food on the table on a day-to-day basis. My parents had to go through a rapid transformation of Singapore. There were no playbooks or SOPs and my grandparents weren’t able to give good advice in this new world. My parents had to figure out how to make the best out of their new environment.

Now that we have landed ourselves in the Sandwich Generation, our challenge is in having enough money to support our parents, children, as well as taking care of our own retirement. We need to start taking charge of our finances. Money becomes an ever more important subject and we need to figure it out as early as possible.

I went through many aspects of personal finance in this guide and hopefully, you would have picked up something useful.

Your career is still what you will make most of your money from. Human capital is your most valuable asset and the market will pay you for it. Your earlier years will always be about converting your life to money.

Spending as much as you earn isn’t a good idea. You need to save money. You need to start accumulating financial capital because your human capital will decline overtime.

You want to buy insurance against whatever is possible to derail you financially, within your affordability.

Don’t just save. You must invest your money. There are several ways to do it. Some higher risks, some higher effort. Pick what suits you best.

Think critically and don’t fall for bullshit. Control what you can control and don’t fret about things outside your control. Just make sure you respond as wisely as possible when events happened.

I wish us all the best in our endeavour to become the last Sandwich Generation.

If you have enjoyed this, feel free to join our Ask Dr Wealth Facebook Group. If you want to receive up to date articles daily, you can also join our telegram group chat.

For those of you who are uncertain of how to get started, or how to generate clear buy/sell prices for stocks, you can register for a seat here. Free of charge.